Why the Latest Fed Rate Cut Didn’t Matter for Mortgage Rates—Again

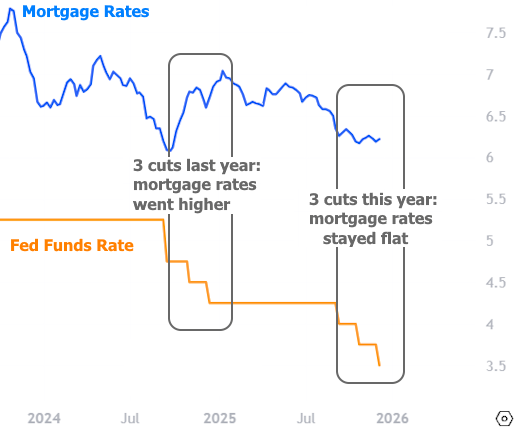

Once again, the Federal Reserve cut interest rates and once again, mortgage rates didn’t benefit. By the end of Friday, mortgage rates were back near the highest levels of the week, closing out another stretch where borrowers saw no relief despite a Fed move.

This outcome continues to challenge one of the most common myths in housing finance: that Fed rate cuts automatically lead to lower mortgage rates. They don’t and this week was another clear example.

The Simple Truth About Fed Cuts and Mortgages

For those who don’t want a deep dive, here’s the short version:

Fed rate cuts and mortgage rates are not the same thing.

The Fed Funds Rate applies to loans that last less than one day.

Mortgage rates apply to loans that last up to 30 years.

Rates tied to very short-term borrowing behave very differently from rates tied to long-term lending. Inflation expectations, economic growth, and investor demand matter far more for mortgage rates than the Fed’s overnight target.

Timing Matters Even More Than Policy

Even if Fed policy and mortgage rates were closely linked, timing still breaks the connection.

- The Fed meets only eight times a year

- Mortgage rates change every day

Because markets usually know what the Fed will do well in advance, mortgage rates often move before a Fed decision is announced. By the time the Fed actually cuts rates, markets have already priced it in.

In fact, every Fed rate cut in 2025 was viewed as more than 90% likely in the days leading up to the announcement. This week was no different. As a result, the market reaction stayed well within the normal trading range for long-term rates.

Markets See Few Cuts Ahead

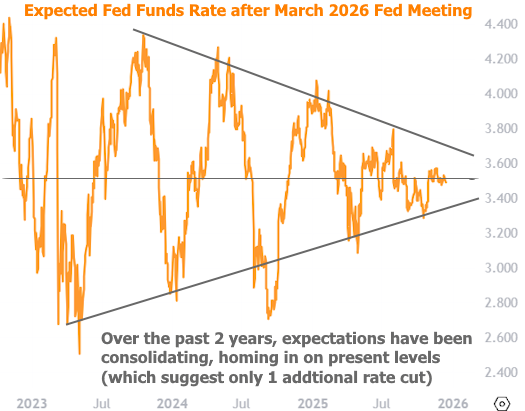

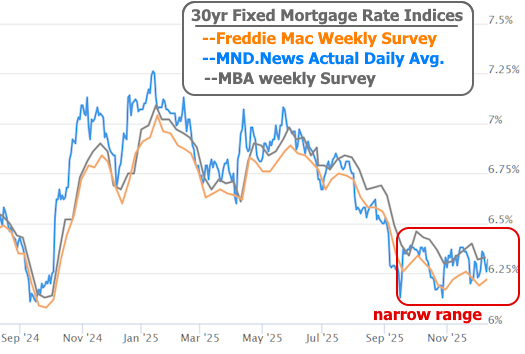

Another reason the Fed’s move didn’t matter much is that the future path of rates is becoming clearer—and narrower.

Markets now expect only one more rate cut by early 2026. That outlook has been forming for months and has become more settled over the past three months.

As expectations tighten, rate movements also tighten. This has led to a narrow trading range for both:

- U.S. Treasury yields

- Mortgage rates

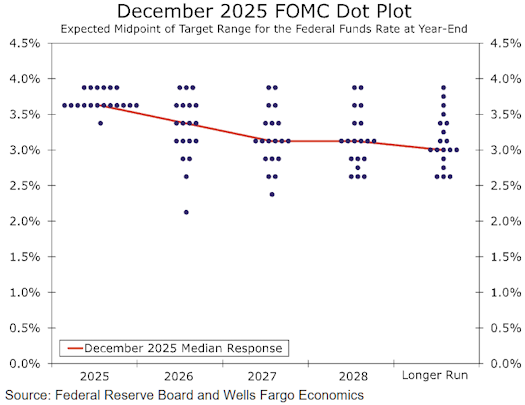

The Fed’s own projections support this view. Its updated dot plot shows that the median Fed official expects just one more cut in 2026 and possibly one more by 2028.

So What Actually Matters for Rates Now?

At this point, Fed decisions are mostly old news. What matters next are developments that markets cannot predict in advance.

The biggest upcoming drivers include:

- November jobs report (delayed due to the shutdown)

- November Consumer Price Index (CPI)

- Any major changes in fiscal policy or economic conditions

If the jobs data shows clear labor market weakness, markets may price in a higher chance of future cuts, which could push long-term rates lower. But that move could be offset if inflation data comes in hotter than expected.

Think of it like two coin flips:

- If both reports point the same way, rate moves could be stronger

- If one supports lower rates and the other doesn’t, they may cancel each other out

Clearing Up Confusion About Fed Bond Buying

There has also been confusion around the Fed’s announcement regarding bond purchases. Some have labeled it quantitative easing (QE) and assumed it would push mortgage rates lower. That is not correct.

True QE floods the financial system with excess liquidity to force lending and drive long-term rates down. That is not what the Fed announced.

Instead, the Fed is acting to prevent liquidity from shrinking too much as banks absorb growing amounts of short-term Treasury debt. If reserves drop too far, lending becomes harder, volatility rises, and rates can spike.

To avoid that, the Fed plans to buy just enough short-term Treasuries to keep the system running smoothly. This move helps prevent rates from rising unnecessarily but it is not designed to push them lower.

Importantly, this step was expected and discussed by the Fed for more than a year. Markets had already planned for it.

What This Means for Borrowers

The takeaway is simple:

Don’t expect Fed rate cuts to lower mortgage rates on their own.

Mortgage rates will move based on inflation data, labor market trends, and investor sentiment not headlines about Fed meetings. Anyone claiming certainty about where rates go next is guessing.

For borrowers, the best strategy remains the same: focus on personal timing, budget, and long-term plans not predictions that rarely pan out. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses