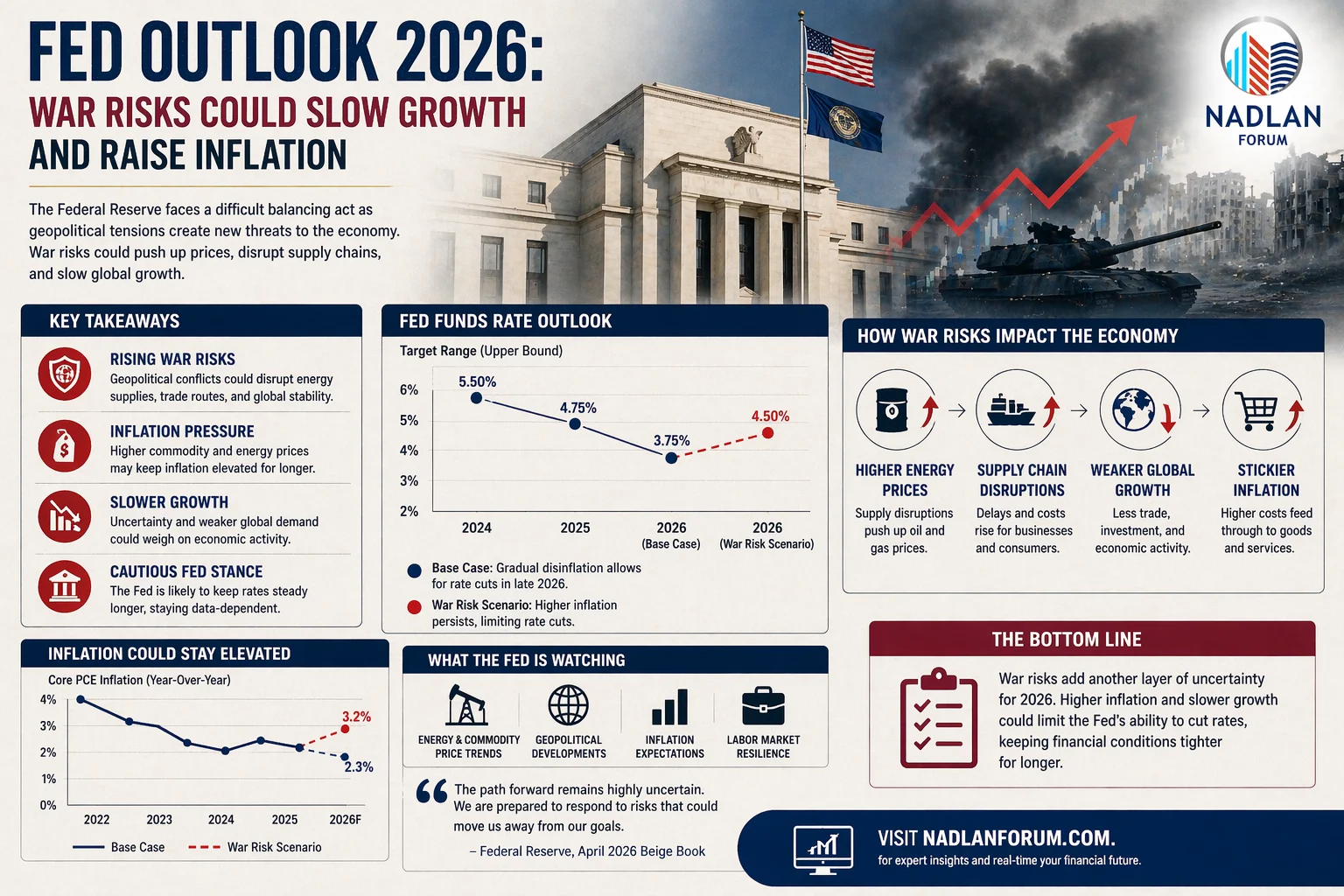

Rising Mortgage Rates Push More Homebuyers Toward Adjustable Loans

Mortgage rates continued moving higher in May, putting additional pressure on homebuyers and causing more borrowers to consider adjustable-rate mortgages as affordability challenges grow across the housing market.

According to the latest Mortgage Bankers Association data, overall mortgage application activity declined last week as borrowing costs reached their highest level in nearly two months.

At the same time, demand for adjustable-rate mortgages, commonly known as ARMs, climbed to the highest level since late 2025 as buyers searched for lower monthly payments.

Mortgage Rates Continue Moving Higher

The average contract interest rate for a 30-year fixed mortgage with conforming loan balances increased to 6.56% last week, up from 6.46% the previous week.

This marks the highest average level in seven weeks and continues the broader upward trend seen throughout May.

Mortgage rates have been climbing as financial markets react to:

- Higher inflation readings

- Rising fuel and energy costs

- Global debt concerns

- Treasury yield increases

- Ongoing geopolitical tensions

Higher Treasury yields typically push mortgage rates higher because mortgage-backed securities compete directly with government bonds for investor demand.

Adjustable-Rate Mortgage Demand Surges

As fixed mortgage rates become more expensive, borrowers are increasingly turning to adjustable-rate mortgages to reduce upfront monthly costs.

The ARM share of total mortgage applications rose to nearly 10%, the highest level since October 2025.

The average interest rate on a five-year adjustable mortgage was 5.76%, significantly lower than the average 30-year fixed rate.

For many buyers struggling with affordability, even a small difference in rates can meaningfully reduce monthly payments.

That is becoming especially important as housing costs continue rising across many markets.

Why Buyers Are Choosing ARMs Again

Adjustable-rate mortgages became far less popular after the 2008 housing crisis, but they are beginning to return as affordability pressure intensifies.

With an ARM, borrowers receive a lower fixed interest rate for an introductory period, typically five, seven, or ten years.

After that period ends, the rate adjusts periodically based on market conditions.

Many buyers are now considering ARMs because:

- Fixed mortgage rates remain elevated

- Monthly payments are becoming harder to afford

- Home prices are still high in many areas

- Buyers expect rates could eventually decline

- Some borrowers plan to refinance later

Borrowers who do not expect to stay in a property long term may also see ARMs as a temporary solution.

Risks of Adjustable-Rate Mortgages

Although ARMs offer lower starting rates, they also carry more risk than fixed-rate loans.

Once the introductory period expires, monthly payments can increase significantly if market interest rates remain elevated.

That uncertainty is why adjustable loans are generally considered riskier products.

During the housing crash years, many borrowers faced payment shocks when adjustable rates reset higher.

However, lending standards today are significantly stricter than they were before the 2008 financial crisis.

Most lenders now require stronger income documentation and clearer borrower qualification standards.

Home Purchase Activity Slows

Higher borrowing costs are also reducing demand from homebuyers.

Applications for mortgages to purchase homes fell 4% compared to the previous week.

Purchase activity remains only modestly above year-ago levels, even though mortgage rates were closer to 7% at this time last year.

The spring housing market has remained weaker than many analysts originally expected entering 2026.

While inventory levels have improved in some markets, affordability continues limiting buyer activity.

Many households remain cautious because of:

- Elevated mortgage payments

- Rising insurance costs

- Higher property taxes

- Economic uncertainty

- Inflation concerns

- Energy price increases

Refinance Activity Also Weakens

Refinance demand remained soft as well.

Applications to refinance existing mortgages declined slightly from the prior week, though refinance activity still remains above year-ago levels because many homeowners continue searching for ways to reduce monthly expenses.

However, refinancing opportunities remain limited for borrowers who locked in ultra-low mortgage rates during 2020 and 2021.

Many homeowners still hold mortgage rates below 4%, making refinancing unattractive in the current environment.

Inflation Remains a Major Problem for Rates

One of the biggest drivers behind rising mortgage rates continues to be inflation.

Recent economic reports showed inflation moving higher again in April, fueled partly by rising energy prices connected to global supply disruptions and geopolitical tensions.

Investors closely monitor inflation because persistent price increases reduce the purchasing power of future bond payments.

As inflation expectations rise, bond investors demand higher yields, which directly impacts mortgage rates.

The market has also reduced expectations for Federal Reserve rate cuts later this year.

Some traders are now even pricing in the possibility of future rate hikes if inflation remains elevated.

Affordability Challenges Continue Growing

Housing affordability remains one of the biggest obstacles for buyers in 2026.

Higher mortgage rates dramatically increase monthly housing costs even when home prices remain stable.

For example, a buyer financing a $400,000 home today faces hundreds of dollars more in monthly payments compared to borrowers who purchased homes during the low-rate environment just a few years ago.

That affordability gap is forcing many buyers to:

- Delay purchases

- Reduce home budgets

- Move to lower-cost areas

- Consider smaller homes

- Explore adjustable-rate loans

Some first-time buyers are also increasingly relying on temporary rate buydowns and seller concessions.

Mortgage Market Faces Uncertain Summer Outlook

Mortgage analysts expect rate volatility to continue through the summer as markets monitor inflation data, Federal Reserve policy signals, and global economic developments.

If inflation remains elevated, mortgage rates could stay above 6.5% or potentially move even higher.

However, some analysts believe rates could stabilize later in the year if inflation pressures ease and energy prices decline.

For now, buyers continue facing a difficult balance between elevated borrowing costs and limited affordability improvements.

Housing Market Activity May Slow Further

The recent increase in rates may create additional pressure on housing demand heading into the second half of 2026.

Many economists expected lower mortgage rates to help revive housing activity this year, but recent inflation data has complicated that outlook.

While some markets continue seeing stable demand, many buyers remain sensitive to even small changes in borrowing costs.

As a result, mortgage rates are likely to remain one of the biggest factors influencing housing market activity over the coming months. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses