Stan Middleman on AI, Mortgage Rates, and Why 2026 Could Be a Turning Point

Freedom Mortgage CEO Stan Middleman has watched the mortgage industry move through decades of change. Since launching Freedom Mortgage in 1990, he has led the company through booms, downturns, and everything in between becoming one of the nation’s largest nonbank lenders and servicers along the way. Middleman has also held board positions with the MBA, Fannie Mae, Freddie Mac, and other key housing groups.

Earlier this year, Middleman described 2025 as a “wait-and-see” period. As the year winds down, he says the industry performed largely as expected but 2026 may bring a different set of challenges and opportunities. In this discussion, he explains how AI could affect unemployment and interest rates, why affordability may not get better anytime soon, and what lenders should be preparing for as a new market cycle approaches.

2025 Played Out as Expected

Middleman says the year unfolded almost exactly as he predicted back in March.

“Nothing really moved much,” he said. “We expected rates to be a little lower by year-end, and that’s what happened. It sets the stage for a small improvement next year.”

The market stayed steady, with limited rate swings and predictable volume. But as Middleman notes, the environment is beginning to shift heading into 2026.

How AI Could Push Rates Lower in 2026

Mortgage rates held stable throughout 2025, and Middleman expects some downward pressure early in 2026 depending on what happens in the job market.

He points to Amazon’s recent large-scale layoffs as a possible early sign of AI-related job losses.

“If this is the start of layoffs connected to AI, unemployment could increase,” he explained. “Higher unemployment usually leads to lower interest rates.”

While he doesn’t expect a return to the historic lows of 2020 and 2021, he believes short-term rates could fall by 75 to 100 basis points next year. If unemployment rises sharply, the drop could be even bigger.

Lower short-term rates combined with improving mortgage activity could lift total industry volume to around $2.5 trillion, he said—and possibly close to $3 trillion if AI-related job loss pushes rates even lower.

Affordability: Will 2026 Bring Relief?

Middleman’s view is clear: even if rates fall, affordability may not improve much.

“As interest rates go lower, prices rise,” he said. “Those two numbers work against each other.”

He doesn’t expect a major change in supply. Without a surge in available homes, lower mortgage rates are likely to push prices higher, keeping affordability tight.

“Property prices will rise, and affordability won’t improve. In fact, it could get slightly worse,” he added.

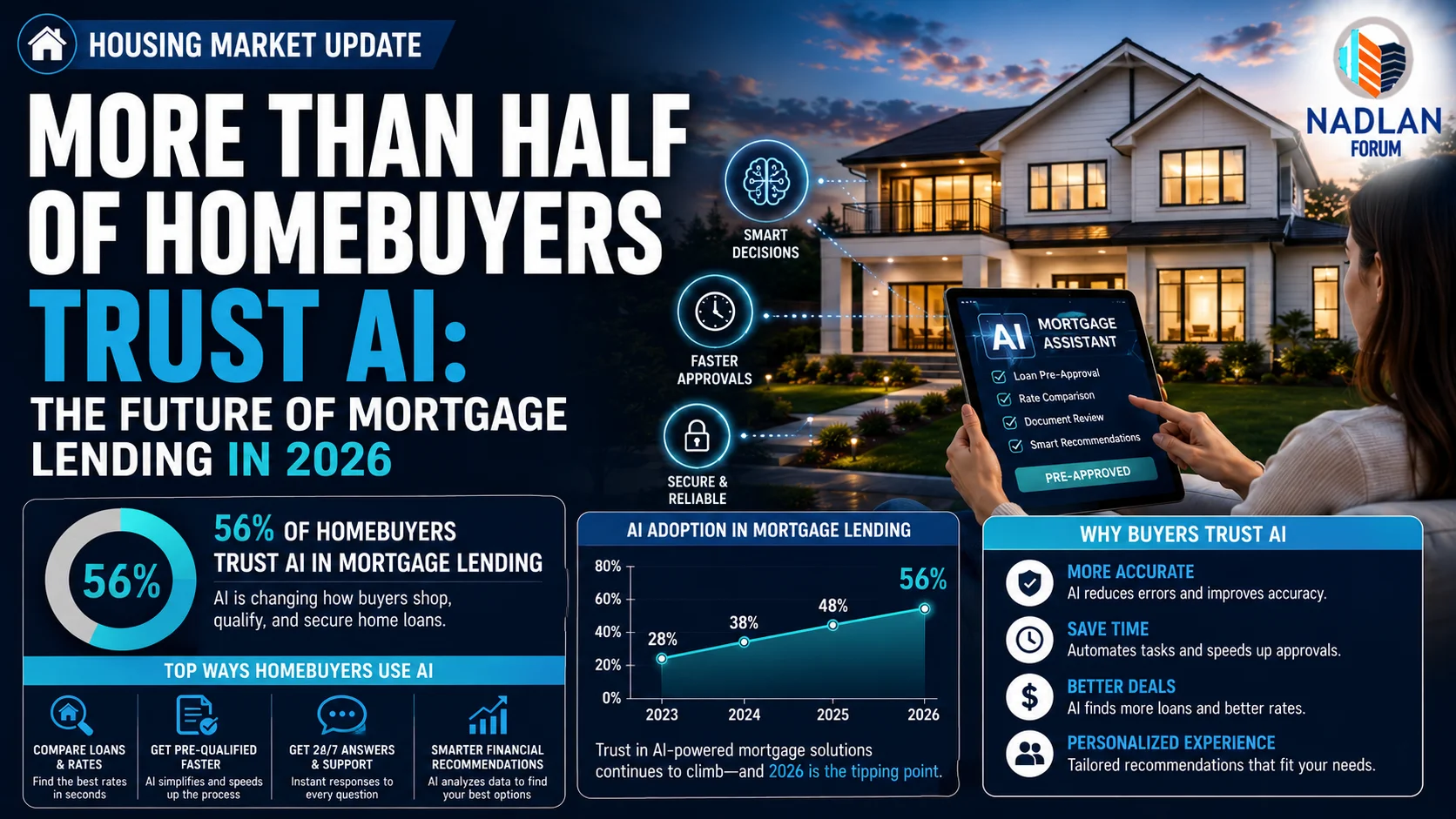

How AI and Data Will Shape Borrower Service

Middleman sees a major technology shift coming in 2026, especially in servicing and customer communication.

“The speed at which data moves, the access to that data, and our ability to explain it to customers all of that improves next year,” he said.

Routine tasks should become simpler and faster, improving the borrower experience. Even complex servicing issues, which fall into the “exception” category, should become easier to identify and resolve.

He believes 2026 will mark a meaningful step forward in customer satisfaction and service accuracy.

How Politics Could Influence Housing in 2026

With another heated election year approaching, Middleman says policy shifts could play an important role.

He credits the current administration’s deregulation efforts with improving conditions for lenders.

“If the administration keeps control of Congress, more deregulation and more pro-business policies are possible,” he said.

But political outcomes could shift quickly and bring uncertainty with them.

Risks and Opportunities Lenders Should Watch

Middleman believes 2026 will not be the year risks peak but the early warning signs may start showing.

“The seeds of future problems are planted now,” he said.

He points specifically to products tied to private securitization such as non-QM loans, second mortgages, and CLOs. By 2027 and 2028, he expects liquidity pressure to rise for these products.

“I’m concerned about liquidity in the broader market for products that rely on private-label securitization,” he noted.

On the opportunity side, he believes tech improvements and lower rates could give lenders a healthier market and more volume next year.

Competition: More Scale Coming to Nonbanks

Nonbanks continue to expand, and Middleman expects that trend to continue especially if banks remain cautious due to regulation.

“If banks stay on the path they’re on, nonbanks will keep gaining scale,” he said. “The largest nonbank players with strong technology and efficient operations will have the advantage.”

One Lesson From 2025: Stop Hitting Snooze

If he had to sum up the biggest takeaway from the past year, Middleman says it’s simple:

“Wake up. We have to pay attention.”

He expects mortgage activity to rise by as much as 20% next year. That means lenders who prepare now rather than waiting for conditions to improve will be positioned to benefit.

“The alarm went off,” he said. “It’s time to get back to work.” For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses