U.S. Housing Market Trends: Rising Mortgage Payments and High Rates in 2026

Mortgage Payments Hit Record Highs in Q4 2025

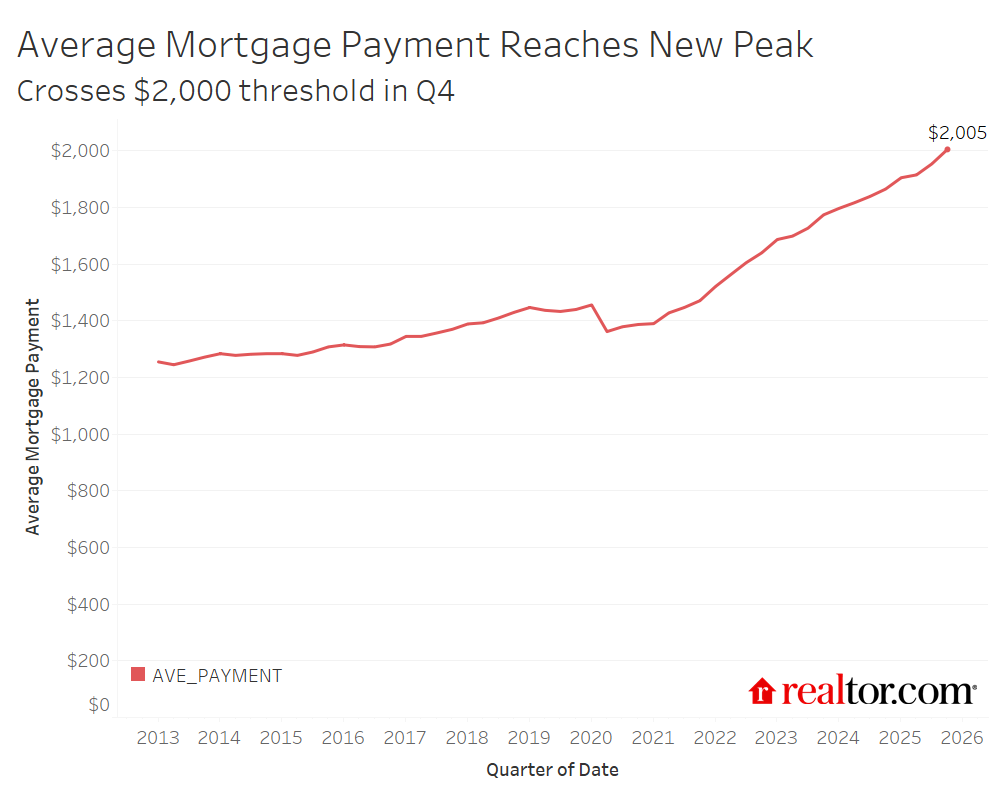

According to the latest data from Realtor.com, the average mortgage payment for U.S. homeowners surpassed $2,000 for the first time in Q4 2025. This reflects a significant shift as homebuyers struggle to manage higher interest rates and rising property prices. The impact of rising rates is still being felt by many, particularly those who bought homes during the pandemic when rates were at historic lows.

Homebuyers entering the market in 2026 are faced with average mortgage rates between 5% and 7%, and for many, this means higher monthly payments. This shift is causing considerable stress for many potential buyers who are already grappling with affordability challenges.

Mortgage Rates and Loan Trends: How Rising Rates Affect Homeowners

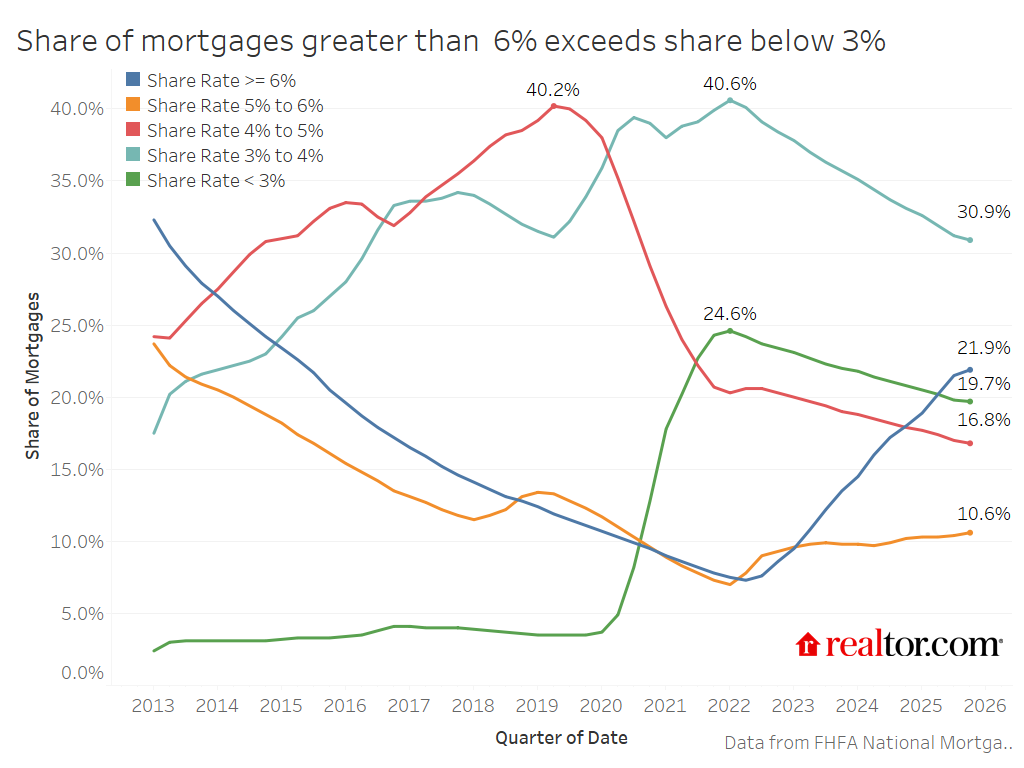

The decline in mortgage rates from 6.34% in early October 2025 to 6.15% by the end of the year gave homeowners a brief reprieve, but the rising geopolitical concerns from the Middle East conflict have pushed rates back up in March 2026. Despite these fluctuations, rates have remained above 6% since September 2022.

This ongoing uncertainty continues to impact homebuyer behavior, especially when it comes to moving or selling homes. Potential sellers are finding themselves “locked in” with lower rates from previous mortgages, which is preventing them from listing their properties and contributing to low inventory. As a result, the market remains highly competitive with limited options for buyers.

Shifting Mortgage Rate Distribution

According to the latest data, a significant portion of mortgages still falls below the 6% mark. In fact, 78% of outstanding mortgages have rates below 6%, with just 21.9% of mortgages carrying rates of 6% or higher. This is a notable change from previous years, as a growing number of homeowners with historically low interest rates find themselves staying in their homes longer to preserve their favorable mortgage terms.

However, the market is still feeling the effects of the surge in mortgage rates after 2022. As mortgage payments continue to rise, fewer homeowners are refinancing, and the average payment is significantly higher than it was just a few years ago.

The Impact of Rising Payments on Affordability

The average payment of $2,005 in Q4 2025 represents a sharp increase over previous years. From an average payment of $1,255 in early 2013, the cost of homeownership has escalated as housing prices continue to climb. By the beginning of 2020, the average mortgage payment had risen to $1,456, and it has steadily climbed ever since.

The most significant increase came after mid-2022, when mortgage rates surged. In just three years, the average mortgage payment has gone up by more than $600, a 44% increase. This change reflects not only the rise in rates but also the significant increase in home prices, which have continued to outpace wages.

Trends in Homeowner and Buyer Activity

Despite the ongoing affordability challenges, homebuyers are still active in the market. Many are dealing with these financial pressures by adjusting their expectations and seeking out properties that better fit their current budgets.

- 43% of homebuyers indicated that they anticipated closing a transaction within two weeks, showing that speed is becoming a key factor in today’s housing market.

- Younger buyers, including Gen Z and millennials, are more likely to expect quick closings compared to older generations.

Regional Variations in Mortgage Trends

There are regional differences in how mortgage trends are affecting homeowners. In areas with high housing demand and limited inventory, such as coastal cities, the competition for homes remains fierce, pushing prices even higher.

However, in other parts of the country where housing is more affordable, buyers may have more opportunities to secure properties with lower rates and less competition. These areas are seeing a slight uptick in listings and increased activity, which is bringing some optimism to the housing market despite the overall challenges.

Looking Ahead: What’s Next for the Housing Market?

As we move further into 2026, the outlook for homebuyers remains uncertain. While the housing market has shown some signs of improvement, such as increased listings and pending sales, the combination of high mortgage rates and soaring property prices continues to put pressure on buyers.

The market’s trajectory will likely depend on how quickly interest rates stabilize and whether sellers feel comfortable entering the market with higher rates. Buyers will continue to be cautious, looking for ways to manage rising costs, but will also have to weigh the benefits of homeownership against the current economic landscape.

In conclusion, the U.S. housing market is experiencing significant shifts in mortgage payments and rates, creating new challenges for both buyers and homeowners. While mortgage rates remain a central concern, the demand for homes persists, and buyers are adapting by seeking more affordable options and adjusting their expectations. Whether the market will see a full recovery or continue to struggle remains to be seen, but the impact of rising mortgage payments on affordability is undeniable. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses