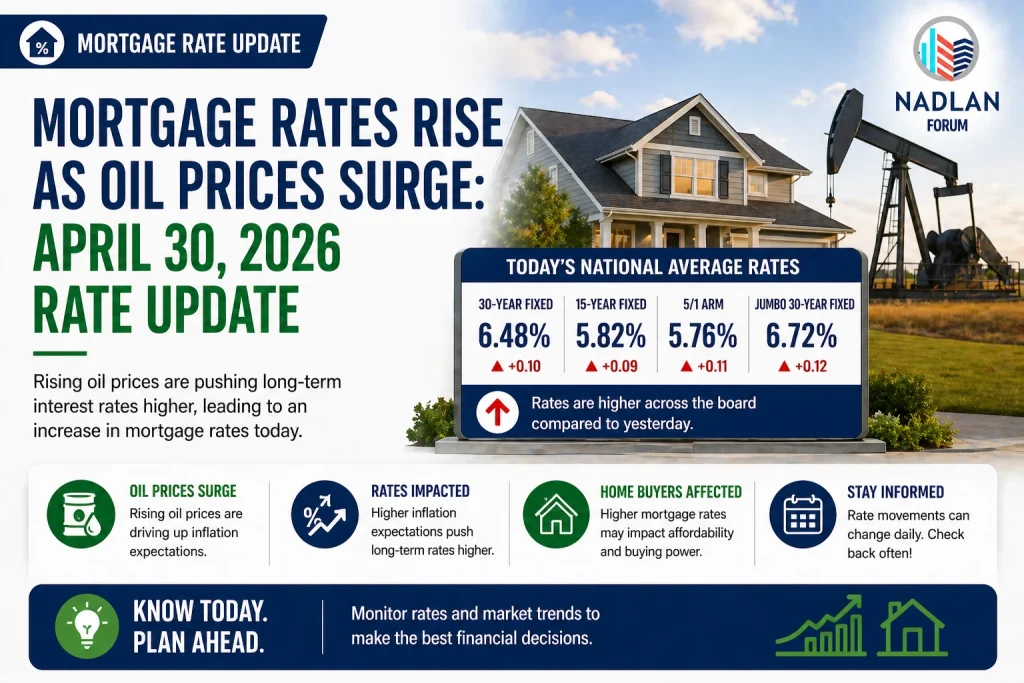

Mortgage Rates Rise as Oil Prices Surge: April 30, 2026 Rate Update

Mortgage rates moved higher this week as rising oil prices added new pressure to inflation expectations. The increase comes at a time when the housing market is entering its peak spring season, making borrowing costs a key concern for buyers.

According to data from Freddie Mac, the average 30-year fixed mortgage rate climbed to 6.3%, up from 6.23% the previous week. This marks a reversal after several weeks of declining rates.

Why Mortgage Rates Are Rising

The recent increase in mortgage rates is closely tied to broader economic developments.

Growing tensions between the U.S. and Iran have pushed oil prices higher, raising concerns about inflation. As energy costs increase, they tend to affect transportation, production, and overall consumer prices.

Mortgage rates often follow movements in the 10-year Treasury yield, which has also risen in response to inflation concerns. When investors expect higher inflation, bond yields typically move higher—and mortgage rates follow.

Market Reaction and Buyer Activity

Despite rising rates, some buyers are still moving forward with home purchases.

Recent data shows that mortgage applications for home purchases increased slightly over the past week. This suggests that buyers are taking advantage of improved housing inventory, even as borrowing costs rise.

At the same time, higher rates continue to create challenges for affordability, especially for first-time buyers.

Current Mortgage Rates (April 30, 2026)

Here are the latest national average mortgage rates based on data from Zillow:

- 30-year fixed: 6.11%

- 20-year fixed: 6.08%

- 15-year fixed: 5.62%

- 5/1 ARM: 6.11%

- 7/1 ARM: 6.09%

- 30-year VA: 5.62%

- 15-year VA: 5.34%

- 5/1 VA: 5.36%

These figures are national averages and can vary depending on location, credit score, and lender.

Current Refinance Rates

Refinance rates are also showing small movements:

- 30-year fixed refinance: 6.19%

- 20-year fixed refinance: 5.99%

- 15-year fixed refinance: 5.64%

- 5/1 ARM refinance: 5.85%

- 7/1 ARM refinance: 5.90%

- 30-year VA refinance: 5.67%

- 15-year VA refinance: 5.21%

- 5/1 VA refinance: 5.16%

Refinance rates are often close to purchase rates, though they can sometimes be slightly higher depending on market conditions.

How Mortgage Rates Work

A mortgage interest rate is the cost of borrowing money from a lender, expressed as a percentage. There are two main types of mortgage rates:

Fixed-rate mortgages:

- Rate stays the same for the entire loan term

- Monthly payments remain predictable

Adjustable-rate mortgages (ARMs):

- Rate stays fixed for an initial period

- Adjusts periodically based on market conditions

For example, a 5/1 ARM keeps the same rate for five years and then adjusts once per year after that.

What Affects Mortgage Rates

Mortgage rates are influenced by both personal and economic factors.

Factors you can control:

- Credit score

- Debt-to-income ratio

- Down payment size

- Choice of lender

Factors you cannot control:

- Inflation trends

- Economic growth

- Global events

- Federal Reserve policy

When the economy is strong or inflation is rising, rates tend to increase. When economic activity slows, rates may decline to encourage borrowing.

30-Year vs 15-Year Mortgage

Two of the most common mortgage options are 30-year and 15-year fixed loans.

30-year mortgage:

- Lower monthly payments

- Higher total interest over time

15-year mortgage:

- Lower interest rate

- Faster payoff

- Higher monthly payments

The choice depends on whether you want lower monthly costs or long-term savings on interest.

Impact on Homebuyers

Rising mortgage rates can affect buyers in several ways:

- Higher monthly payments

- Reduced purchasing power

- Increased focus on affordability

However, some buyers are still active in the market due to better inventory and the need to secure housing before rates move even higher.

FAQs About Mortgage Rates

What is the current 30-year mortgage rate?

The national average is around 6.1% to 6.3%, depending on the data source.

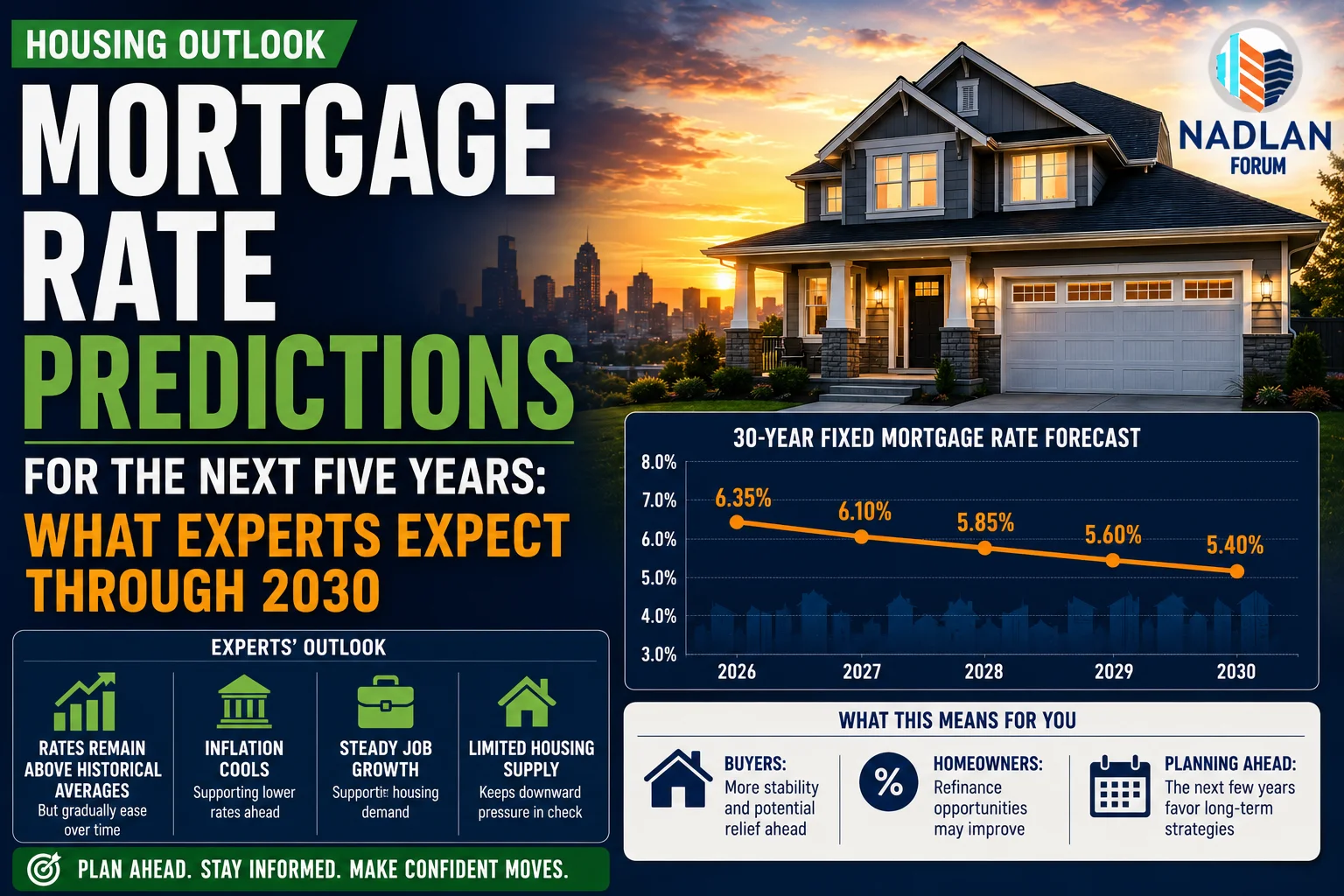

Are mortgage rates expected to fall?

Rates may remain volatile due to inflation and global factors, including energy prices.

What is considered a low mortgage rate?

Rates below 3% were seen during 2020–2021, but such levels are unlikely in the current market.

When should you refinance?

Many experts suggest refinancing when you can lower your rate by 1% to 2%, depending on your financial goals.

Final Outlook

Mortgage rates are rising again as inflation concerns return, largely driven by higher oil prices and global uncertainty. While the increases are modest, they highlight how sensitive borrowing costs are to economic changes.

For buyers and homeowners, the current environment requires careful planning. Comparing lenders, improving credit profiles, and understanding loan options can help manage costs in a market where rates are likely to remain unpredictable in the near term. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses