Existing Home Sales March 2026: Market Slows as Inventory Remains Limited

Home Sales Decline Across the U.S.

The U.S. housing market showed signs of slowing in March, as existing-home sales dropped 3.6% compared to the previous month. According to the latest report from the National Association of Realtors, sales activity remains below last year’s levels, reflecting ongoing affordability challenges and cautious buyer behavior.

Economists point to weaker consumer confidence and slower job growth as key factors reducing demand. Even though buyers are still active, many are delaying decisions due to higher borrowing costs and economic uncertainty.

Inventory Shortage Continues to Shape the Market

One of the biggest issues affecting the housing market is the limited number of homes available for sale.

Total housing inventory in March reached 1.36 million units, a modest increase from the previous month. However, supply remains below normal levels, with just a 4.1-month inventory available. A balanced market typically requires closer to a 5- to 6-month supply.

Experts estimate that an additional 300,000 to 500,000 homes would be needed to bring the market closer to equilibrium. Until that happens, buyers will continue to face limited choices and competitive conditions.

Home Prices Continue to Rise

Despite slower sales, home prices are still moving upward due to tight supply.

- Median home price: $408,800 (up 1.4% year-over-year)

- 33 consecutive months of annual price increases

This trend highlights a key imbalance: demand may be cooling slightly, but supply remains too low to push prices down significantly.

Over the past six years, rising home values have added significant wealth for homeowners, with average gains exceeding $100,000. While this benefits current owners, it creates additional barriers for new buyers trying to enter the market.

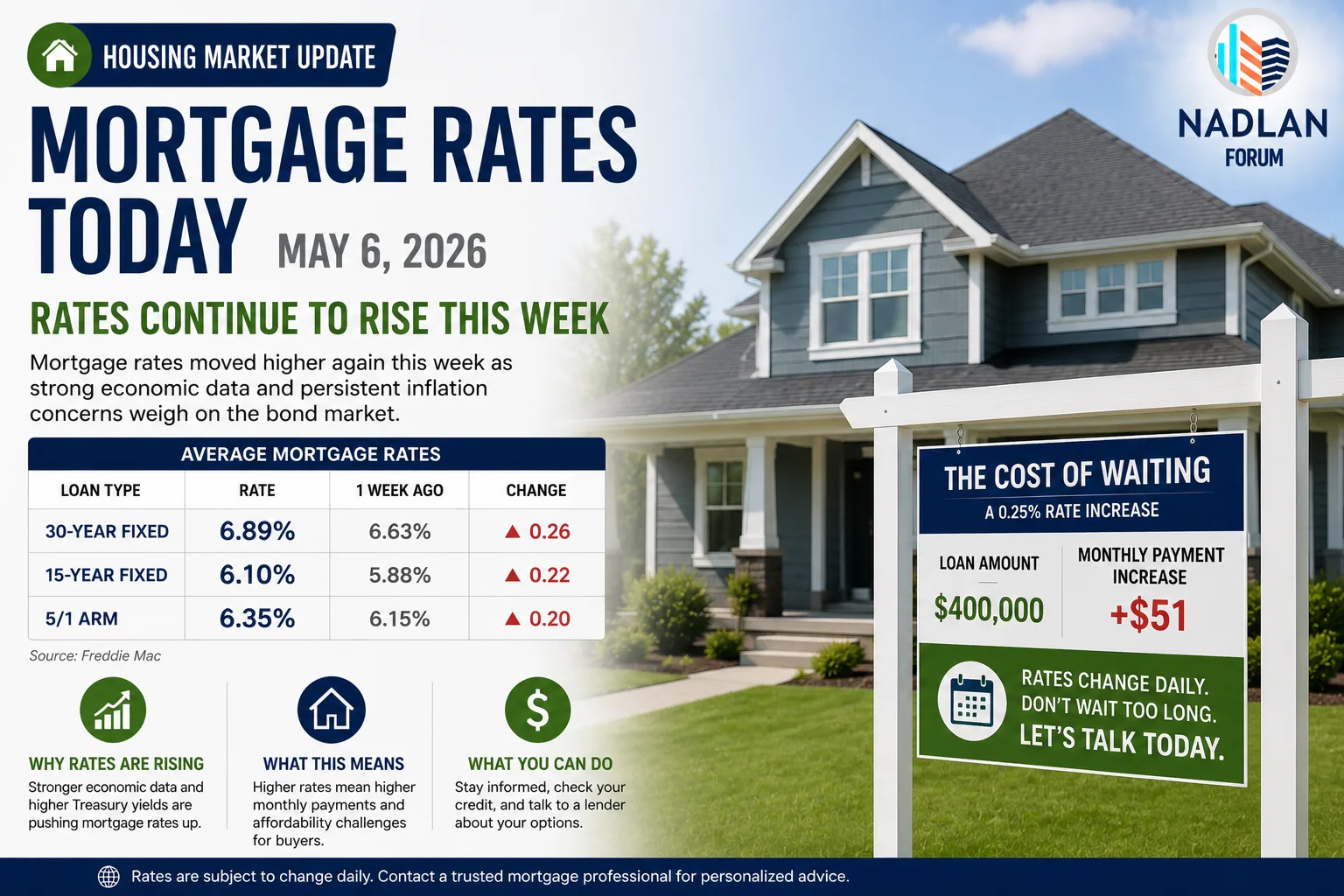

Mortgage Rates Adding Pressure

Borrowing costs are another major factor shaping market conditions. Data from Freddie Mac shows that the average 30-year fixed mortgage rate rose to 6.18% in March, up from 6.05% in February.

Even small increases in rates can have a noticeable impact on monthly payments, reducing affordability and limiting how much buyers can borrow.

Because home purchases typically take 30 to 60 days to close, current sales data may not fully reflect recent rate changes. This suggests that further slowdowns could appear in upcoming reports if rates remain elevated.

Regional Trends Show Mixed Results

Sales declined in all four major U.S. regions on a monthly basis, but year-over-year trends were more mixed:

- Northeast: Sales down 12.2% annually, prices up 5.7%

- Midwest: Sales down 3.2%, prices up 4.9%

- South: Sales up 2.2%, prices up 0.8%

- West: Sales up 1.3%, prices down 1.3%

The West was the only region to see a decline in median prices, suggesting some cooling in higher-cost markets. Meanwhile, the South and Midwest continue to show relative stability.

Breakdown by Property Type

Different property types are experiencing varying levels of demand:

Single-family homes:

- Sales down 3.5% month-over-month

- Median price: $412,400 (up 1.3% annually)

Condos and co-ops:

- Sales down 5.4% month-over-month

- Median price: $371,500 (up 2.3% annually)

Condos saw a larger drop in sales, which may reflect shifting buyer preferences or affordability concerns.

Buyer Activity and Market Behavior

The report also highlights changing buyer patterns:

- First-time buyers: 32% of purchases

- Cash sales: 27% of transactions

- Investors/second-home buyers: 18% of sales

- Median days on market: 41 days

The share of first-time buyers remains relatively low, showing the ongoing challenge of affordability. At the same time, investor activity is increasing, which can add competition for available homes.

Housing Affordability Shows Mixed Signals

The Housing Affordability Index declined slightly to 113.7 in March, indicating reduced affordability compared to the previous month.

However, on a yearly basis, affordability improved across all regions due to slower price growth and slightly better income conditions. This suggests that while short-term conditions remain tight, the long-term trend may be stabilizing.

Updated Housing Market Outlook for 2026

The NAR has adjusted its housing forecast for the year:

- Existing-home sales expected to rise 4% (lower than earlier projections)

- New-home sales expected to remain flat

- Home prices still projected to increase about 4%

These revisions reflect the impact of higher mortgage rates and limited inventory, both of which are expected to persist throughout the year.

Final Thoughts

The March 2026 housing data shows a market that is slowing but not declining sharply. Sales are down, but activity continues, and prices remain supported by low supply.

For buyers, the environment remains challenging, with higher rates and limited options. For sellers, the market still offers strong pricing power, though demand may be more selective.

Overall, the housing market is in a period of adjustment, balancing between affordability pressures and ongoing supply constraints. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses