Consumer Anxiety Is the Missing Piece in the 2026 Housing Recovery

On paper, the U.S. housing market is entering 2026 with better fundamentals. Mortgage rates have eased from recent highs, housing inventory is finally expanding, and affordability metrics are showing early signs of relief. So why does the recovery still feel fragile?

The answer lies not in housing data, but in household psychology.

A new nationwide consumer survey from Bright MLS reveals a troubling disconnect: while conditions for buying a home are slowly improving, Americans are increasingly worried about their personal finances. Concerns about debt, everyday expenses, and job security are shaping behavior and potentially holding back housing demand just as the market is poised to rebound.

If people don’t feel financially secure, will they really take on a 30-year mortgage? And if they hesitate, what does that mean for housing in 2026?

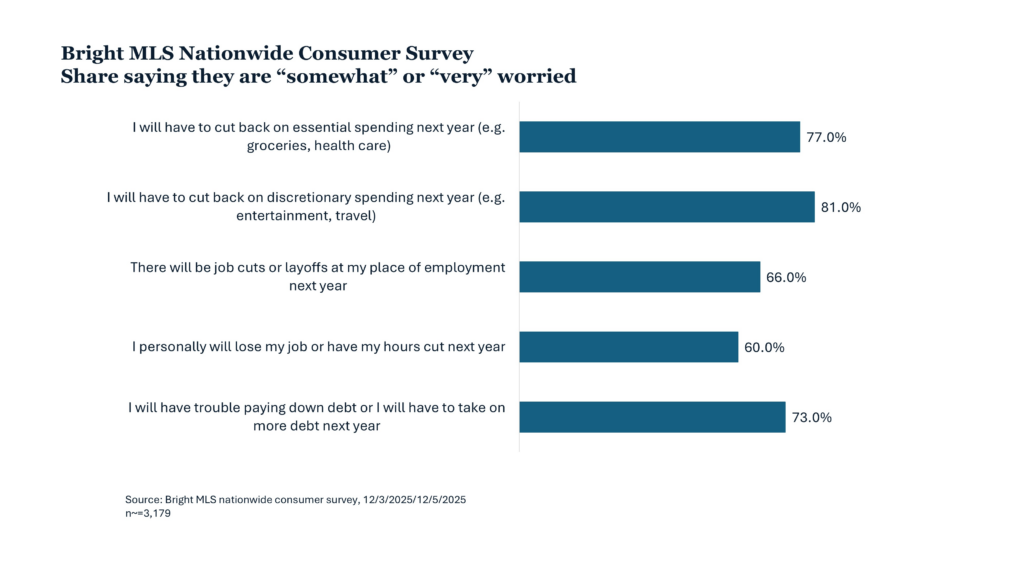

Key Highlights From the Bright MLS Consumer Survey

The December survey, which included more than 3,300 U.S. adults aged 18 and older, paints a picture of broad-based financial unease that cuts across income levels, age groups, and housing status.

Here are the most important takeaways:

- Widespread financial anxiety: A majority of Americans report being concerned about their personal financial situation heading into 2026.

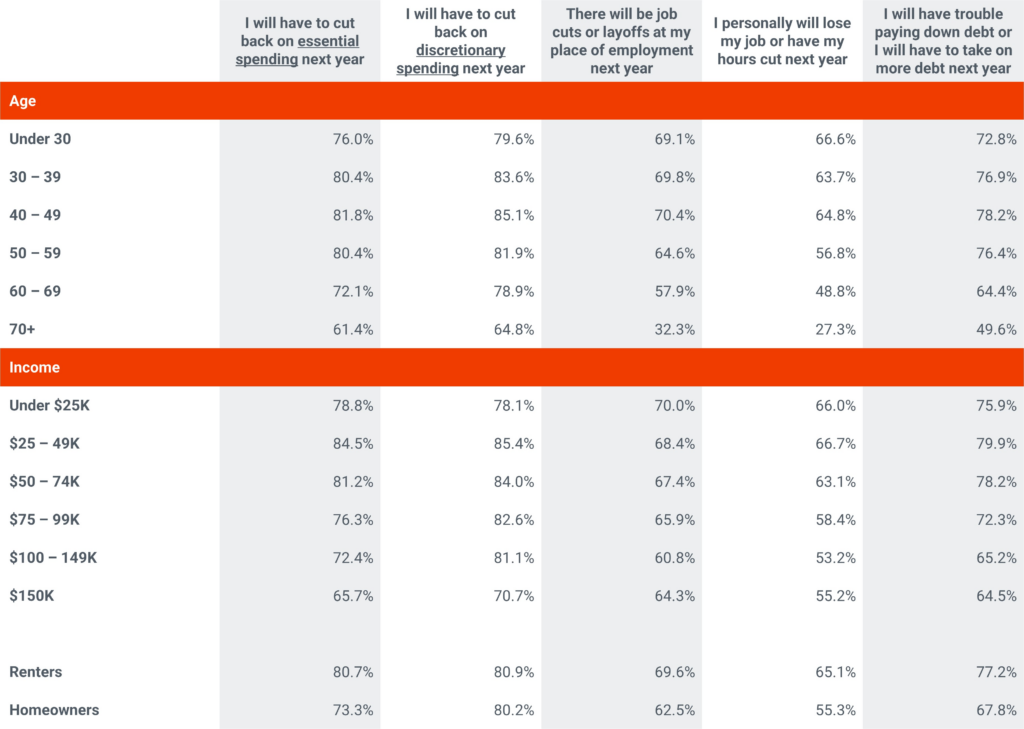

- Renters feel more pressure than homeowners: Renters consistently report higher stress levels around spending, debt, and financial stability.

- Lower-income households are struggling most: Households earning under $50,000 show significantly higher concern than higher-income households.

- Millennials carry heavy economic baggage: Adults aged 30–49 report the highest levels of anxiety, especially around debt and essential expenses.

- Job security fears are rising: Nearly two-thirds of respondents worry about layoffs or reduced hours in the next 12 months.

- Spending pullback is likely: More than 80% expect to cut back on discretionary spending, and over 77% fear reducing spending on necessities.

With consumer spending representing roughly 70% of U.S. GDP, these findings have implications far beyond housing alone.

Why Financial Stress Is So High Right Now

At first glance, the level of concern may seem surprising. Inflation has cooled compared to its peak, unemployment remains relatively low, and interest rates are no longer climbing. So what’s driving the anxiety?

The reality is that households are still dealing with the aftereffects of several major economic shocks.

Rising prices over the past few years permanently reset household budgets. Many Americans took on higher debt to maintain their standard of living during inflationary periods, and those balances haven’t disappeared. Credit card rates remain elevated, student loan payments have resumed for millions, and rent growth has outpaced income gains in many markets.

Even modest financial improvements don’t feel reassuring when families are already stretched thin.

Have you noticed how even small expenses now feel harder to absorb? That’s the psychological impact of prolonged cost pressure and it matters.

Renters vs. Homeowners: A Growing Divide

One of the most striking findings from the survey is the gap between renters and homeowners.

Nearly 80% of renters say they are concerned about having to reduce spending on necessities, compared with about 73% of homeowners. Renters are also significantly more worried about taking on additional debt in the coming year.

This matters because renters represent the future buyer pool. If they feel financially squeezed today, they’re less likely to save for a down payment tomorrow.

For many renters, rising rents, limited savings, and economic uncertainty create a psychological barrier to homeownership — even if mortgage rates fall further. Will lower monthly payments be enough to overcome fear of job loss or mounting debt?

Income Inequality Shapes Housing Demand

The survey also highlights how uneven the financial strain has become.

Households earning under $50,000 annually show the highest levels of concern across nearly every category:

- Over 80% worry about cutting back on essential spending

- Nearly 78% fear taking on more debt

- A majority express uncertainty about their ability to manage future expenses

In contrast, households earning $100,000 or more report noticeably lower anxiety levels, though concern is still widespread.

This divergence suggests that housing demand in 2026 may remain strongest at the higher end of the market, while entry-level and first-time buyer segments continue to struggle.

Is this why starter home activity still feels muted in many regions?

Millennials: The Most Economically Exhausted Generation

Adults aged 30 to 49 a group dominated by older Millennials report the highest stress levels of all age cohorts.

More than 80% in this age group are concerned about reducing spending on necessities, and nearly 78% worry about taking on additional debt or paying down existing balances.

This group has faced repeated economic disruptions at critical life stages:

- Entering the workforce during the Great Recession

- Navigating career and family growth during the COVID-19 pandemic

- Now confronting renewed uncertainty while trying to buy or upgrade homes

By the time many Millennials are finally financially ready to purchase, confidence has been eroded. How willing are they to stretch financially when recent history suggests stability can vanish quickly?

Job Security: The Silent Housing Market Risk

Housing decisions are deeply tied to employment confidence. Even if mortgage rates drop another half-point, buyers won’t move forward if they fear layoffs.

According to the survey:

- 66% of respondents are concerned about potential layoffs at their employer

- 60% worry about losing their job or having their hours reduced

While layoffs haven’t surged nationally, slower job growth and high-profile corporate cuts are shaping perception. Media headlines often matter as much as data when it comes to consumer sentiment.

If buyers think their income might be at risk, they pause and housing activity slows.

What This Means for Investors and Borrowers

This environment creates both challenges and opportunities, depending on perspective.

For borrowers:

Lower rates alone may not be enough to drive action. Borrowers are prioritizing financial resilience, liquidity, and flexibility. Adjustable strategies, conservative budgeting, and long-term planning are becoming more important than timing the absolute bottom in rates.

For investors:

A cautious consumer often means slower transaction volume, but also reduced competition. Markets with strong employment bases, diversified economies, and rental demand may outperform national averages.

Investors should also watch renter sentiment closely. If renters remain under financial pressure, rental demand could stay elevated longer supporting multifamily and build-to-rent strategies.

Are you positioned for steady, patient growth rather than rapid appreciation?

Why 2026 May Be a Year of “Selective Recovery”

The Bright MLS survey reinforces a key theme emerging across housing data: recovery won’t be uniform.

Some markets will rebound faster due to strong job growth and income stability. Others may lag as consumer anxiety limits mobility and risk-taking.

Lower mortgage rates and increased inventory will bring buyers back — but slowly. Confidence takes longer to rebuild than affordability.

This means 2026 is likely to reward disciplined decision-making rather than aggressive speculation.

Conclusion: Housing Moves at the Speed of Confidence

The U.S. housing market doesn’t just respond to rates and supply it responds to how people feel about their financial future.

Right now, many Americans feel cautious, stretched, and uncertain. Until that changes, housing activity will remain measured, even as conditions improve.

At Nadlan Capital Group, we believe understanding borrower psychology is just as important as tracking market data. The smartest strategies in 2026 will balance opportunity with realism.

What do you think — will confidence rebound faster than expected, or will caution define this housing cycle? Let us know your thoughts and stay connected with Nadlan Capital Group for data-driven insights that help you move forward with confidence.

Responses