Mortgage Rates Reach 9-Month High: Inflation and Iran War Push Borrowing Costs Higher

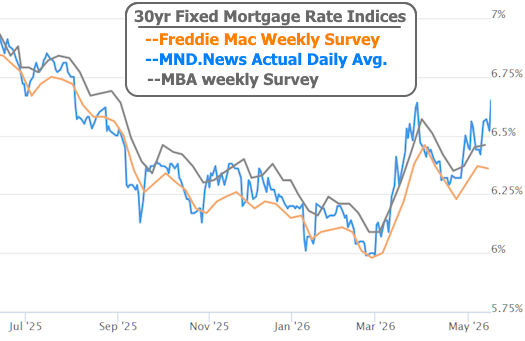

Mortgage rates moved sharply higher this week, reaching their highest levels in roughly nine months as inflation concerns and global tensions continued putting pressure on the bond market.

The average 30-year fixed mortgage rate climbed significantly during the week, reversing much of the improvement borrowers had seen earlier this year. Housing analysts say growing inflation worries tied to rising energy prices and ongoing geopolitical uncertainty remain the biggest drivers behind the increase.

Over the past nine months, mortgage rates have experienced major swings. Rates previously dropped by roughly 0.65 percentage points before climbing back to nearly the same levels again by the end of this week.

This week alone accounted for a noticeable jump in borrowing costs as financial markets lost confidence that the Iran conflict would end quickly.

Why Mortgage Rates Are Rising Again

Mortgage rates are heavily influenced by the bond market, particularly U.S. Treasury yields and mortgage-backed securities.

When investors expect inflation to rise, bond yields usually move higher. Since mortgage rates follow bond market trends closely, borrowing costs for homebuyers often increase as well.

Several major factors are currently pushing rates upward:

- Rising oil prices

- Inflation concerns

- Government borrowing needs

- Ongoing geopolitical uncertainty

- Stronger inflation data

Analysts say the Iran conflict has become one of the largest drivers of recent mortgage market volatility.

Higher oil prices caused by the conflict are increasing transportation, manufacturing, and energy costs throughout the economy. Investors worry these higher costs could keep inflation elevated for a longer period.

Inflation Reports Added More Pressure

Fresh inflation data released this week reinforced market concerns that inflation remains far from under control.

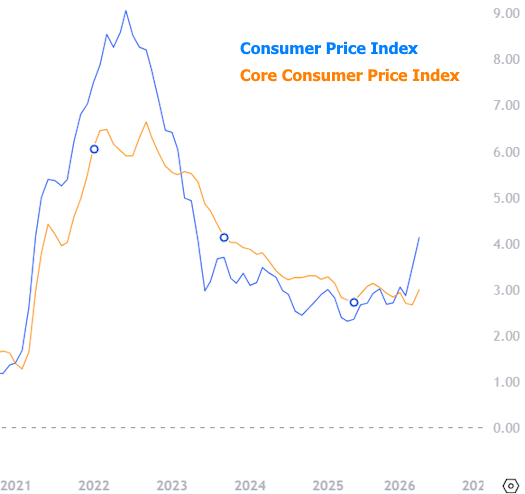

The Consumer Price Index (CPI) rose to its highest annual level since 2023, signaling that household costs continue increasing across many sectors of the economy.

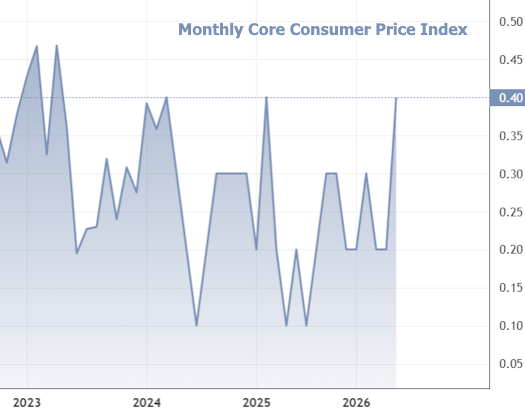

Even core inflation, which excludes food and energy prices, showed continued strength.

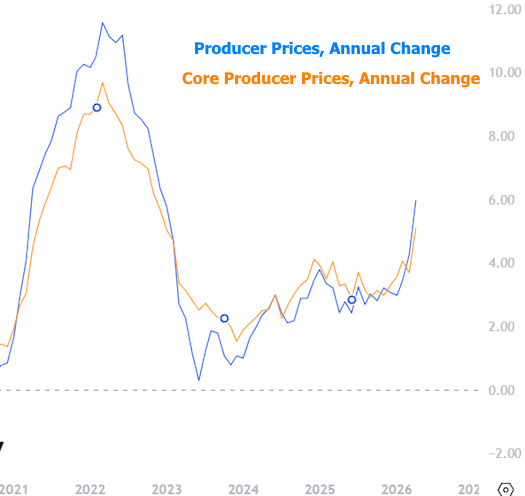

At the wholesale level, inflation pressures were even stronger.

The Producer Price Index (PPI) surged 6% year over year, marking the highest reading since late 2022. Core wholesale inflation also climbed to its highest level in years.

Economists say these reports confirmed what financial markets were already expecting after energy prices surged earlier this spring.

Oil Prices Continue Impacting the Housing Market

Energy prices remain one of the biggest concerns for both consumers and financial markets.

Since the conflict in the Middle East intensified earlier this year, oil prices have climbed sharply. Gasoline prices in many parts of the country have moved back above $4 per gallon, adding pressure to household budgets.

Higher energy costs can affect the housing market in several ways:

- Higher mortgage rates

- Reduced buyer affordability

- Increased construction costs

- Higher transportation expenses

- Rising household monthly costs

Housing analysts say these factors are beginning to create additional pressure on homebuyers already dealing with elevated home prices.

Bond Market Reacts to Geopolitical Tensions

Financial markets also reacted negatively after this week’s Trump-Xi summit ended without any major breakthrough involving the Iran conflict.

Some investors had hoped the meeting could lead to diplomatic progress or at least signals that tensions might ease.

Instead, bond yields moved sharply higher immediately after the summit concluded without new developments.

By Friday afternoon, the 10-year Treasury yield had climbed to its highest level in roughly a year.

Mortgage rates followed closely behind.

Mortgage Rates Still Slightly Protected

Even though Treasury yields moved significantly higher, mortgage rates did not rise quite as quickly.

Analysts say this is partly because Fannie Mae and Freddie Mac have continued purchasing mortgage-backed securities in large amounts.

These purchases help support the mortgage market by reducing the spread between Treasury yields and mortgage rates.

In simple terms, government-backed buying activity has helped prevent mortgage rates from rising even faster.

Still, rates remain well above levels many buyers hoped to see earlier this year.

Homebuyers Face Renewed Affordability Challenges

The latest rate increase creates new affordability concerns for buyers entering the spring and summer housing market.

Even relatively small changes in mortgage rates can significantly affect monthly payments.

For example:

- A higher rate increases monthly mortgage costs

- Buyers may qualify for smaller loan amounts

- Purchasing power declines

- Competition for lower-priced homes may increase

Many buyers who were waiting for rates to fall further may now face additional pressure if borrowing costs remain elevated.

Federal Reserve Outlook Becoming More Complicated

The inflation data also makes it more difficult for the Federal Reserve to justify cutting interest rates in the near future.

Markets previously expected multiple rate cuts in 2026. However, expectations have shifted dramatically over the past several weeks.

Some traders are now even pricing in the possibility of future rate hikes if inflation continues accelerating.

Federal Reserve officials have repeatedly stated they remain focused on controlling inflation before considering additional easing.

With inflation readings still running well above the Fed’s 2% target, analysts say policymakers are likely to remain cautious.

Housing Market Activity May Slow Again

Higher mortgage rates could create additional challenges for the housing market moving into the second half of 2026.

Recent weeks had shown signs of improving buyer activity as rates briefly moved lower during April.

Pending home sales, mortgage applications, and buyer interest had all started improving modestly.

However, the recent spike in rates could slow some of that momentum.

Potential impacts include:

- Fewer mortgage applications

- Slower home sales

- Reduced refinancing activity

- More cautious buyers

- Increased affordability pressure

Housing economists say the market remains highly sensitive to interest rate changes after several years of elevated borrowing costs.

Inflation and War Remain the Main Drivers

For now, mortgage markets remain heavily tied to inflation trends and developments involving the Iran conflict.

If energy prices continue rising, inflation could remain elevated through much of the year. That would likely keep pressure on both Treasury yields and mortgage rates.

On the other hand, any meaningful progress toward a peace agreement could help stabilize oil prices and potentially improve mortgage market conditions.

Analysts say rates could move lower again if inflation cools and geopolitical risks ease. But this week showed how quickly markets can reverse when optimism fades.

Outlook for Mortgage Rates

Most economists expect mortgage rates to remain volatile in the near term.

Current forecasts suggest rates may continue hovering above 6% throughout much of 2026 unless inflation improves significantly.

Several factors will likely determine where rates move next:

- Inflation reports

- Oil prices

- Federal Reserve policy

- Labor market strength

- Global geopolitical developments

For homebuyers, affordability remains the biggest challenge.

While housing inventory has improved in many markets, higher borrowing costs continue limiting purchasing power for many Americans.

The mortgage market now enters the second half of 2026 facing renewed uncertainty as inflation pressures and global risks continue shaping the outlook for rates. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses