Older Hispanic Homeowners Face Challenges in Passing Down Housing Wealth

For many older Hispanic homeowners, a house represents more than just a place to live it is often their most valuable financial asset and a potential source of generational wealth. Yet, for a significant portion of this population, the dream of converting homeownership into a lasting financial legacy remains out of reach. A recent analysis from the Harvard Joint Center for Housing Studies highlights the structural and financial obstacles that prevent many Hispanic families from preserving and transferring their housing wealth to younger generations.

A Gap in Non-Housing Wealth and Income

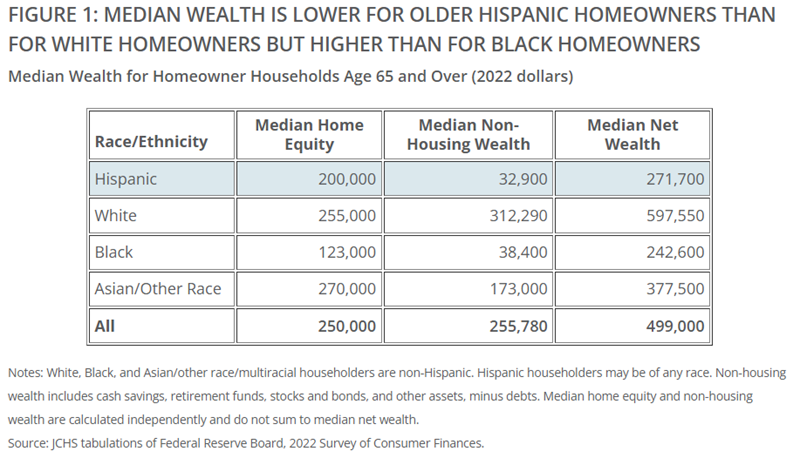

In 2022, Hispanic homeowners aged 65 and older had dramatically less wealth outside their homes than their white counterparts. The median non-housing wealth for older Hispanic homeowners was $32,900, compared with $312,290 for white homeowners a tenfold difference. Income disparities further exacerbate this inequality. Median household income for older Hispanic homeowners stood at $41,000, trailing the $55,590 median for white households.

These financial limitations restrict the ability of older Hispanic families to invest in home improvements, cover emergencies, or leverage their housing equity to support other family members. While homeownership can be a path to stability, without sufficient savings or income, it may offer only limited financial security.

Housing Costs and Debt Burdens

Housing-related expenses remain a significant hurdle. Older Hispanic homeowners who still carry a mortgage face median monthly payments of $911, notably higher than the $773 median reported for their white peers. Many live in regions where housing costs are rising faster than incomes, eroding potential home equity gains and making it harder to maintain or upgrade their properties.

Cash reserves are often minimal. Among Hispanic homeowners aged 65–74, the median cash savings was just $3,000—compared with $31,400 for white homeowners in the same age group. Limited liquidity makes it difficult to handle urgent home repairs, accessibility modifications, or other critical expenditures. The report notes that as homeowners age, they may face new financial pressures, including increased healthcare costs, mobility or functional limitations, and responsibilities for caregiving, which can further strain resources.

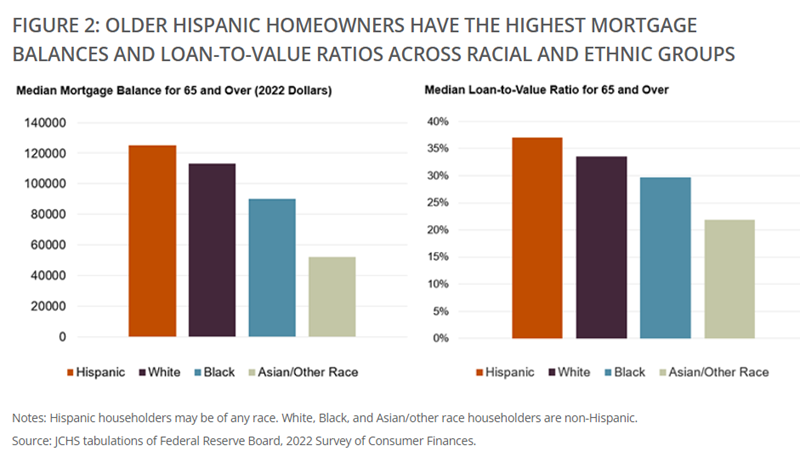

Mortgage debt into retirement compounds these challenges. Nearly 40% of Hispanic homeowners over 65 still had an outstanding mortgage in 2022, compared with about 33% of white homeowners. Those with mortgages often carried higher balances and owed more relative to the value of their homes, leaving them with less financial flexibility.

Implications for Intergenerational Wealth

The impact of these disparities is clear: many older Hispanic households have limited means to provide financial support for their children or grandchildren. Only 7.2% of Hispanic households reported receiving an inheritance or financial gift, compared with nearly 30% of white households. This gap highlights how homeownership alone does not guarantee long-term financial security or the ability to pass on wealth.

Experts note that closing this gap requires more than individual effort. Policies and programs that lower housing costs, provide assistance for caregiving, and support home modifications or repairs could help older Hispanic homeowners preserve their wealth. Financial education and access to credit for home improvements may also play a role. Without targeted support, the wealth divide is likely to persist for future generations.

Looking Ahead

As the population ages and housing costs continue to rise in many parts of the country, the challenges facing older Hispanic homeowners are likely to grow. Advocates argue that broader interventions—such as affordable housing initiatives, expanded social support for older adults, and programs that help households manage mortgage debt are essential to ensuring that homeownership can fulfill its promise as a tool for building intergenerational wealth.

Homeownership is a critical part of the American Dream, but it is not an automatic path to financial security or generational wealth, the report concludes. Without deliberate efforts to address systemic disparities in income, housing costs, and caregiving support, many older Hispanic families will continue to face barriers in turning their homes into a lasting financial legacy. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses