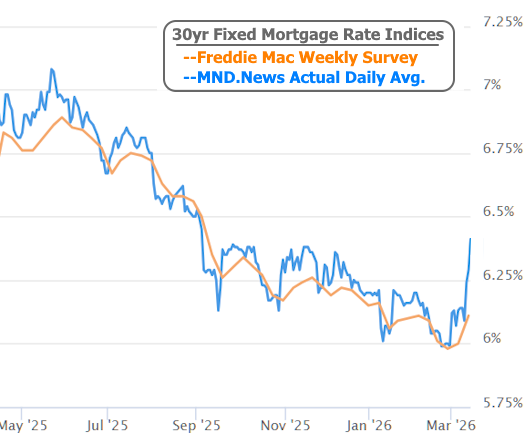

Mortgage Rate Trends 2026: From 3-Year Lows to 7-Month Highs in Just Two Weeks

Mortgage interest rates experienced a sharp reversal in early March, shifting from multi-year lows to their highest levels in several months within a short period of time. At the end of February, average 30-year mortgage rates were at the lowest point in more than three years, providing temporary relief for homebuyers.

However, in the weeks that followed, borrowing costs increased rapidly. By mid-March, mortgage rates had climbed to seven-month highs, reflecting major changes in global financial markets.

The sudden shift highlights how sensitive mortgage rates are to economic conditions, global events, and movements in the bond market.

Mortgage Rates Rise Quickly After February Lows

The final days of February brought encouraging news for potential homebuyers as mortgage rates declined to levels not seen in several years.

But the improvement was short-lived. Since the beginning of March, rates have steadily increased, creating one of the fastest reversals in the mortgage market in recent months.

Such quick changes are not unusual when major economic events affect investor expectations about inflation, interest rates, and global trade.

Mortgage rates typically follow the direction of long-term Treasury yields, which respond rapidly to global financial developments.

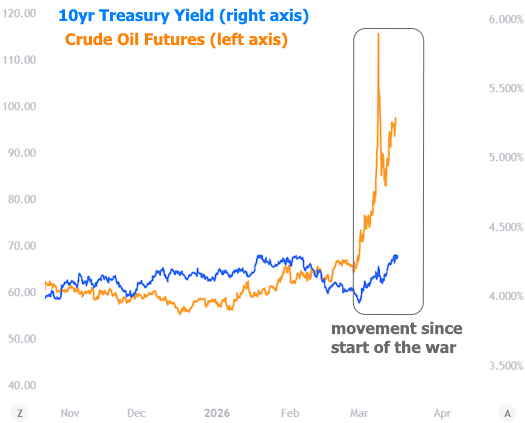

Oil Prices and Inflation Expectations Push Rates Higher

A major factor behind the rise in mortgage rate trends in 2026 is the increase in global energy prices.

Geopolitical tensions in the Middle East have led to a surge in oil prices. Because oil plays a key role in transportation and manufacturing costs, rising energy prices often lead to expectations of higher inflation.

When investors anticipate inflation, they typically demand higher returns on bonds. This causes bond yields to rise, which ultimately pushes mortgage interest rates higher.

In simple terms, when energy prices increase quickly, the financial markets often assume that the cost of goods and services will increase as well.

Why Oil Prices Affect Interest Rates

Oil prices influence the economy in several important ways.

Energy is used in transportation, manufacturing, agriculture, and supply chains around the world. When oil becomes more expensive, companies often face higher operating costs.

These increased costs can eventually lead to higher prices for consumers, contributing to inflation.

Because mortgage rates are closely linked to long-term inflation expectations, sudden increases in oil prices can push interest rates higher even before inflation appears in official data.

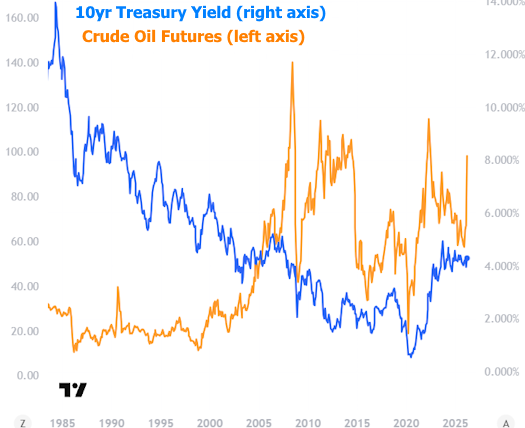

Oil and Interest Rates Do Not Always Move Together

Although oil prices and interest rates often move in the same direction during periods of rising inflation expectations, the relationship between the two is not always consistent.

Both oil prices and interest rates are influenced by broader economic conditions such as:

- Global economic growth

- Currency movements

- Supply chain disruptions

- Central bank policies

Sometimes these factors push oil prices and interest rates in opposite directions. For example, a strong U.S. dollar can lower commodity prices while still contributing to higher interest rates.

Because of this complexity, short-term correlations between oil and rates should be interpreted carefully.

Additional Factors Influencing Mortgage Rates

While rising energy prices are currently the dominant driver of interest rate changes, several other forces may also be influencing the bond market.

These include:

- Inflation expectations

- Global economic uncertainty

- Investor demand for government bonds

- Supply chain disruptions in key industries

Analysts note that once energy markets stabilize, it will become easier to determine how much these other factors are contributing to rate movements.

For now, oil prices remain one of the most visible drivers of the recent increase in borrowing costs.

Why Rates May Not Fall Immediately

Even if geopolitical tensions ease and energy prices decline, mortgage rates may not immediately return to their previous lows.

Markets tend to assume that inflation pressures created by supply disruptions can persist for several months.

For example, increases in oil, natural gas, or fertilizer prices can affect transportation and food costs over time. These effects may take months to appear in consumer price data.

Because of this delayed impact, investors may remain cautious about purchasing bonds aggressively until inflation indicators show clear improvement.

Role of the Federal Reserve

Some observers wonder whether the Federal Reserve could lower interest rates to counter rising mortgage costs.

However, the Fed primarily controls short-term interest rates, while mortgage rates are influenced by longer-term bond yields.

Even when the Federal Reserve reduces short-term rates, long-term borrowing costs do not always follow immediately.

There have been several instances in recent years where mortgage rates increased even after the central bank implemented rate cuts.

For this reason, the Federal Reserve has limited direct control over mortgage interest rates.

Why Rate Cuts Are Unlikely in the Near Term

The Federal Reserve is scheduled to hold a policy meeting soon, where officials will review inflation data and economic conditions.

However, analysts generally expect that interest rates will remain unchanged in the near term.

Inflation risks linked to rising energy prices make it difficult for policymakers to justify lowering interest rates at the moment.

Central banks typically prefer to see clear signs that inflation is slowing before easing monetary policy.

What Could Help Mortgage Rates Decline

For mortgage rates to move lower again, several economic developments would likely need to occur.

Possible factors that could reduce rates include:

- Lower energy prices

- Reduced inflation pressures

- Slower economic growth

- Increased investor demand for bonds

In many cases, weaker economic activity can lead to lower interest rates as investors seek safer assets like government bonds.

However, such conditions may also bring broader economic challenges.

Housing Market Outlook

The rapid change in mortgage rate trends in 2026 highlights how quickly the housing market can react to global economic events.

Higher borrowing costs can affect both homebuyers and sellers by reducing affordability and slowing housing demand.

At the same time, limited housing supply continues to support home prices in many regions.

As a result, the direction of mortgage rates in the coming months will depend heavily on energy prices, inflation data, and overall economic conditions.

While rates could eventually stabilize or decline, the recent surge suggests that financial markets may remain volatile in the near term. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses