The Bank of Mom and Dad: Family Support Shapes First-Time Homebuying

Parents Playing a Bigger Role in Homeownership

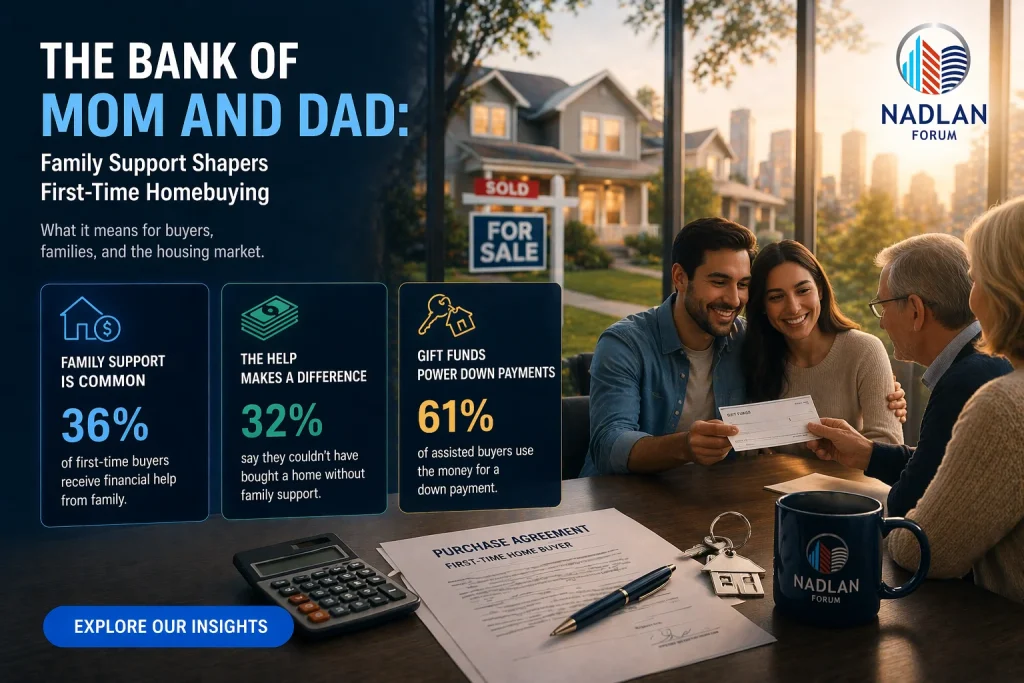

Buying a first home is becoming more difficult, and many younger buyers are turning to family for help. A recent survey from Veterans United Home Loans shows that nearly 6 in 10 parents are either helping or planning to help their children purchase a home.

This growing trend highlights how affordability challenges are changing the path to homeownership. With rising home prices, higher interest rates, and stricter lending standards, family support is becoming a key factor for many first-time buyers.

Support appears even stronger among military families, where a larger share of parents say they are willing to step in financially.

Why Parents Are Stepping In

There are two main reasons parents are helping: upfront costs and loan qualification.

Saving for a down payment remains one of the biggest hurdles. Many buyers also struggle to meet income or credit requirements needed to secure a mortgage.

According to the survey:

- 43% of parents help with down payments

- 33% assist with closing costs

- 37% aim to improve mortgage approval chances

Beyond immediate costs, some parents are thinking long term. Many want to help their children build equity, reduce monthly payments, or access better neighborhoods and schools.

Common Ways Families Provide Support

Parents are using a range of strategies to support homebuyers. Some of the most common include:

- Contributing directly to the down payment

- Gifting cash for purchase-related expenses

- Paying off existing debt to improve credit profiles

- Covering closing costs or moving expenses

- Allowing children to live at home to save money

In many cases, this support is given without the expectation of repayment. Over half of parents describe their contributions as gifts, while others structure them as loans or a mix of both.

How Much Money Are Parents Giving?

The level of financial support can be significant. Many families are contributing tens of thousands of dollars to help make homeownership possible.

Survey results show:

- 30% plan to contribute between $25,000 and $49,999

- 23% expect to give between $50,000 and $99,999

- 12% anticipate contributions exceeding $100,000

These amounts can make a major difference, especially in competitive housing markets where upfront costs are high.

Where the Money Comes From

To provide this support, parents are tapping into different financial resources:

- Savings and cash accounts

- Investment portfolios

- Home equity

- Retirement funds

- Inheritance or trust funds

While this approach can help younger buyers, it also means some parents are stretching their own finances or adjusting long-term plans.

Parents Taking a More Active Role

In some cases, parents are going beyond financial gifts and becoming directly involved in the homebuying process.

- About 18% have co-signed or plan to co-sign a mortgage

- Another 17% have bought or may buy a home outright for their child

- A similar share are offering private loans

These actions can improve loan approval chances and reduce borrowing costs, but they also come with financial risks for parents.

What This Means for the Housing Market

The rise of family-assisted homebuying is changing the dynamics of the housing market. Buyers with financial support may have an advantage over those relying solely on personal savings.

This trend could:

- Increase competition among first-time buyers

- Widen the gap between those with and without family support

- Influence home prices in certain markets

At the same time, it reflects how households are adapting to ongoing affordability challenges.

Things to Consider Before Accepting Help

While family support can make buying a home easier, there are important factors to consider:

- Clearly define whether the support is a gift or a loan

- Understand tax implications for large financial gifts

- Ensure proper documentation for mortgage approval

- Discuss expectations upfront to avoid future conflicts

Planning ahead can help both parents and buyers avoid misunderstandings later.

Final Thoughts

Parents helping children buy a home is becoming a common part of today’s housing market. As affordability challenges continue, family support is helping many buyers take their first step into homeownership.

While this trend opens doors for some, it also highlights the financial barriers that still exist. For many households, reaching the goal of owning a home now depends not just on personal savings, but on family support and long-term planning. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses