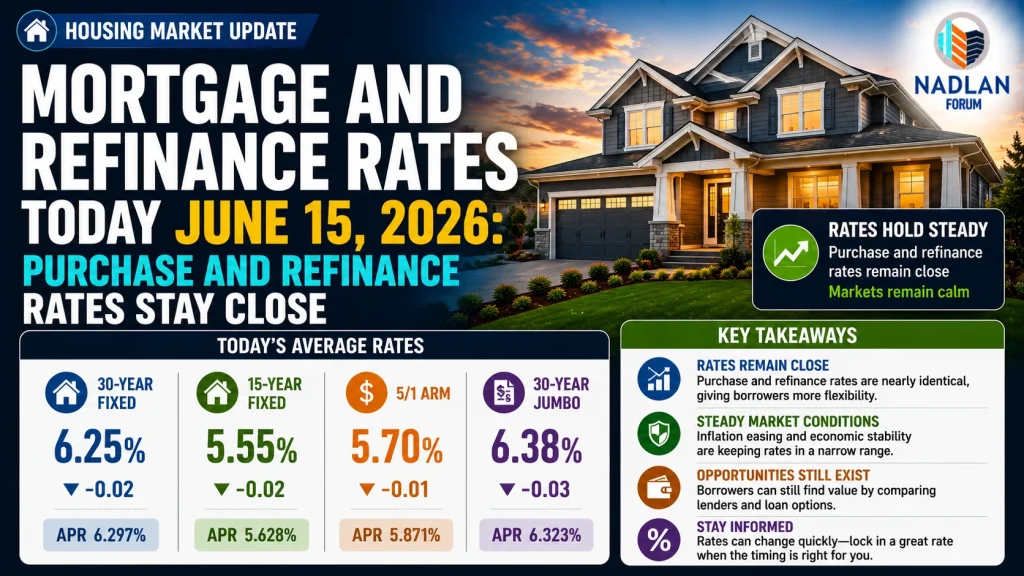

Mortgage and Refinance Rates Today June 15, 2026: Purchase and Refinance Rates Stay Close

Mortgage rates started the week with little movement, giving both homebuyers and homeowners a relatively stable borrowing environment. One of the most notable trends is the narrow gap between purchase and refinance rates, creating opportunities for consumers considering either buying a home or refinancing an existing mortgage.

According to the latest market data, fixed-rate and adjustable-rate mortgages remain near recent levels, while refinance rates are almost identical to purchase loan rates across several major loan products.

Although mortgage rates remain higher than the historic lows seen during the pandemic, recent stability could help borrowers make more confident financial decisions.

Today’s Mortgage Rates

Several popular mortgage products remained competitive.

Current Purchase Mortgage Rates

| Loan Type | Rate |

|---|---|

| 30-Year Fixed | 6.35% |

| 20-Year Fixed | 6.10% |

| 15-Year Fixed | 5.78% |

| 5/1 ARM | 6.30% |

| 7/1 ARM | 6.45% |

| 30-Year VA | 5.82% |

| 15-Year VA | 5.34% |

| 5/1 VA | 5.64% |

The average 30-year fixed mortgage declined slightly, while the 15-year fixed mortgage posted a larger daily improvement.

Current Refinance Rates

Homeowners considering refinancing continue to see competitive pricing.

Current Refinance Mortgage Rates

| Loan Type | Rate |

| 30-Year Fixed | 6.34% |

| 20-Year Fixed | 6.11% |

| 15-Year Fixed | 5.82% |

| 5/1 ARM | 6.25% |

| 7/1 ARM | 6.35% |

| 30-Year VA | 5.79% |

| 15-Year VA | 5.33% |

| 5/1 VA | 5.60% |

One of the most interesting developments is the extremely small difference between purchase and refinance rates.

The average 30-year refinance rate sits just one basis point below the purchase rate, creating a favorable environment for homeowners exploring refinancing opportunities.

Purchase And Refinance Rates Are Nearly Identical

Traditionally, refinance rates are slightly higher than purchase mortgage rates.

Today’s market is different.

Rate Comparison

| Loan Product | Purchase Rate | Refinance Rate |

| 30-Year Fixed | 6.35% | 6.34% |

| 20-Year Fixed | 6.10% | 6.11% |

| 15-Year Fixed | 5.78% | 5.82% |

| 5/1 ARM | 6.30% | 6.25% |

This narrow spread may encourage more homeowners to evaluate refinancing opportunities while helping buyers compare financing options more effectively.

Monthly Payments Remain Manageable Compared With Recent Peaks

While mortgage rates remain elevated compared with pandemic lows, today’s relatively stable environment provides some predictability.

For a typical home purchase priced around $425,000 with a 20% down payment, estimated monthly housing costs remain near $2,600 when taxes and insurance are included.

Monthly payments continue to depend on:

- Home price.

- Down payment.

- Mortgage rate.

- Property taxes.

- Homeowners insurance.

- HOA fees.

- Private mortgage insurance when applicable.

30-Year Mortgage Remains The Most Popular Option

The 30-year fixed mortgage continues to dominate the housing market.

Advantages

- Lower monthly payments.

- Fixed interest rate.

- Predictable budgeting.

- Greater financial flexibility.

Disadvantages

- Higher total interest costs.

- Longer repayment period.

- Slightly higher interest rates than shorter-term loans.

For many households, lower monthly payments remain the primary advantage.

15-Year Mortgages Offer Long-Term Savings

Borrowers looking to reduce total borrowing costs often consider 15-year loans.

Benefits

- Lower interest rates.

- Faster equity growth.

- Earlier mortgage payoff.

- Lower lifetime interest expenses.

Challenges

- Higher monthly payments.

- Reduced monthly cash flow flexibility.

A shorter loan term may work well for borrowers with stable incomes and long-term ownership plans.

Adjustable-Rate Mortgages Continue To Compete

Adjustable-rate mortgages remain an option for certain buyers.

A 5/1 ARM offers a fixed rate for five years before annual adjustments begin.

ARM Advantages

- Lower initial rates in some market conditions.

- Reduced early monthly payments.

- Attractive for shorter ownership periods.

ARM Risks

- Future payment uncertainty.

- Potential rate increases.

- Higher long-term borrowing costs.

Borrowers should compare adjustable and fixed-rate products carefully before making decisions.

How To Secure A Lower Mortgage Rate

Several factors influence mortgage pricing.

Improve Credit

Higher credit scores generally qualify for better rates.

Increase Down Payment

Larger down payments reduce lender risk.

Lower Debt

Reducing debt-to-income ratios can improve loan pricing.

Compare Multiple Lenders

Shopping around often produces meaningful savings.

Consider Rate Buydowns

Borrowers can pay discount points to permanently reduce interest rates.

Temporary Rate Buydowns Gain Popularity

Temporary buydowns have become increasingly common in today’s market.

A typical 2-1 buydown works like this:

Example

| Year | Interest Rate |

| Year 1 | 4.25% |

| Year 2 | 5.25% |

| Remaining Loan | 6.25% |

These programs reduce initial payments but require additional upfront costs.

Borrowers should calculate whether long-term savings justify the investment.

Will Mortgage Rates Fall Later This Year?

Most housing economists expect mortgage rates to remain relatively stable during 2026.

Current Forecasts

| Organization | 2026 Outlook |

| MBA | 6.4% – 6.5% |

| Fannie Mae | Around 6.3% |

Future movements will depend on:

- Inflation.

- Federal Reserve policy.

- Treasury yields.

- Employment data.

- Consumer spending.

- Global economic events.

What This Means For Homebuyers

Stable mortgage rates help buyers plan purchases with greater confidence.

Moderating home price growth and improving inventory in many markets are also creating additional opportunities.

Buyers may benefit from:

- Better negotiations.

- Seller concessions.

- More inventory choices.

- Financing flexibility.

What This Means For Homeowners

The small difference between purchase and refinance rates may encourage homeowners to explore refinancing options.

Potential benefits include:

- Lower monthly payments.

- Shorter loan terms.

- Fixed-rate conversions.

- Home equity access.

Each homeowner should compare potential savings with refinancing costs.

Key Mortgage Market Numbers

Purchase Rates

| Product | Rate |

| 30-Year Fixed | 6.35% |

| 15-Year Fixed | 5.78% |

| 5/1 ARM | 6.30% |

Refinance Rates

| Product | Rate |

| 30-Year Fixed | 6.34% |

| 15-Year Fixed | 5.82% |

| 5/1 ARM | 6.25% |

Bottom Line

Mortgage and refinance rates remained remarkably close on June 15, 2026, creating opportunities for both homebuyers and homeowners. The average 30-year purchase mortgage stood at 6.35%, while the comparable refinance rate was just one basis point lower.

Stable borrowing costs, combined with improving housing inventory and moderating home price growth in many markets, may help support housing activity during the remainder of the year. Although mortgage rates remain above the historic lows of recent years, today’s environment offers greater predictability for borrowers making important financial decisions.

Whether purchasing a home or refinancing an existing mortgage, comparing multiple lenders, evaluating loan products, and understanding long-term costs remain essential steps for securing the best financing available. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses