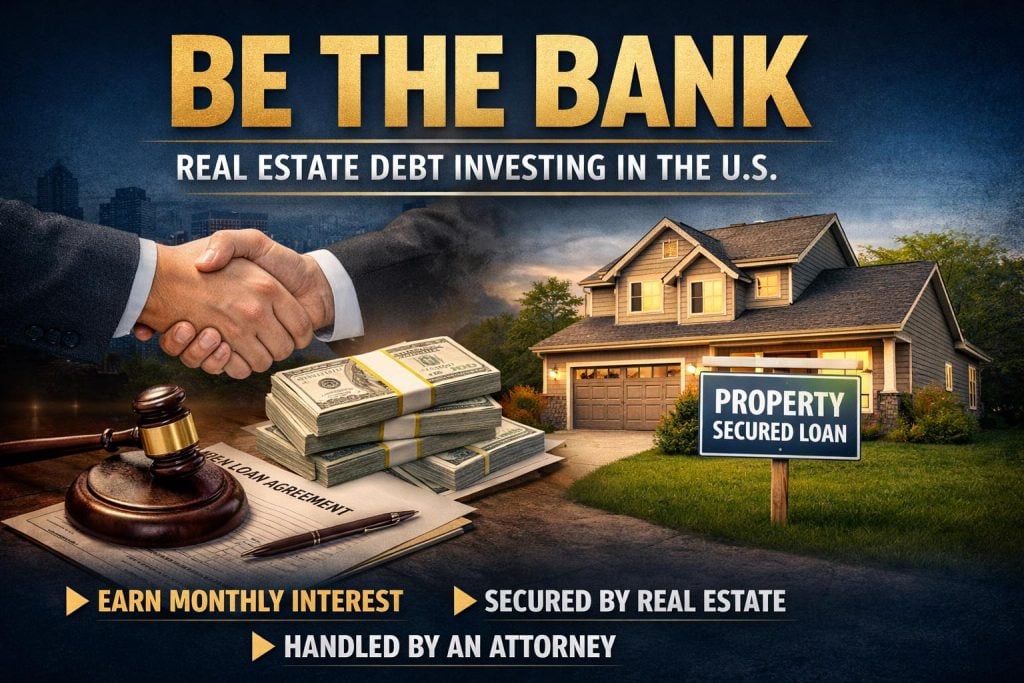

Be The Bank: Real Estate Debt Investing In The U.S.

Most people enter real estate through buying, renovating, and renting.

There’s a completely different path: debt investing backed by real estate.

Instead of owning the property—you become the bank.

You lend money to an investor or developer,

and receive security in the form of a lien on the property.

Not presentations. Not promises.

A real, legally recorded collateral.

How does it work?

The deal is structured properly through:

- A real estate attorney

- A title company

- A loan agreement

- A promissory note

- A recorded lien (mortgage/deed of trust)

This gives you legal rights to the property if the borrower defaults—

without having to manage the asset day-to-day.

How do you make money?

Two main structures:

1. Interest-only + balloon payment

- Monthly interest payments

- Full principal returned at the end

2. Amortized payments

- Monthly payments that include both principal and interest

Typical deal profile

- Investment size: ~$50,000+

- Term: 1–5 years

- Returns: typically 8%–12%, depending on:

- Risk level

- Borrower quality

- Property quality

Why investors like this strategy

✔️ Predictable cash flow

✔️ Less dependency on market timing

✔️ No tenants

✔️ No renovations

✔️ No operational headaches

✔️ Priority position over equity holders in case of default

But it’s not risk-free

If the borrower doesn’t pay:

- You must enforce the lien

- Possibly go through foreclosure

Which means:

- Proper Loan-to-Value (LTV) is critical

- Borrower quality matters—a lot

Bottom line

You’re still in real estate—

but you’re not relying on appreciation or execution.

You’re working with capital, not hope.

And investors who truly understand control and risk management

often prefer being on the lender side—

not the operator side.

Responses