Low Pay and High Mortgage Rates Seen as Biggest Barriers to Homeownership, Survey Finds

Housing affordability remains a major concern for Americans, and a new national survey shows that most people believe the problem comes down to one simple issue: they don’t earn enough money to buy a home.

A Bright MLS survey of roughly 3,000 Americans found that more than 90% believe housing affordability is a serious problem. When asked why, respondents pointed most often to low incomes and high mortgage rates, rather than housing shortages or construction issues.

Income and Mortgage Rates Top the List

More than half of survey participants (55.5%) said the biggest reason housing feels out of reach is that incomes are too low. High mortgage rates followed closely, cited by 50.1% of respondents.

While many Americans acknowledge that housing supply plays a role, fewer see new construction as the main cause of the affordability problem. About 43% said there aren’t enough homes being built at affordable prices, and only 24.5% felt there aren’t enough homes where people want to live.

Interestingly, 32.3% of respondents blamed real estate investors for affordability challenges, even though investors make up a relatively small share of total home purchases. The survey was conducted before recent policy discussions around limiting institutional homeownership.

Views Are Consistent Across Age Groups

Across all age ranges, income was the most common concern. Younger adults under 40 were slightly more likely to point to a lack of new homes in desirable locations, while people aged 60 and older were more likely to say affordable homes are simply not being built.

Overall, Bright MLS said consumers tend to focus more on personal financial pressure earnings and loan costs than on broader supply-side explanations.

Short-Term Reality Matches Consumer Views

In recent years, consumer perceptions may be well aligned with economic data. Between 2010 and 2020, household income growth generally kept pace with home prices. That balance changed sharply in 2020.

Since then, home prices have risen much faster than wages, creating a widening gap between what homes cost and what people earn. This shift is one of the main reasons buyers feel priced out today.

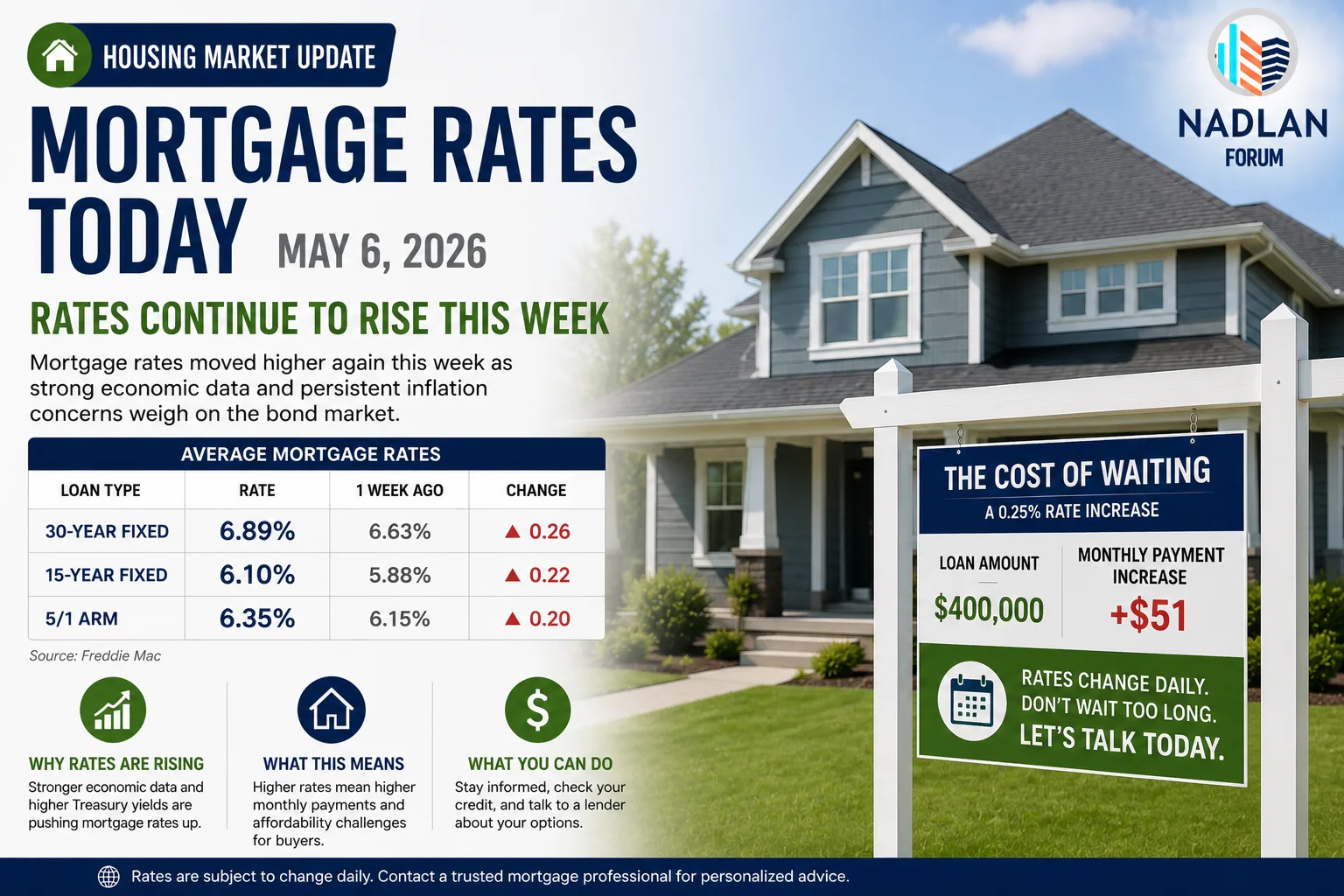

Mortgage rates also began climbing around the same time. After years of steady declines, rates rose quickly starting in 2020 before leveling off at higher levels, adding to monthly payment pressure.

Construction Looks Stronger in Recent Years

Bright MLS noted that housing construction activity has improved compared to the period following the Great Recession. New building permits are significantly higher today than in 2010, suggesting that recent supply growth is not unusually weak by short-term standards.

That helps explain why many consumers point to income and mortgage rates first. When people think about recent changes, they remember rising prices and loan costs more than long-term building trends.

The Long-Term Picture Tells a Different Story

Looking further back, housing affordability issues become more complex. Mortgage rates today are far lower than they were in the 1980s, but major price jumps occurred during periods when borrowing became easier.

These include the early 2000s, when subprime lending expanded access to mortgages, and the 2020–2021 period, when very low interest rates fueled rapid home price growth.

Over the past two decades, income growth has generally lagged behind home prices, especially during boom periods. Without those sharp surges, incomes and prices may have stayed closer in line.

Housing Supply Still Lags Over Time

While construction has improved recently, Bright MLS noted that long-term housing supply still trails levels seen in the late 1980s and 1990s. Even with recent gains, new home building has not fully caught up with population growth and demand.

Bottom Line

Most Americans see housing affordability as a personal financial issue, driven by earnings that haven’t kept pace with prices and mortgage rates that remain elevated. While supply matters over the long run, today’s buyers are feeling the impact of tighter budgets and higher monthly payments making income growth and borrowing costs central to the homeownership challenge. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses