How the Iran Peace Deal Is Shaping Mortgage Rates in June 2026

Mortgage rates remained under pressure this week as investors balanced two major market developments: progress toward a peace agreement involving Iran and a more cautious outlook from the Federal Reserve.

For much of the spring, geopolitical events in the Middle East played a major role in bond market movements. However, that focus shifted after the Federal Reserve’s latest policy meeting, which introduced new expectations for interest rates and quickly became the dominant force driving market sentiment.

Although financial markets experienced volatility following the Fed announcement, mortgage rates ultimately remained relatively stable compared with recent months.

Markets Started the Week on Positive Ground

At the beginning of the week, bond markets benefited from continued signs that tensions surrounding the Iran conflict were easing.

As reports emerged that senior officials had formally signed a peace memorandum, investors responded positively. Treasury yields moved lower and reached some of their best levels in roughly a month.

Lower Treasury yields generally create favorable conditions for mortgage rates because mortgage-backed securities often move in the same direction as government bonds.

The possibility of reduced geopolitical risk helped improve investor confidence and eased some of the pressure that had been weighing on fixed-income markets earlier in the year.

Federal Reserve Meeting Changed the Conversation

The market’s attention quickly shifted on Wednesday when the Federal Reserve released its latest policy statement and economic projections.

This meeting attracted extra attention because it was the first major policy gathering under Federal Reserve Chair Kevin Warsh.

While investors closely monitored the chair’s comments, the biggest market reaction came from the Federal Reserve’s updated economic projections and interest-rate expectations.

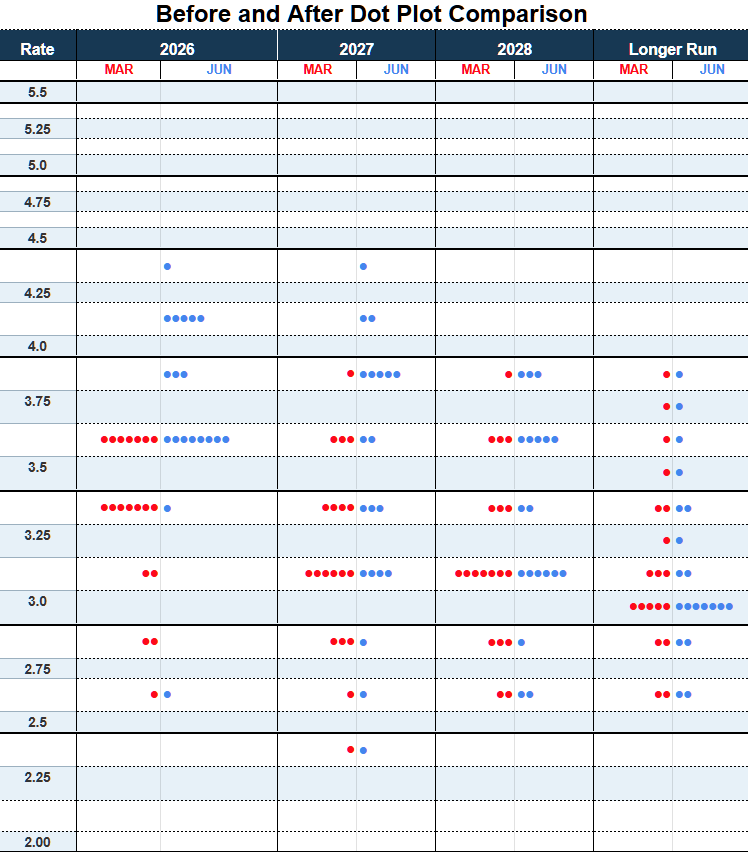

Understanding the Dot Plot

One of the most closely watched elements of every quarterly Federal Reserve projection release is the so-called “dot plot.”

The dot plot summarizes where individual Federal Reserve officials expect the federal funds rate to be in future years.

Each dot represents a policymaker’s outlook.

Investors study these projections because they provide insight into how the central bank may respond to future economic developments, including inflation, employment growth, and broader financial conditions.

Although the dot plot is not a guarantee of future action, it often influences market expectations.

Why Investors Reacted

The updated projections suggested a more cautious approach toward interest rate cuts than many investors had anticipated.

Earlier expectations had left room for stable policy or potential easing later in the year. Instead, the revised projections indicated that a significant number of policymakers now see the possibility of additional rate increases before the end of 2026.

The shift signaled that inflation concerns remain an important consideration for the central bank.

As a result, Treasury yields moved higher immediately after the release, reflecting changing expectations about future monetary policy.

Chair Warsh Avoided Strong Forward Guidance

Market participants also paid close attention to Chair Warsh’s first major press conference.

Rather than providing detailed guidance about future rate decisions, he largely avoided making commitments about the direction of policy.

His comments emphasized uncertainty and the importance of incoming economic data.

While some investors expected stronger signals regarding future rate cuts or hikes, the chair chose a more measured approach.

This left markets with fewer clues about how policymakers might respond over the coming months.

As a result, uncertainty increased, contributing to additional volatility across financial markets.

Short-Term Rates Moved Higher

One of the most notable outcomes of the Federal Reserve meeting was the increase in short-term interest rate expectations.

Financial markets adjusted their forecasts to reflect a higher likelihood that rates could remain elevated for longer than previously expected.

Investors who earlier anticipated multiple rate cuts this year have increasingly shifted toward expectations of a more restrictive policy environment.

This change was most visible in short-term Treasury securities and federal funds futures markets.

Mortgage Rates Held Up Better Than Expected

Despite the volatility, mortgage rates did not experience the same degree of movement seen in some short-term interest rate markets.

Mortgage pricing tends to follow longer-term Treasury yields rather than overnight interest rates.

Because longer-term bond markets recovered much of their post-Fed losses by the end of the week, mortgage rates avoided a significant spike.

This helped limit the impact on prospective homebuyers and homeowners considering refinancing.

Although mortgage rates remain elevated compared with historical averages, the week’s events did not dramatically alter the overall lending environment.

Why Mortgage Rates Behave Differently

Many consumers assume mortgage rates move directly with Federal Reserve policy decisions.

In reality, mortgage rates are influenced by several factors, including:

- Long-term Treasury yields.

- Inflation expectations.

- Economic growth forecasts.

- Mortgage-backed security demand.

- Global investor sentiment.

- Housing market conditions.

Because mortgage loans often remain outstanding for many years, lenders focus more heavily on long-term economic expectations rather than short-term policy changes.

This explains why mortgage rates can sometimes fall even when the Federal Reserve keeps rates unchanged—or rise despite expectations for future rate cuts.

What Homebuyers Should Watch

For buyers and homeowners, several developments remain important.

Inflation Data

Inflation remains one of the most important indicators influencing future Federal Reserve decisions.

Lower inflation could improve the outlook for mortgage rates later in the year.

Energy Prices

Oil prices have been closely linked to recent geopolitical developments.

A stable energy market could help reduce inflation pressure and support lower long-term interest rates.

Labor Market Reports

Employment data continues to influence expectations for economic growth and future monetary policy.

Strong job growth can support higher rates, while weaker labor market conditions may encourage a more accommodative policy stance.

Treasury Market Trends

Mortgage rates often follow movements in the 10-year Treasury yield.

Investors will continue monitoring bond market performance for clues about future borrowing costs.

What Happens Next?

Markets are expected to remain focused on two key themes during the coming weeks.

The first is confirmation and implementation of the Iran peace agreement. Additional stability in the region could continue supporting bond markets and easing inflation concerns tied to energy prices.

The second is incoming economic data, particularly inflation reports. Investors are looking for evidence that price pressures are continuing to moderate.

If inflation slows and economic growth remains stable, long-term interest rates could gradually improve.

However, if inflation proves more persistent than expected, borrowing costs may remain elevated.

Bottom Line

This week’s mortgage market story was shaped by two competing forces. Progress toward peace involving Iran helped support bond markets and improve investor sentiment, while the Federal Reserve’s latest projections reinforced expectations that interest rates could stay higher for longer.

Although short-term rate expectations moved noticeably higher after the Fed meeting, mortgage rates remained relatively stable because long-term Treasury yields recovered much of their initial losses.

For homebuyers, homeowners, and real estate investors, future inflation data, energy prices, and Federal Reserve policy expectations will likely remain the key drivers of mortgage rates throughout the remainder of 2026. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses