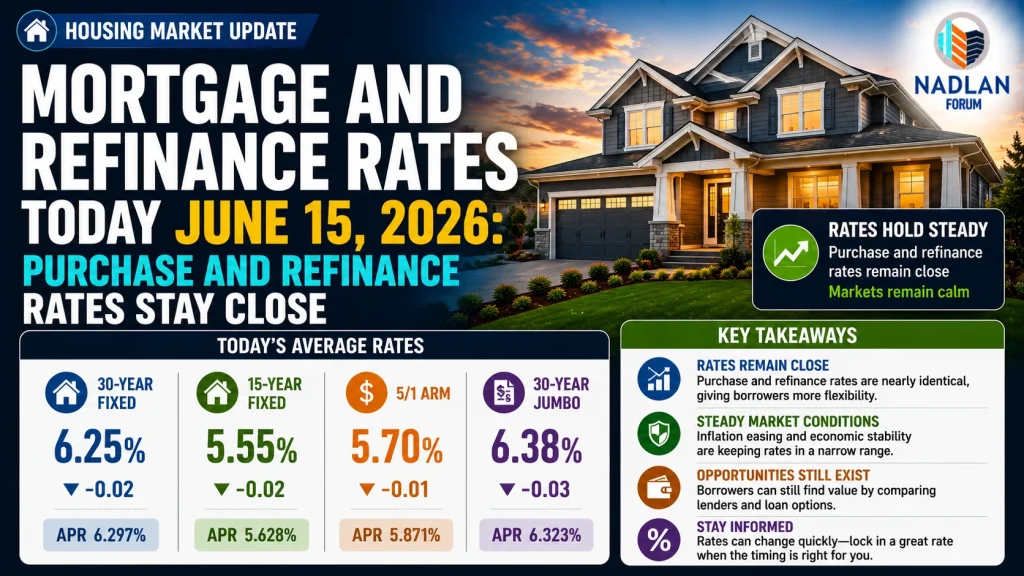

Mortgage Rates Today April 20, 2026: Rates Near 6% and May Drop Lower

Mortgage Rates Hold Steady With Downward Pressure

Mortgage rates are staying relatively low and could soon move below the 6% level, giving some relief to buyers and homeowners. According to data from Zillow, the average 30-year fixed mortgage rate is currently 6.02%, while the 15-year fixed rate stands at 5.50%.

After weeks of volatility earlier this year, the market is now showing signs of stability. Lower bond yields and easing global concerns are helping keep rates from rising again, and that has improved sentiment among buyers heading into the spring season.

Today’s Mortgage Rates Snapshot

Here are the latest national average rates:

- 30-year fixed: 6.02%

- 20-year fixed: 5.84%

- 15-year fixed: 5.50%

- 5/1 ARM: 6.17%

- 7/1 ARM: 5.98%

- 30-year VA: 5.57%

- 15-year VA: 5.34%

- 5/1 VA: 5.39%

These numbers are averages, so actual rates can vary based on credit score, location, and lender terms.

Current Refinance Rates

Refinance rates remain slightly higher than purchase rates in most cases:

- 30-year fixed refinance: 6.12%

- 20-year fixed refinance: 6.24%

- 15-year fixed refinance: 5.57%

- 5/1 ARM refinance: 6.09%

- 7/1 ARM refinance: 6.35%

- 30-year VA refinance: 5.48%

- 15-year VA refinance: 5.21%

- 5/1 VA refinance: 5.33%

For homeowners who locked in higher rates in recent months, the current trend may create opportunities to refinance especially if rates drop further.

30-Year vs. 15-Year Mortgage: Cost Difference

Choosing between a 30-year and 15-year loan still depends on your financial priorities.

30-Year Fixed Mortgage

- Lower monthly payments

- More flexibility in budgeting

- Higher total interest over time

Example:

A $300,000 loan at 6.02% results in:

- Monthly payment: about $1,803

- Total interest: about $348,904

15-Year Fixed Mortgage

- Higher monthly payments

- Lower interest rate

- Major long-term savings

Example:

The same $300,000 loan at 5.50% results in:

- Monthly payment: about $2,451

- Total interest: about $141,225

This shows how shorter terms can save over $200,000 in interest, but require stronger monthly cash flow.

Adjustable-Rate Mortgages: Are They Worth It?

Adjustable-rate mortgages (ARMs) still play a role, but they are less attractive right now.

- Rates are sometimes similar to fixed-rate loans

- Payments can increase after the initial fixed period

- Best suited for short-term homeowners

For example, a 5/1 ARM keeps the same rate for five years, then adjusts annually. If you plan to move before that adjustment period, an ARM could reduce upfront costs.

However, in today’s market, fixed rates are often competitive enough that many buyers prefer the stability.

Why Mortgage Rates Are Staying Low

Mortgage rates are influenced by several economic factors, including:

- Inflation trends

- Federal Reserve policy expectations

- Bond market movements

- Global economic conditions

Recent easing in energy prices and improved market confidence have helped stabilize rates. While uncertainty still exists, especially globally, the overall direction has shifted toward gradual improvement.

How to Get a Lower Mortgage Rate

Even in a favorable rate environment, your personal profile matters. To secure the best rate:

- Improve your credit score

- Lower your debt-to-income ratio (DTI)

- Save for a larger down payment

- Compare multiple lenders

You can also consider discount points, where you pay upfront to reduce your interest rate, or temporary rate buydowns to lower payments in the early years.

What This Means for Buyers and Homeowners

For buyers, today’s rates offer a better opportunity than last year, even if affordability challenges remain. Lower rates improve buying power and reduce long-term costs.

For homeowners, refinancing could become more attractive if rates dip below 6%. Even a small drop can make a noticeable difference in monthly payments and total interest.

Outlook for the Rest of 2026

Forecasts suggest mortgage rates may stay close to current levels:

- Around 6.3% on average through 2026

- Potential to fall slightly below 6% later in the year

- Moderate stability expected into 2027

While a return to ultra-low rates is unlikely, the current environment is far more balanced than the peaks seen in recent years.

Bottom Line

Mortgage rates in April 2026 are holding near 6% and could move lower in the coming months. This creates a window of opportunity for both buyers and homeowners.

The key is not just timing the market but making sure your finances are ready. A strong credit profile, smart loan choice, and careful planning can make a bigger difference than small rate changes alone. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses