Despite Lower Mortgage Rates, Soaring Home Prices Still Lock Out Buyers

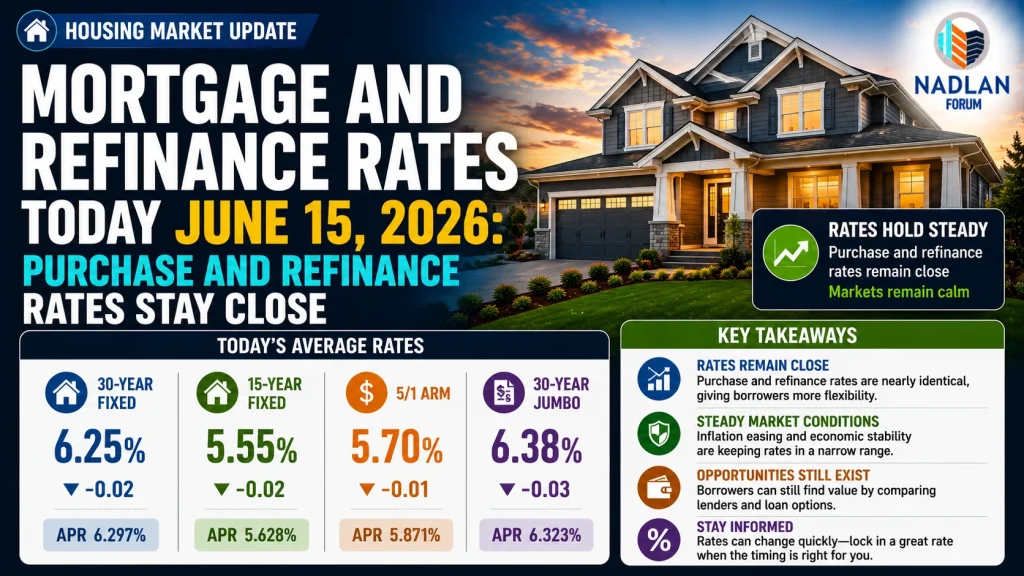

Mortgage rates have finally begun to cool after a turbulent two years, but for most Americans, homeownership remains painfully out of reach. The average 30-year fixed mortgage rate now sits around 6.2%, a noticeable improvement from the 6.8% average earlier this year. Yet, despite this drop, home sales remain stuck at near 30-year lows, underscoring a stubborn reality: falling rates alone aren’t enough to offset record-high home prices.

According to a new analysis from Harvard University’s Joint Center for Housing Studies (JCHS), the affordability crisis gripping the housing market is worse than at any point in modern history. Even with modest declines in mortgage rates, the cost of purchasing a home has more than doubled since 2020, thanks largely to skyrocketing prices and rising insurance and property tax bills.

The Price of Homeownership Has Doubled in Five Years

The numbers tell a sobering story. A typical first-time buyer putting down a small deposit now faces a monthly mortgage payment of roughly $2,500 compared to just $1,200 in 2020. To qualify for that loan, the household would need to earn more than $130,000 a year, nearly twice the income required just five years ago.

While today’s mortgage rates might feel steep compared to the ultra-low 3% levels during the pandemic, they’re not particularly unusual by historical standards. What is unprecedented, however, is the price of the homes themselves.

Nationally, home prices have surged by about 50% since early 2020, making the median home price now equivalent to five times the median household income a ratio never seen before in U.S. housing history.

This imbalance has created a generational divide: millions of younger and middle-income Americans are effectively priced out of homeownership, forced instead to remain in rentals or stay longer in family homes.

Why Falling Rates Don’t Guarantee Affordability

Lower mortgage rates may offer some breathing room for borrowers, but they don’t solve the bigger issue. Even a full one-percentage-point decline in rates would only trim monthly payments by roughly the same amount as a 10% drop in home prices a marginal improvement when prices are up 50% in just five years.

To return affordability to pre-pandemic levels, mortgage rates would need to plunge near zero, which is neither realistic nor sustainable in today’s inflation-conscious economy. Even then, other costs such as property taxes, insurance premiums, and maintenance expenses have surged alongside home values, ensuring that ownership remains far more expensive than it once was.

“What we’re seeing is a fundamental imbalance,” said Dr. Emily Santos, a senior housing economist at JCHS. “Interest rate cuts can provide short-term relief, but they don’t address the structural lack of affordable supply that’s keeping prices sky-high. The solution has to come from the construction side.”

The Real Problem: Not Enough Homes

Experts agree that the true bottleneck lies in the nation’s chronic housing shortage. Since 2010, the construction of smaller, more affordable homes such as starter homes, condos, and manufactured housing has fallen sharply. Builders have largely shifted focus to larger, higher-margin properties, leaving first-time and middle-income buyers with few options.

Recent data from the National Association of Home Builders (NAHB) shows that new housing starts in the “affordable” segment remain 40% below pre-Great Recession levels, even as demand continues to surge.

Meanwhile, zoning restrictions, high land prices, and construction costs have further squeezed supply. Many cities have struggled to reform outdated zoning laws that restrict duplexes or multi-family units in single-family neighborhoods policies that housing experts say are a major contributor to today’s affordability crisis.

“The market has been geared toward building luxury,” explained Mark Delaney, a real estate analyst with CoreInsight Analytics. “We need to shift toward building attainable housing smaller homes, accessory units, and multi-family developments that can meet the needs of working families.”

The Human Toll: Homeownership Out of Reach

For aspiring buyers, the emotional toll of being priced out is growing. A 2025 LendingTree survey found that 72% of renters still want to buy a home, but only 28% believe they’ll be able to afford one in the next five years. Many say they’ve delayed major life milestones like starting families or moving for better jobs because of housing costs.

The result is a widening gap between those who own homes and those who don’t. Homeowners have seen record gains in equity, while renters face rising costs and limited opportunities to build wealth.

Even homeowners hoping to move are often “locked in” by historically low mortgage rates from the pandemic years. Trading a 3% loan for today’s 6%-plus rate feels financially impossible for many, keeping existing inventory tight and driving prices even higher.

What It Will Take to Fix the Crisis

Most economists agree that real, lasting improvement will require a significant increase in housing supply particularly in affordable categories. That means incentivizing builders to produce smaller, lower-cost homes, streamlining local permitting processes, and investing in infrastructure that supports new developments in growing areas.

Some policymakers are proposing expanded tax credits for first-time buyers, down-payment assistance programs, and targeted subsidies for builders who produce below-market housing. Others are calling for zoning reform to open up suburban areas to multi-family construction and accessory dwelling units (ADUs).

Still, experts caution that these changes take time.

“Even if we start building more affordable homes today, it will take years for supply to catch up,” said Santos. “In the meantime, falling rates are helpful but they’re not a magic fix. The affordability crisis runs deeper than that.”

The Bottom Line

Mortgage rates may finally be drifting lower, but the real barrier to homeownership isn’t borrowing costs—it’s home prices. Without a meaningful expansion in affordable housing supply, millions of Americans will remain on the sidelines, watching prices climb faster than wages.

For now, the dream of homeownership is slipping further out of reach for many middle-class families, and no amount of short-term rate relief can change that overnight.

Until the market finds a balance between demand, supply, and affordability, the so-called housing recovery will remain uneven good news for existing homeowners, but another setback for those still waiting to buy their first home. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses