Renting Now Beats Owning in Every Major U.S. City — A Stark Shift in the Housing Math

For decades, buying a home was seen as the financially superior move especially in large U.S. cities where rents climbed relentlessly. That assumption no longer holds.

According to a new nationwide study by LendingTree, renting is now cheaper than owning a home with a mortgage in every large U.S. metro area. Not just in coastal cities or overheated markets but across the board.

The difference isn’t small. On average, homeowners with a mortgage are paying nearly 37% more per month than renters. That growing gap is reshaping household decisions, delaying homeownership, and forcing Americans to rethink what the “right” housing choice really looks like in 2026.

So how did we get here and what does this mean if you’re deciding whether to rent or buy?

The Cost Gap Is Widening, Not Shrinking

LendingTree’s analysis reveals a nationwide affordability shift that has accelerated over the past two years.

Here are the most important findings:

- Homeowners with a mortgage pay 36.9% more per month than renters

- Median monthly rent in 2024: $1,487

- Median monthly housing cost with a mortgage: $2,035

- Monthly gap: $548, or $6,576 per year

- The gap widened by $50 from 2023 to 2024

- Renting is cheaper than owning in all 100 of the largest U.S. metros

- In 22 metros, homeowners pay 50% or more than renters monthly

This is no longer a regional story. It’s a national reset of housing economics.

Why the Cost Difference Keeps Growing

Down payments often get the spotlight when discussing affordability, but they’re just the entry fee. The real divergence happens after the purchase.

Mortgage rates remain elevated compared to pre-2022 levels, pushing monthly payments higher even as home price growth slows. At the same time, homeowners face additional costs renters don’t: property taxes, homeowners insurance, maintenance, repairs, and, in many cases, HOA fees.

Renters, by contrast, face one primary obligation rent with fewer unpredictable expenses.

From 2023 to 2024:

- Median rent rose 5.8%

- Monthly homeownership costs rose 6.9%

That imbalance continues to push the math in favor of renting.

Have you noticed how owning now feels riskier, even if rent isn’t cheap? That perception reflects this widening cost gap.

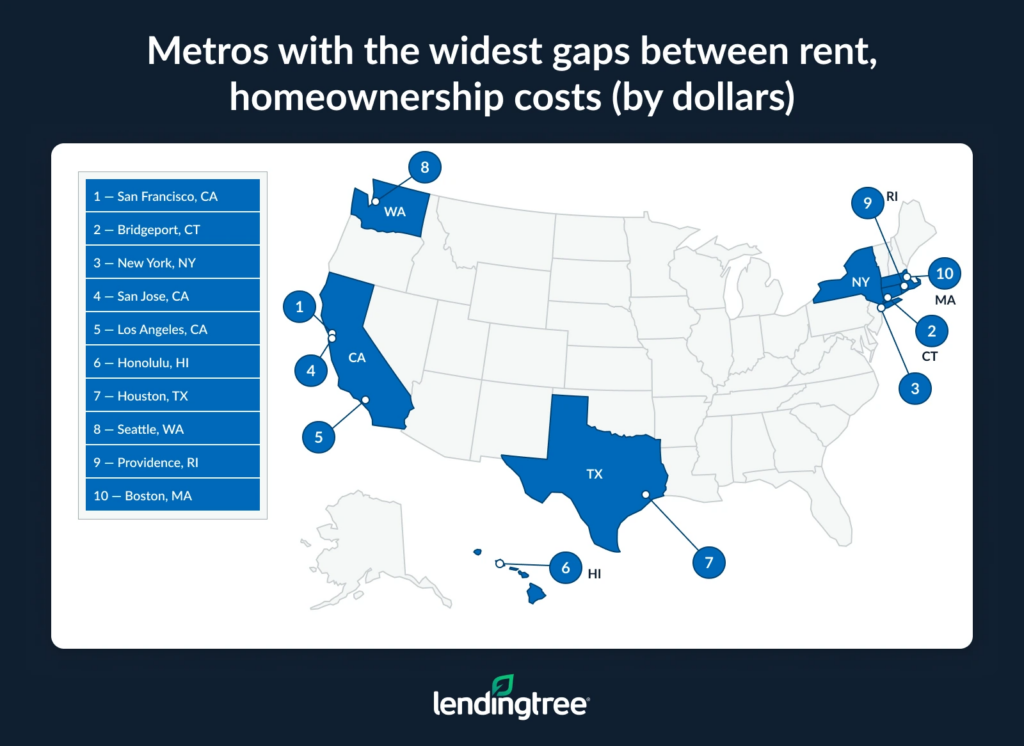

Where Renting Saves the Most Money

While renting is cheaper everywhere, the size of the gap varies dramatically by metro.

Among the 100 largest U.S. metro areas, the biggest differences are concentrated in high-cost coastal and Northeast markets.

The largest monthly gaps:

- San Francisco: $1,565

- Bridgeport, Connecticut: $1,427

- New York City: $1,409

In San Francisco, median rent sits around $2,435, while median monthly homeownership costs exceed $4,000. That’s not a marginal difference — it’s a structural one.

In percentage terms, the widest gaps are found in:

- New York: 76.1%

- Bridgeport: 75.3%

- Providence, Rhode Island: 66.5%

In these metros, owning with a mortgage can cost nearly double renting.

Even the “Affordable” Markets Aren’t Immune

The story doesn’t end with expensive coastal cities.

Even in metros where affordability is traditionally stronger, renting still comes out ahead.

The smallest monthly gaps:

- Phoenix: $184

- Orlando: $257

- Columbia, South Carolina: $271

While those differences are modest compared to San Francisco or New York, they still matter especially for first-time buyers stretching to qualify for a mortgage.

When renting is cheaper even in lower-cost markets, the incentive to delay buying grows stronger.

Is it worth locking into higher monthly payments just to own or does flexibility now have more value?

A Five-Year Look: 2024 Was the Peak Gap

LendingTree’s study examined trends over the past five years, and one thing stands out: 2024 marked the widest gap between renting and owning.

- Highest gap: 2024 ($548/month)

- Lowest gap: 2022 ($475/month)

This suggests that the affordability shock following rate hikes hasn’t fully worked its way out of the system. Even as home prices cool in some markets, financing costs continue to do the heavy lifting.

Until mortgage rates meaningfully decline or incomes rise faster this gap is likely to persist.

Expert Insight: “The Choice Isn’t Just About Money”

Despite the stark math, experts caution against reducing the rent-versus-own decision to a spreadsheet.

Matt Schulz, LendingTree’s chief consumer finance analyst, argues that homeownership still carries non-financial value.

“The choice isn’t just about money,” Schulz explains. “Homebuying can represent accomplishment, security, safety and plenty of other things. There’s a reason why homeownership has long been considered part of the American Dream.”

That emotional and psychological value remains powerful even when the numbers don’t cooperate.

Homeownership and Wealth: Still True, But More Complicated

Traditionally, owning a home has been one of the most reliable ways for Americans to build wealth. Equity accumulation, forced savings, and long-term appreciation have historically favored buyers.

That hasn’t disappeared but the timeline has stretched.

High purchase prices and elevated rates mean it often takes many years before ownership overtakes renting financially. Schulz notes that equity can still be valuable for future financing needs, such as:

- Home renovations

- Starting a business

- Paying off high-interest debt

But those benefits usually require staying put for several years.

If mobility is important, renting may now be the more rational financial choice.

Why More Americans Are Delaying Homeownership

The cost gap is changing behavior — and not subtly.

According to Schulz, Americans are:

- Waiting longer to buy their first home

- Choosing not to move to avoid giving up low-rate mortgages

- Becoming resigned to long-term renting

Some households are even concluding they may never own a home at all.

That shift has ripple effects beyond individual finances. Delayed homeownership influences household formation, consumer spending, labor mobility, and long-term wealth inequality.

What happens to the economy when ownership becomes optional instead of expected?

A Broader Trend: Markets That Flipped

LendingTree’s findings align with broader research across the housing sector.

A separate analysis by InvestorsObserver found that between 2021 and 2025, 39 major U.S. metro areas flipped from markets where buying was cheaper than renting to markets where renting is now the more affordable option.

Importantly, this shift occurred across both red and blue states, underscoring that the trend is structural not political or regional.

The rent-versus-own equation has fundamentally changed.

What This Means for Renters

For renters, the data offers both relief and frustration.

On one hand, renting is currently the cheaper monthly option almost everywhere. On the other hand, it reinforces how difficult it has become to transition into ownership.

Renters may benefit from:

- Lower monthly obligations

- Greater flexibility

- Reduced exposure to maintenance and insurance costs

But they miss out on equity accumulation — unless they invest elsewhere.

Renting now demands a stronger long-term financial plan, not just a housing strategy.

What This Means for Buyers

For buyers, the decision requires sharper clarity.

Owning may still make sense if:

- You plan to stay long-term

- You value stability over flexibility

- You can comfortably absorb higher monthly costs

But buying purely because “renting feels like throwing money away” no longer holds up under scrutiny in many markets.

In 2026, buying a home is more about lifestyle alignment than automatic financial optimization.

What This Means for Investors and Policymakers

For investors, rising rent-to-own gaps support rental demand but also raise affordability concerns. For policymakers, the findings highlight the growing divide between housing access and housing ownership.

Without:

- Increased supply

- Lower financing costs

- Zoning and construction reform

The ownership gap will continue to widen.

This isn’t just a housing issue — it’s a long-term economic one.

Conclusion: Renting Isn’t a Failure — It’s a Rational Choice

The idea that renting is a temporary stop on the way to homeownership is fading. In today’s market, renting is often the financially smarter option not just a compromise.

At Nadlan Capital Group, we believe housing decisions should be grounded in data, personal goals, and long-term planning not outdated assumptions.

Whether you rent or own, the key is intentionality. The market has changed, and strategies must change with it.

Do you think renting will remain cheaper long-term, or is this gap setting the stage for the next housing shift? Share your thoughts with us and stay connected with Nadlan Capital Group for clear, practical insights on navigating today’s housing economy.

Responses