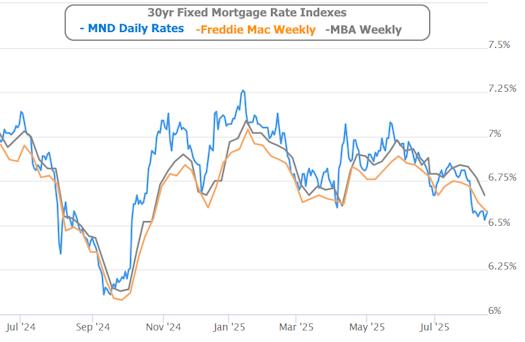

Mortgage Rates Touch 10-Month Lows — But a Fed Cut Isn’t a Guaranteed Fix

Mortgage rates recently reached their lowest levels in nearly 10 months, driven largely by expectations of an upcoming Federal Reserve rate cut. Yet, even with the Fed likely to act soon, homeowners and prospective buyers shouldn’t automatically assume rates will drop further. The reality is a bit more nuanced.

Inflation Data Steers the Market

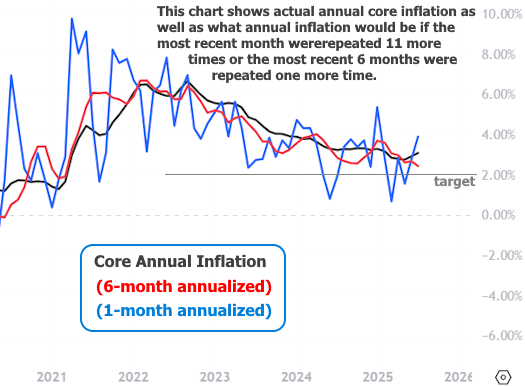

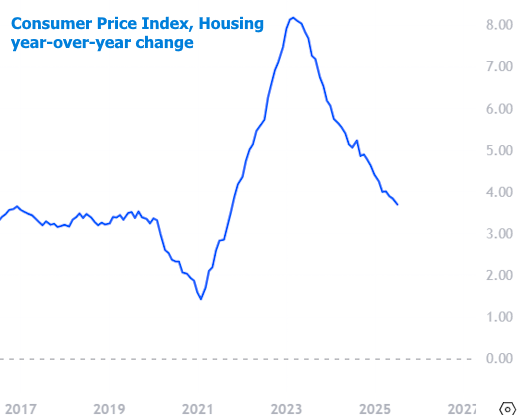

The week’s economic reports were closely watched by both markets and mortgage lenders. Tuesday’s Consumer Price Index (CPI) report largely aligned with forecasts. While certain categories, particularly those affected by tariffs, showed price increases, housing costs continued to ease, preventing an overall spike. Initially, this was welcome news for the mortgage market. Investors interpreted the data as supportive of Fed easing, pushing mortgage rates lower and raising expectations of a September cut to nearly 100% by midweek.

Wednesday offered a momentary calm, with no major reports to sway markets. Mortgage rates largely held their ground, buoyed by optimism surrounding the Fed’s potential actions.

However, Thursday brought a jolt. The Producer Price Index (PPI), which measures wholesale inflation, came in significantly higher than expected. This suggested that tariff pressures could continue to push prices upward in the months ahead. While the data wasn’t universally alarming—some components that overlap with the Personal Consumption Expenditures (PCE) index, the Fed’s preferred inflation gauge, remained moderate the report was enough to lift bond yields and, consequently, mortgage rates.

Friday saw stronger-than-expected retail sales. While bond markets initially remained stable, trading conditions deteriorated as the day progressed, prompting several lenders to make minor afternoon rate increases. Despite this, the average mortgage rate remained significantly lower than most of the past 10 months, demonstrating just how far rates had fallen in the first place.

The Fed’s Role: Expectation vs. Reality

Mortgage rates often move alongside expectations of Fed policy changes, rather than the actual changes themselves. This is because both mortgage rates and Fed policy are influenced by similar economic factors particularly inflation, employment data, and broader market sentiment.

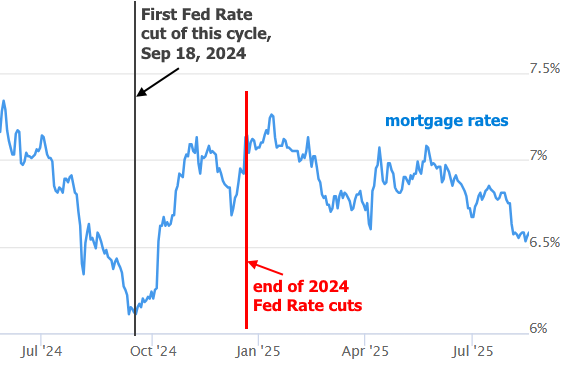

History offers a clear example. In late 2024, mortgage rates hit long-term lows as investors anticipated Fed action. Yet, when the Fed finally cut rates, mortgage rates began rising again, illustrating that a cut alone does not automatically lower borrowing costs.

The takeaway for today’s market is that while a potential Fed rate cut may offer some support for mortgage rates, it is not a guarantee of further declines. Future movements will depend heavily on incoming economic data, particularly employment reports and the next round of inflation measures.

Looking Ahead: Key Economic Events

The coming week is packed with critical updates that could influence mortgage rates further:

- Wednesday: The Fed will release the minutes from its most recent meeting. While this offers a detailed look at the Fed’s discussions, it reflects conditions from three weeks ago and cannot account for recent economic developments.

- Thursday: The Fed’s annual Jackson Hole Symposium kicks off. This is a more forward-looking event where the Fed Chair and other officials can discuss expectations, concerns, and potential policy directions, taking recent inflation and labor data into account.

Investors and homebuyers should pay close attention to these events, as the statements and guidance emerging from Jackson Hole often have immediate and tangible effects on bond markets—and, by extension, mortgage rates.

Bottom Line: Rates Are Near Lows, But Caution Is Key

Mortgage rates remain tantalizingly close to their lowest levels of the year. However, several factors could influence whether they continue downward or begin creeping back toward the levels seen earlier in 2025:

- Inflation Trends: Rising inflation could push rates higher despite Fed intervention.

- Employment Data: Strong job growth could signal a robust economy, potentially tempering expectations for rate cuts.

- Tariff Impacts: Prices influenced by international trade policies could create inflationary pressures that keep rates elevated.

For homebuyers and refinancers, the current environment presents both opportunity and uncertainty. While rates are historically low, locking in a mortgage now may be wise for those who prefer certainty over speculation. On the other hand, future economic data could either open the door to slightly lower rates or push them higher.

In short, while the Fed is likely to cut rates in September, mortgage rates don’t respond in a straight line. Understanding the nuances of market expectations, inflation trends, and broader economic conditions is crucial for anyone looking to make a move in today’s housing market. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses