Mortgage and Refinance Rates Hold Steady as Experts Predict Prolonged Highs

August 4, 2025

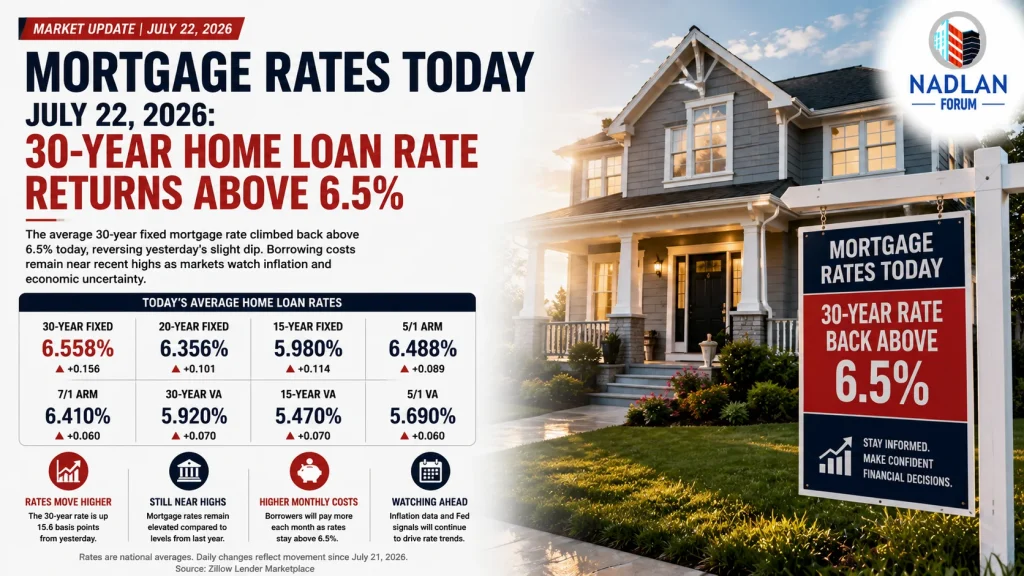

Mortgage rates have seen only minor shifts this week, remaining at elevated levels that continue to challenge homebuyers. According to the latest data from Zillow, the average 30-year fixed mortgage rate stands at 6.60%, while the 15-year fixed rate holds at 5.76%. Despite early-year optimism for a drop, the reality is that borrowing costs are expected to stay high well into 2026.

📈 Where Rates Stand Today

Here’s a snapshot of the current national mortgage and refinance rates:

| Mortgage Type | Purchase Rate | Refinance Rate |

|---|---|---|

| 30-Year Fixed | 6.60% | 6.66% |

| 20-Year Fixed | 6.36% | 6.09% |

| 15-Year Fixed | 5.76% | 5.39% |

| 5/1 ARM | 6.91% | 7.32% |

| 7/1 ARM | 7.12% | 6.75% |

| 30-Year VA | 6.22% | 6.03% |

| 15-Year VA | 5.58% | 5.67% |

| 5/1 VA ARM | 5.94% | 6.03% |

💡 Note: These rates are national averages and may vary based on lender, credit profile, and location.

🏠 What This Means for Buyers

The Mortgage Bankers Association (MBA) forecasts that 30-year rates will likely finish the year around 6.7%, remaining elevated into next year. Rates are projected to hover between 6.4% and 6.6% throughout 2026.

That means affordability remains tight. For example, on a $300,000 30-year fixed loan at 6.60%, your monthly principal and interest would be about $1,916, and you’d end up paying nearly $390,000 in interest over the life of the loan.

Opting for a 15-year mortgage? At today’s average of 5.76%, that same $300,000 loan comes with a monthly payment of $2,493, but you’d only pay $148,711 in interest a significant savings, though with higher monthly costs.

🔄 Refinancing Outlook

Refinance rates remain slightly above purchase rates, as is typical. However, refinancing might still make sense for homeowners seeking to tap into equity or switch from an adjustable-rate loan to a fixed-rate option.

⚠️ Tip: Before refinancing, weigh closing costs against long-term interest savings.

🔄 Fixed vs. Adjustable Rates

Adjustable-rate mortgages (ARMs) offer lower initial rates but carry the risk of rate increases down the line. With 5/1 ARMs averaging 6.91% and 7/1 ARMs at 7.12%, the benefits aren’t currently as clear-cut especially when compared to stable 30-year fixed options.

However, ARMs could work if you’re planning to move within a few years, allowing you to benefit from the lower introductory period without long-term risk.

✅ How to Get the Best Mortgage Rate

To score a lower rate, focus on the following:

- Boost your credit score

- Lower your debt-to-income ratio (DTI)

- Make a larger down payment

- Shop multiple lenders for quotes

- Consider buying discount points to permanently lower your rate

Another strategy is using a temporary buydown, such as a 2-1 buydown. For instance, if your final rate is 6.5%, your rate would start at 4.5% for the first year, then rise to 5.5% in year two before settling at 6.5%.

🧮 Use a mortgage calculator to estimate your monthly payments and compare scenarios based on rate and loan term.

❓Frequently Asked Questions

What’s the average mortgage rate today?

As of August 4, 2025, the average 30-year fixed rate is 6.60%, while the 15-year fixed is 5.76%, per Zillow.

Will rates go down this year?

Experts believe mortgage rates will likely stay elevated throughout 2025 due to inflation concerns, global trade pressures, and the Federal Reserve’s monetary policy stance.

Should I lock my rate now?

If you’re planning to buy or refinance soon and want to protect yourself from rate hikes, it may be wise to lock in your rate especially if it fits your budget and timeline.

Bottom Line:

Mortgage rates remain stubbornly high, and while minor fluctuations are occurring, a major drop isn’t on the horizon. If you’re in the market, your best bet is to stay informed, improve your borrower profile, and explore lender options to secure the most favorable terms available. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses