Mortgage Interest Savings by Credit Score: Why 760 Matters for Homebuyers

A new nationwide study highlights how credit scores play a major role in home affordability. According to research from AD Mortgage, improving a borrower’s credit score can lead to significant savings on mortgage interest over the life of a loan.

The study, titled “Credit Score vs. Mortgage Cost: How Long It Takes to Improve and How Much It Can Save”, examined credit data across all U.S. states and analyzed how different credit scores influence mortgage rates and borrowing costs.

The findings show that even small improvements in a borrower’s FICO score can reduce mortgage interest costs by tens of thousands of dollars during a typical 30-year home loan.

Why a 760 Credit Score Matters for Mortgage Rates

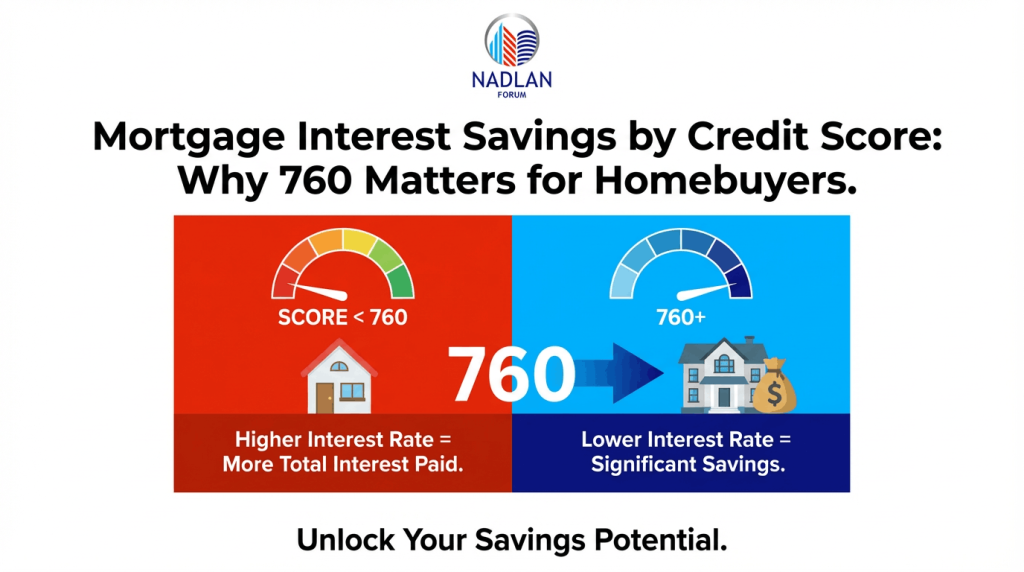

In the mortgage industry, a 760 FICO score is widely considered the threshold for accessing the most competitive mortgage rates.

Borrowers who reach this credit level typically qualify for lower interest rates, which can significantly reduce monthly payments and total interest paid over time.

According to the study, homeowners across the United States can save between $10,000 and $46,000 in interest costs over the life of a mortgage simply by improving their credit score to 760.

However, the exact savings depend heavily on location, home prices, and loan size.

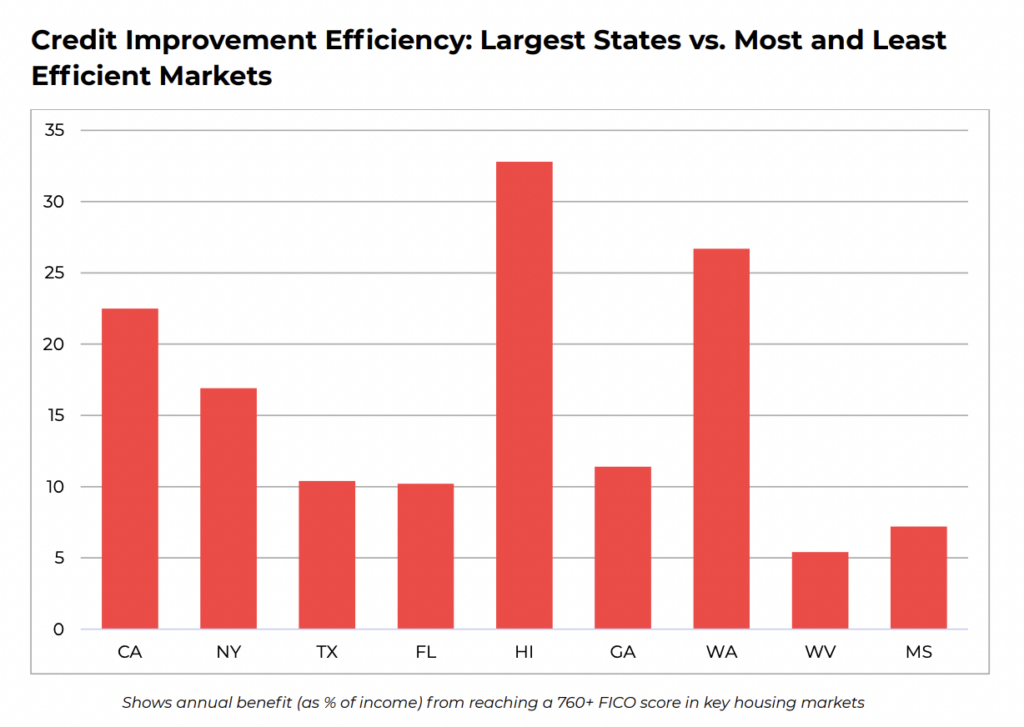

State Differences in Mortgage Interest Savings

The financial benefits of improving credit scores vary widely across states because of differences in housing prices and loan amounts.

In higher-cost housing markets, such as California and Hawaii, the impact of lower interest rates becomes much more noticeable.

For example:

- California: Borrowers can save about $42,753 in total mortgage interest by raising their credit score to 760.

- Texas: Borrowers may save around $26,881, though the relative penalty for having a lower score is higher.

In Texas, borrowers with credit scores below 760 can pay more than 10.7% of the total loan value in additional interest, making it one of the states where credit score penalties are most noticeable relative to loan size.

States With the Highest Potential Mortgage Savings

States with higher home values tend to show the largest total savings from improved credit scores because mortgage balances are larger.

The study found that some of the states offering the highest potential savings include:

- Hawaii

- California

- Massachusetts

In these markets, even a small interest rate difference can translate into tens of thousands of dollars in long-term savings.

For borrowers purchasing expensive homes, improving their credit score can have a major impact on overall affordability.

States With the Biggest Credit Score Penalties

In some states, the financial penalty for not having a high credit score is particularly large.

States where borrowers face the steepest mortgage rate penalties for scores below 760 include:

- Alabama

- Mississippi

- Georgia

- Louisiana

- Texas

In these regions, borrowers may end up paying more than 10% of their loan amount in extra interest if their credit score falls below the top tier.

This means that even though home prices may be lower, weaker credit profiles can still significantly affect total borrowing costs.

How Long It Takes to Improve a Credit Score

The study also examined how long it typically takes borrowers to improve their credit score enough to qualify for better mortgage rates.

For many Americans, raising a credit score to 760 takes between 18 months and three years.

However, the timeline can vary depending on factors such as:

- Existing credit history

- Debt levels

- Payment behavior

- Local average credit scores

In states where the average credit score is lower, it may take longer for borrowers to reach top-tier levels.

Credit Scores and Household Income

Another important finding from the study is how credit score improvements affect affordability when measured against local household income.

In high-cost states such as Hawaii and California, the savings from achieving a 760 credit score can equal more than 40% of a typical household’s yearly income.

This means that improving credit can significantly increase purchasing power, especially in expensive housing markets where mortgage payments represent a large share of income.

How Credit Scores Affect Homebuying Power

The research highlights a key reality of the housing market: two buyers with similar incomes can have very different purchasing power depending on their credit scores.

Even a 20- to 30-point difference in FICO score can affect mortgage rates enough to change how much a borrower can afford.

Lower interest rates reduce monthly payments and allow buyers to qualify for larger loans. On the other hand, higher rates can limit the price range buyers can consider when shopping for a home.

Because of this, credit preparation has become an essential step for anyone planning to purchase a home.

Steps Borrowers Can Take to Improve Credit

For potential homebuyers, improving a credit score before applying for a mortgage can make a significant financial difference.

Common steps that help raise credit scores include:

- Paying bills on time

- Reducing credit card balances

- Avoiding new debt before applying for a mortgage

- Checking credit reports for errors

- Maintaining long-standing credit accounts

Lenders often recommend preparing credit profiles well before starting the homebuying process, since improvements can take time to appear on credit reports.

What the Study Means for Future Homebuyers

The results of the credit score study show that credit preparation is one of the most effective ways to reduce mortgage costs.

While housing prices and interest rates are influenced by market conditions, credit scores remain one factor that borrowers can actively improve.

By raising their credit score before applying for a mortgage, buyers may increase their purchasing power and potentially save tens of thousands of dollars over the life of a home loan.

As housing affordability continues to challenge many buyers, strengthening credit profiles may become an increasingly important step for those hoping to enter the housing market. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses