Subsidized Credit and Rental Investors: Why They’re Winning More Bidding Wars

Single-family rental homes play a major role in the U.S. housing system. These 1–4 unit properties provide space for families who are not ready or able to buy. Many of these homes are similar to entry-level houses, often with three or four bedrooms, average values near $300,000, and rents around $1,800 per month.

But new research from the American Enterprise Institute (AEI) raises an important question: Should federal mortgage policy support investors who are competing with first-time homebuyers for the same starter homes?

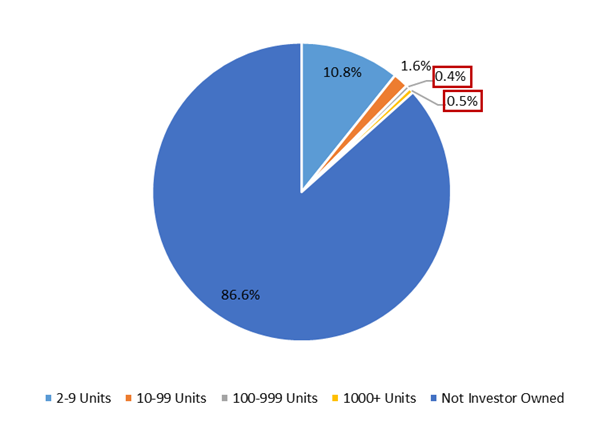

Institutional Investors vs. Small Investors

Public debate often focuses on large institutional landlords. However, AEI’s findings show that these firms own only about 1% of the single-family housing stock. By contrast, small-scale “mom-and-pop” investors who own fewer than nine homes control roughly 10.8% of the market.

The larger issue is not the size of ownership concentration, but how these investors finance purchases.

Between 2018 and 2024, nearly 40% of small-investor purchases were backed through the government-sponsored enterprise (GSE) channel. The two main GSEs, Fannie Mae and Freddie Mac, provide liquidity to the mortgage market. Their backing lowers borrowing costs for qualified loans.

According to AEI, that lower cost of capital can give investors stronger bidding power when competing for entry-level homes.

Why Financing Matters in Competitive Markets

Investors financed through the GSE system typically receive lower interest rates than they would through private lenders. Research shows private investor loans can run 90 to 100 basis points higher than comparable GSE-backed loans.

On a $250,000 mortgage, the difference between a 7% and 8% interest rate can reduce monthly principal and interest payments by about $170. That translates into roughly $2,000 per year in savings and nearly 10% greater borrowing capacity.

In competitive markets, that margin can determine who wins a bid.

This advantage becomes more significant when investors and first-time buyers are targeting the same properties.

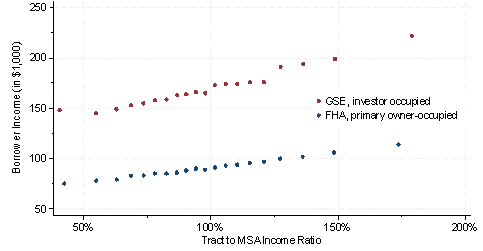

FHA Borrowers and GSE Investors Target Similar Homes

Data shows that FHA borrowers and GSE-financed investors often compete in similar neighborhoods at similar price points.

- Average FHA owner-occupied purchase price: $326,000

- Average GSE-financed investor purchase price: $336,000

Neighborhood income levels also overlap. Median income ratios in census tracts are nearly identical for both groups.

In about 26,000 census tracts analyzed, GSE-backed investors accounted for 22% of transactions. That means roughly one investor purchase for every four FHA purchases in the same areas.

This suggests investors are not operating in a separate market segment. They are frequently bidding on the same homes sought by first-time buyers.

Differences Between Borrowers

Although they compete for similar homes, the borrower profiles differ sharply.

Median income levels show a wide gap:

- Median FHA borrower income (2023): about $90,000

- Median GSE investor borrower income (2023): about $170,000

After adjusting for local income differences, GSE investor borrowers still earn about 90% more than FHA borrowers.

Age differences are also notable. Investor borrowers tend to be 15–20 years older on average, indicating they are often more financially established.

Demographic data also shows variation:

- 48% of FHA borrowers identify as Black or Hispanic

- 20% of GSE investor borrowers identify as Black or Hispanic

- 60% of GSE investor borrowers are non-Hispanic white

This suggests FHA lending serves a broader share of minority households, while investor financing is concentrated among higher-income borrowers.

Rental Housing Is Not the Core Problem

Single-family rentals meet a real need. Around 9.9 million low-income households rent single-family homes. Many would not qualify for a mortgage due to credit limits, income instability, or documentation challenges.

For these families, rental housing provides stability. Removing rental supply entirely would not solve affordability problems.

The policy concern is narrower: Should federal mortgage programs lower borrowing costs for investors competing with first-time buyers for limited starter-home supply?

Supply Is Still the Long-Term Solution

The research makes clear that supply constraints remain central to the housing challenge. More family-sized homes would reduce competition across all buyer groups.

However, mortgage policy can influence short-term competition. Evidence from prior policy adjustments shows that when GSE support for investor purchases is reduced, investor demand declines and private credit does not fully replace it. In those periods, more homes become available to owner-occupants.

This does not eliminate rental housing, but it may rebalance access to starter homes.

Policy Implications for First-Time Buyers

Refocusing GSE policy toward homeownership rather than investor activity could improve access for FHA and other first-time borrowers.

The debate is not about eliminating investors. It is about whether government-backed financing should give higher-income investors a structural advantage over households seeking to buy their first home.

Starter homes remain a key path to long-term wealth building. Ensuring fair competition for those homes may require revisiting how federal mortgage support is structured.

As housing affordability remains tight in many markets, the role of GSE financing in shaping investor demand will likely stay at the center of policy discussions. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses