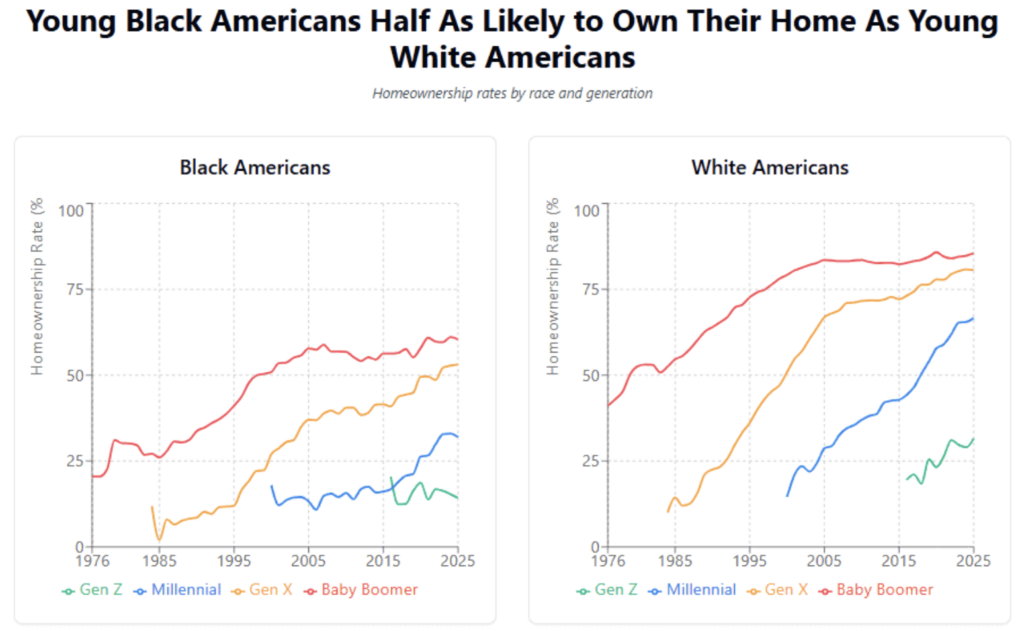

Racial Homeownership Gap Widens Among Gen Z and Millennials

Homeownership in the United States continues to show clear divides across generations and race. New data from Redfin highlights a growing racial homeownership gap, especially among younger Americans.

Among Gen Z adults nationwide, 31.6% of white Gen Zers own their homes compared to just 14.2% of Black Gen Zers. The pattern continues with millennials: 66.6% of white millennials are homeowners, while only 32% of Black millennials own their homes.

While homeownership rates for white young adults have increased slightly over the past two years, rates for young Black Americans have declined.

Recent Trends Show Diverging Paths

In 2023, 16.3% of Black Gen Z adults owned homes. That figure has now dropped to 14.2%. For Black millennials, the rate slipped from about 33% in 2023 to 32% today.

By contrast, white Gen Z homeownership rose from 29.7% to 31.6% over the same period. White millennial homeownership increased from 65.3% to 66.6%.

These numbers reflect more than personal choice. Economic conditions and long-term wealth differences continue to shape who can buy a home.

Why Young Black Americans Face Greater Barriers

Several economic factors help explain the racial homeownership gap:

1. Income Differences

Black workers in the U.S. earn about 79 cents for every dollar earned by white workers. Lower income makes it harder to save for a down payment and qualify for a mortgage.

2. Wealth Gap

Black households hold about $15 in wealth for every $100 held by white households. Since homebuying often depends on savings or family support, this wealth gap creates a major barrier.

3. Unemployment Disparities

Black workers experience higher unemployment rates than white workers. Recent data shows:

- Black men unemployment: 7.1%

- White men unemployment: 3.7%

- Black women unemployment: 6.7%

- White women unemployment: 3.2%

Economic downturns, including the Great Recession and the pandemic, hit Black workers harder.

The Role of Housing Market Conditions

Younger Americans are entering the housing market during a period of:

- High home prices

- Elevated mortgage rates compared to pre-pandemic levels

- Limited housing inventory

These conditions make homeownership harder for all first-time buyers. However, those with less access to savings or family support face even steeper challenges.

According to a recent Redfin survey, 15% of white recent homebuyers used a cash gift from family to help fund their down payment. Only 9% of Black buyers reported receiving similar assistance.

Family wealth transfers often make the difference between renting and buying.

Structural Barriers Still Matter

Historic housing policies such as redlining and discriminatory lending practices limited homeownership opportunities for Black families for decades. Those past policies still affect wealth accumulation today.

Even now, Black mortgage applicants are about twice as likely as white applicants to face loan denials. Credit score differences also contribute. Median credit scores for Black borrowers are lower than for white borrowers, which can raise borrowing costs or limit access to financing.

Older Generations Show Gaps Too

The racial homeownership gap is not limited to younger generations.

- 80.6% of white Gen Xers own homes compared to 53.1% of Black Gen Xers.

- 85.5% of white baby boomers are homeowners compared to 60.4% of Black baby boomers.

While the gap is slightly smaller among older groups, it remains significant.

Homes were generally more affordable when older generations entered the market. However, long-standing wealth and income differences continued to affect ownership rates across race.

Why Homeownership Matters

For many families, homeownership is the largest source of wealth. It provides:

- Equity growth

- Stability

- A financial asset that can be passed to the next generation

Lower homeownership rates limit wealth-building opportunities and reinforce broader economic gaps.

What Could Help Close the Gap?

Experts suggest several approaches that may help reduce the racial homeownership gap:

- Expanding affordable starter home supply

- Increasing down payment assistance programs

- Improving access to fair lending

- Supporting credit-building initiatives

- Providing targeted first-time buyer programs

Policies focused on improving affordability overall would help all young buyers. However, addressing structural and wealth-based differences may require more targeted solutions.

Outlook for 2026

There are signs that housing affordability may slowly improve. Mortgage rates have eased in recent months, and wage growth has outpaced home price growth in some areas.

More inventory and slower price increases could also give buyers more negotiating power.

Still, without changes that address deeper economic gaps, disparities in homeownership may continue.

The racial homeownership gap reflects long-term economic patterns. While market conditions shift year to year, wealth, income, and access to opportunity remain key drivers of who can buy a home — and who cannot. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses