Will a New Fed Chair Really Bring Mortgage Rates Down? Here’s the Reality

With news that President Trump has nominated Kevin Warsh to become the next chair of the Federal Reserve, talk about mortgage rates has heated up fast. Some say this change will push rates lower. Others expect a quick wave of Fed cuts to follow.

Most of that talk misses how mortgage rates really work. Let’s slow things down and clear up what matters and what doesn’t.

Why Do People Think Kevin Warsh Means Lower Rates?

To be blunt, the identity of the nominee isn’t the key issue.

Anyone paying attention already knew the next Fed Chair nominee would likely support more rate cuts. That expectation has been priced into markets for months. Warsh’s nomination didn’t suddenly introduce a new idea it confirmed what investors already assumed was coming.

That’s why it’s strange that this conversation only gained traction now. The idea of a more rate-friendly Fed leadership has been widely expected for a long time.

Do Fed Rate Cuts Lower Mortgage Rates?

No not directly.

The Fed controls short-term interest rates, not long-term ones like mortgages. Mortgage rates are tied to the bond market, especially longer-term Treasury yields and mortgage-backed securities.

By the time the Fed actually cuts rates, the reasons behind that decision slowing growth, weaker jobs, softer inflation have usually already been absorbed by the bond market. That’s why mortgage rates often fall before Fed cuts happen.

This explains why mortgage rates and the Fed Funds Rate often move together over long periods, but not always in the way people expect in the short term.

Why the Fed Cut Myth Won’t Go Away

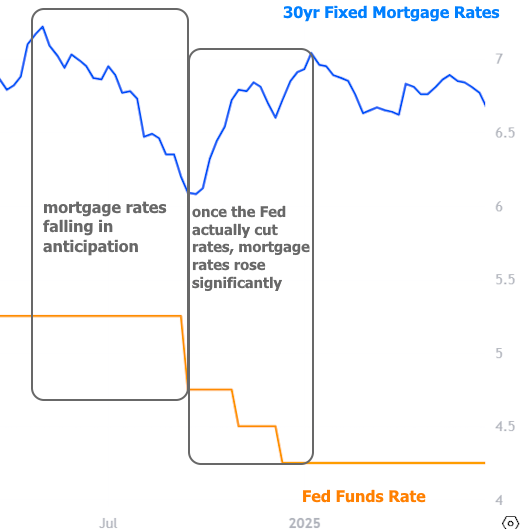

Many people still believe that Fed cuts automatically push mortgage rates lower. History says otherwise.

In late 2024, mortgage rates reached major lows before the Fed cut rates. After the Fed finally began cutting, mortgage rates moved higher for months even while cuts continued.

That pattern wasn’t unusual. It’s how markets work.

What If the New Fed Chair Pushes Rates Lower Anyway?

Even if you strongly believe that the new Fed leadership will lead to lower rates, there’s a hard truth to accept:

If you know it, so does the bond market.

Bond traders act fast. They don’t wait for official announcements. When expectations become clear, they are priced in almost immediately. Any future outcome that seems “obvious” to the public has already been traded by professionals.

That means there’s no hidden advantage in waiting for something that everyone already expects. Markets don’t reward certainty they remove it.

So What Actually Moved Mortgage Rates This Week?

Jobs data not Fed politics.

Thursday stood out as the most important day for rates. Three employment-related reports pointed to a weaker labor market. Slower job growth tends to lower inflation pressure, which bond markets like.

As bonds rallied, mortgage rates improved.

Part of that move was also driven by positioning ahead of next week’s major jobs report the most important labor data release of the month.

What Happens Next Depends on the Jobs Report

- If job growth weakens further: mortgage rates could fall again and revisit January’s lows

- If jobs data meets expectations: recent gains may fade

- If hiring surprises to the upside: rates could rise to their highest levels since December

That report not the Fed Chair will likely set the tone.

Bottom Line

A new Fed Chair doesn’t control mortgage rates. Bond markets do.

Fed cuts don’t magically lower mortgage rates. Expectations already priced into the market matter far more.

Right now, labor market data not politics is driving rate movement. Anyone watching mortgage rates in 2026 should keep their eyes on economic reports, not headlines. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses