Rent vs Buy in 2026: Why the Best Choice Depends on Your Financial Goals

For generations, Americans have been told that buying a home is one of the best financial decisions they can make. The common advice has been simple: buy as soon as possible, put down as much money as you can, and build equity over time.

That strategy worked well for many families who purchased homes during the 1980s and 1990s and watched property values rise significantly over the following decades. However, today’s housing market looks very different.

High home prices, elevated mortgage rates, and rising ownership costs are forcing many consumers to rethink whether buying is always the right move. Recent housing research suggests that renting may actually be the better financial option for some households, especially depending on where they live and how long they plan to stay.

The rent-versus-buy debate is no longer a simple question with a single answer.

The Housing Market Has Changed

Buying a home has become much more expensive over the past several years.

Home prices remain well above pre-pandemic levels, while mortgage rates continue to hover above 6% in many markets. At the same time, insurance costs, property taxes, and maintenance expenses have all increased.

Although many people still view homeownership as a long-term wealth-building strategy, experts say buyers should carefully evaluate the full financial picture before making a decision.

For some households, renting provides greater flexibility and may produce better financial results over time.

Buying Doesn’t Always Pay Off Right Away

One of the biggest misconceptions about homeownership is that buying automatically creates wealth faster than renting.

Recent housing data suggests otherwise.

In many markets across the United States, the average buyer may not financially outperform renting for roughly six years after purchasing a home.

In several expensive metropolitan areas, including Seattle, Los Angeles, and Austin, it could take between 17 and 23 years before buying becomes financially advantageous compared with renting.

Some high-cost markets may even favor renting over an entire 30-year period when all ownership costs are included.

This highlights an important reality: how long you plan to stay in a home matters almost as much as the purchase price itself.

Location Plays a Major Role

The rent-versus-buy calculation varies dramatically across the country.

In many affordable Midwestern and Southern cities, the monthly cost difference between owning and renting is relatively small.

Markets such as:

- Columbus

- Indianapolis

- Cincinnati

- Buffalo

- Memphis

often allow buyers to recover ownership costs within four to five years.

In expensive coastal markets, however, high home prices and mortgage costs can significantly extend the break-even period.

Consumers should focus on local market conditions rather than national averages when making housing decisions.

Renting Has Financial Advantages

Renting is often viewed as simply paying someone else’s mortgage, but financial experts say that perspective overlooks several important benefits.

Renters generally enjoy:

- Greater flexibility.

- Lower upfront costs.

- Fewer unexpected expenses.

- Easier relocation for career opportunities.

- More liquid savings.

Unlike homeowners, renters typically do not have to worry about replacing roofs, repairing plumbing systems, or paying for expensive home maintenance projects.

For people who move frequently or expect career changes, renting can provide valuable financial freedom.

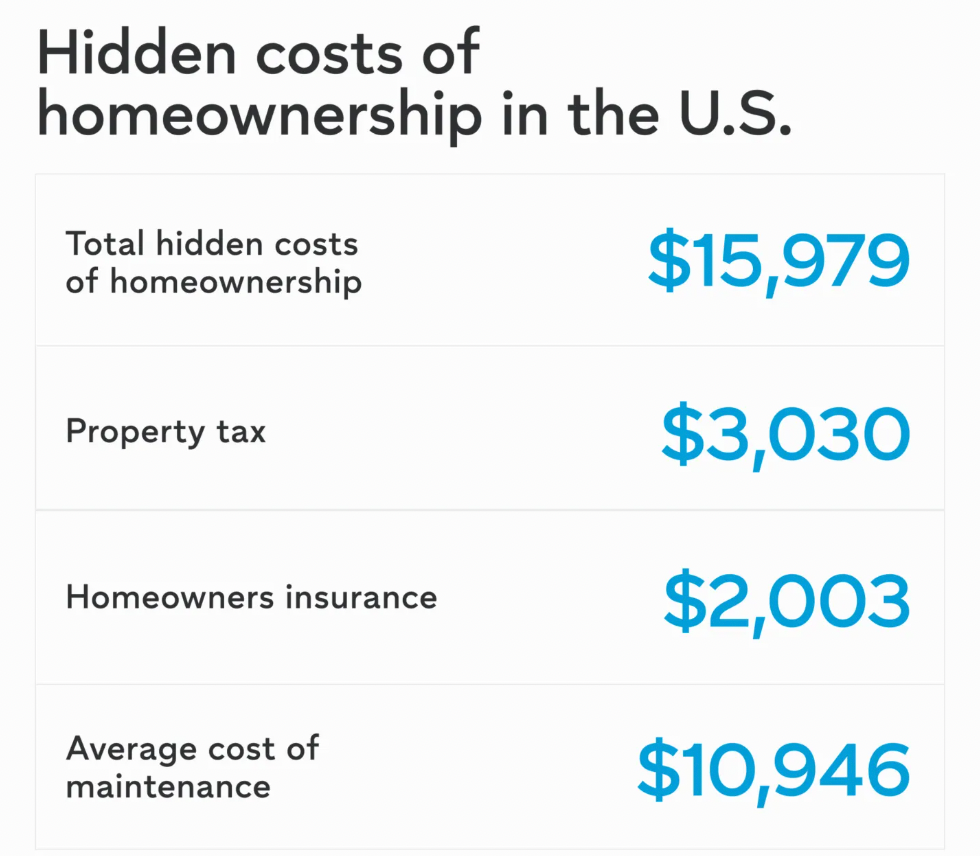

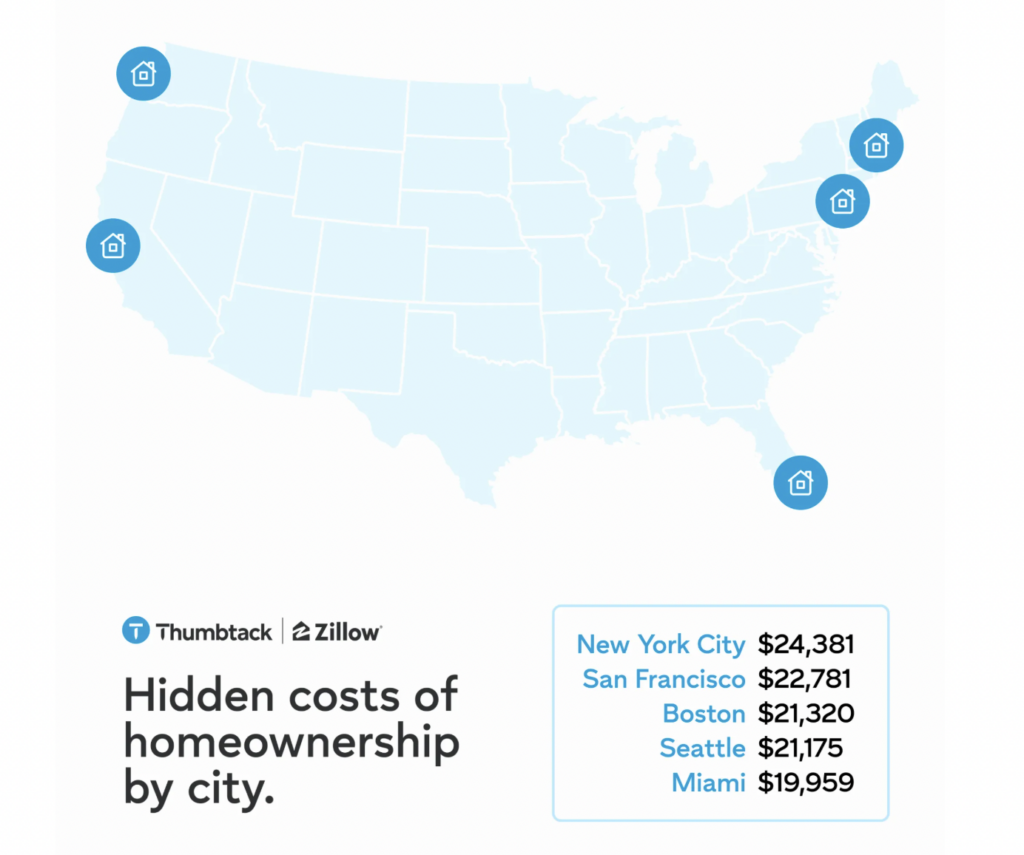

Hidden Costs of Homeownership Add Up

Many first-time buyers focus primarily on the monthly mortgage payment.

However, owning a home involves many additional expenses that can significantly affect the overall cost.

These may include:

- Property taxes.

- Homeowners insurance.

- Routine maintenance.

- Emergency repairs.

- Landscaping.

- Appliance replacement.

- HOA fees.

- Utility upgrades.

Recent housing estimates suggest these hidden ownership expenses now average nearly $16,000 annually nationwide.

That works out to more than $1,300 per month beyond the mortgage payment itself.

Ignoring these costs can lead buyers to underestimate the true financial commitment of owning a home.

Investing the Down Payment Is Another Option

One part of the rent-versus-buy discussion that often receives less attention involves opportunity cost.

When purchasing a home, buyers may commit tens of thousands of dollars toward a down payment.

Renters, on the other hand, can potentially invest that money elsewhere.

If those funds are invested consistently over many years, they may generate significant returns, especially in markets where owning costs substantially more than renting.

This does not mean renting is always better, but it highlights that home equity is only one path toward building wealth.

Financial growth can come through diversified investments as well.

Bigger Down Payments Are Not Always Better

Many consumers believe making the largest possible down payment is the smartest strategy.

However, financial experts suggest that isn’t always true.

In some situations, a smaller down payment can improve long-term financial outcomes because it allows buyers to keep more money invested elsewhere.

For example, a 5% down payment may outperform a 20% down payment if the invested savings generate returns that exceed the additional mortgage costs.

The ideal down payment depends on:

- Mortgage rates.

- Investment opportunities.

- Personal savings goals.

- Emergency fund needs.

- Local housing conditions.

Every buyer’s situation is different.

Homeownership Offers Stability

Despite rising costs, buying a home still provides important benefits.

Homeowners often appreciate:

Predictable Housing Costs

Fixed-rate mortgages provide stable principal and interest payments that do not increase with lease renewals.

Building Equity

Monthly mortgage payments gradually increase ownership in the property.

Long-Term Wealth Creation

Historically, homeownership has played a major role in household wealth accumulation.

Personal Control

Owners have greater freedom to renovate, customize, and improve their property.

For many families, these advantages extend beyond simple financial calculations.

The Emotional Side of Owning a Home

Buying a house is more than an investment decision.

Homeownership also brings responsibilities that many first-time buyers underestimate.

Unexpected repairs, maintenance projects, insurance claims, and ongoing upkeep can create stress.

Recent homeowner surveys suggest many owners worry about the financial demands of maintaining their properties, with some describing ownership as a second full-time job.

Before buying, consumers should honestly assess whether they are prepared for both the financial and personal responsibilities involved.

How to Decide Between Renting and Buying

There is no universal answer to the rent-versus-buy question.

The right choice depends on several personal factors, including:

- How long you plan to stay.

- Your financial stability.

- Local housing prices.

- Mortgage rates.

- Career flexibility.

- Savings goals.

- Maintenance responsibilities.

- Family plans.

A home should fit both your financial situation and your lifestyle goals.

Bottom Line

The traditional belief that buying is always better than renting is becoming less accurate in today’s housing market. Rising home prices, higher mortgage rates, and increasing ownership costs have changed the financial equation for many Americans.

While homeownership remains an important path to long-term financial stability, renting can also be a smart financial strategy depending on location, investment opportunities, and personal circumstances. The best decision is not based on old assumptions but on careful planning, local market conditions, and a realistic understanding of the true costs and benefits of both options.

For today’s consumers, education, patience, and thorough financial analysis remain the most valuable tools when deciding whether to rent or buy a home. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses