Harvard Housing Report: Affordability Reaches a Breaking Point in 2026

The U.S. housing market continues to face one of its most difficult affordability challenges in decades, according to Harvard University’s 2026 State of the Nation’s Housing report. While housing supply has gradually improved in several markets, elevated home prices, high mortgage rates and slowing economic growth continue to keep many buyers and renters on the sidelines.

The annual report from Harvard’s Joint Center for Housing Studies (JCHS) paints a picture of a housing market where supply is beginning to recover, but affordability remains the biggest obstacle. New construction has helped ease shortages in some regions, yet millions of households still struggle to buy a home or afford rising rents.

The report also highlights widening financial pressure on lower-income families, slowing household formation, and a growing need for additional housing policies that expand affordability across the country.

Housing Market Activity Remains Slow

Housing activity has remained subdued throughout early 2026.

Existing home sales continue to recover slowly after falling to their lowest level in nearly three decades during 2023. New home sales have remained relatively steady, but overall buyer demand remains below historical averages.

The report also notes several signs of slower market activity:

- Existing home sales remain below normal levels.

- New home sales have changed little over the past year.

- Apartment turnover has slowed as renters stay in place longer.

- New lease activity has weakened.

- Total housing starts declined about 1% over the past year.

- Single-family housing starts fell roughly 7%.

These trends suggest that both buyers and builders remain cautious as affordability pressures continue to weigh on the market.

Demand Is Slowing Across the Housing Market

One of the report’s most important findings is that weaker demand has become almost as significant as limited supply.

Household formation slowed for the third consecutive year during 2025, reducing the number of new buyers entering the housing market.

Growth in homeowner households also slowed significantly, contributing to a second consecutive annual decline in the national homeownership rate.

Rental demand has also softened. The increase in renter households during the first quarter of 2026 was less than half the pace recorded a year earlier.

Rather than reflecting a lack of interest in homeownership or renting, the report suggests many households simply cannot afford current housing costs.

Economic Conditions Are Reducing Housing Demand

Several economic factors have contributed to weaker housing demand.

Job growth slowed sharply during 2025, reducing confidence among households considering major financial decisions.

Consumer confidence also weakened considerably throughout 2025 and reached one of its lowest levels in recent decades during early 2026.

When employment opportunities become less certain, many people delay:

- Buying a home

- Renting a larger apartment

- Moving to another city

- Starting a family

- Purchasing investment property

Recent college graduates are also more likely to remain with family or roommates until employment conditions improve.

These trends reduce overall housing demand even when supply begins to increase.

Housing Affordability Continues to Worsen

Affordability remains the largest challenge facing today’s housing market.

Median prices for both new and existing homes now exceed $400,000 nationwide.

Since 2020:

- Existing home prices have increased approximately 54%.

- Home values have risen to nearly five times median household income.

- Mortgage rates have remained above 6%.

- Monthly payments for a typical home have increased dramatically.

The report estimates that financing a median-priced home required a monthly payment of approximately $3,100 during late 2025, compared with roughly $1,700 in early 2020.

As a result, a household now needs annual income exceeding $120,000 to comfortably afford a median-priced home, compared with approximately $66,000 just a few years earlier.

This widening affordability gap has priced many middle-income families out of homeownership.

Housing Supply Is Gradually Improving

Although affordability remains difficult, housing inventory has started improving.

Multifamily construction expanded significantly after 2022, while single-family construction has remained relatively steady.

As more housing units entered the market:

- Rental vacancy rates increased from 5.9% in 2022 to 7.3% during the first quarter of 2026.

- Homes available for sale also increased modestly.

- For-sale vacancy rates rose from 0.81% in 2023 to 1.13%.

These vacancy levels are moving closer to historical averages observed during the 1990s.

Greater inventory gives buyers and renters more choices than they had during the extremely tight housing markets of recent years.

Housing Recovery Differs by Region

The report emphasizes that housing conditions vary widely across local markets.

Cities with significant new construction have experienced much larger increases in housing availability.

For example:

Austin, Texas

- Apartment vacancy rates increased by roughly five percentage points since 2021.

- Homes listed for sale have nearly tripled.

Chicago, Illinois

- Apartment vacancy rates increased only about half a percentage point.

- Homes available for sale declined roughly 20%.

These differences illustrate why national housing statistics often fail to reflect local market conditions.

Some metropolitan areas are moving toward balanced markets, while others continue facing severe inventory shortages.

Affordable Housing Remains in Short Supply

While housing inventory has improved overall, affordable housing remains extremely limited.

Much of the new apartment construction completed over the past decade has focused on higher-priced rental properties.

Meanwhile, the number of rental units priced below $1,000 per month has declined by approximately 7 million as older apartments were renovated, demolished or converted into higher-priced housing.

Affordable homes for purchase have also become increasingly difficult to find.

Homes affordable for households earning $75,000 or less annually have fallen roughly 60% compared with 2019.

For many first-time buyers, inventory has expanded primarily in higher price ranges rather than in entry-level housing.

Low-Income Renters Face the Greatest Challenge

The report identifies extremely low-income renters as the group facing the largest housing shortage.

Approximately 11 million extremely low-income renter households compete for only 3.8 million affordable and available rental units.

This creates an estimated shortage of 7.2 million affordable homes for the households that need them most.

Without significant expansion of affordable housing programs, this gap is expected to remain one of the nation’s largest housing challenges.

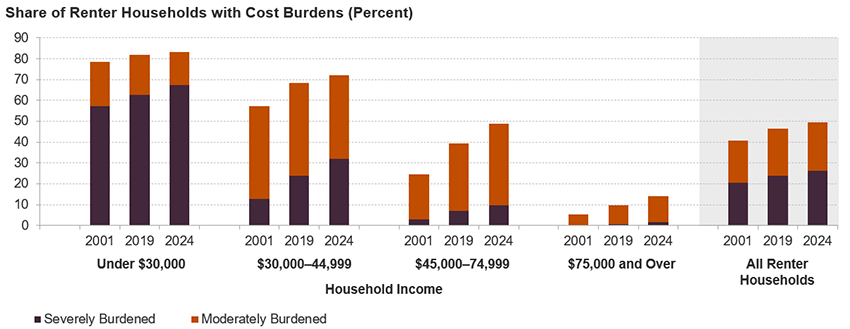

Housing Cost Burdens Continue to Rise

Housing expenses continue consuming a growing share of household income.

The report shows that renter cost burdens reached another record level during 2024.

Among renters earning less than $30,000 annually:

- 83% spend more than 30% of income on housing.

- 66% spend more than 50% of income on housing.

Financial stress has also increased among lower-income homeowners.

In addition to mortgage payments, many households face higher:

- Homeowners insurance premiums

- Property taxes

- Utility bills

- Energy costs

- Maintenance expenses

Combined with inflation, these costs continue reducing household purchasing power.

Families Have Less Money for Everyday Needs

As housing consumes a larger portion of household budgets, less income remains available for daily living expenses.

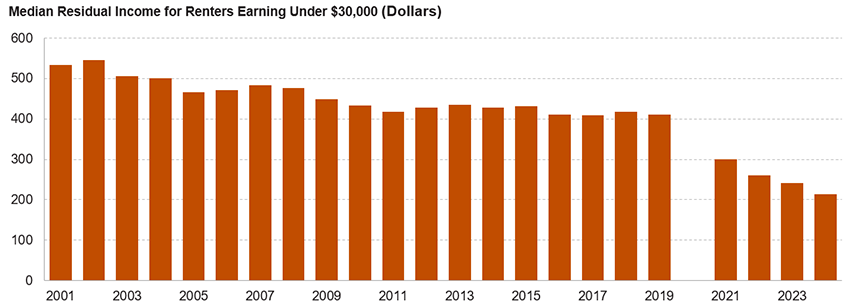

The report estimates that renter households earning under $30,000 annually have a median of only $210 per month remaining after paying housing costs.

That amount must cover:

- Food

- Transportation

- Health care

- Clothing

- Child care

- Utilities

- Household supplies

Only a few years earlier, comparable households had approximately $410 remaining after housing expenses.

Although wages have increased for many workers, inflation has significantly reduced purchasing power.

Governments Continue Pursuing Housing Solutions

Many state and local governments have introduced new initiatives to increase housing supply.

The report highlights efforts that include:

- Updating zoning regulations

- Simplifying permitting processes

- Supporting affordable housing construction

- Creating revolving construction loan funds

- Expanding local financing programs

- Reducing regulatory barriers

These reforms aim to increase the number of homes built while improving affordability over the long term.

Because housing markets differ significantly across regions, many solutions are being developed at the local level rather than through a single nationwide approach.

Federal Housing Programs Continue to Expand

The report also recognizes several recent federal housing initiatives.

Additional funding has been directed toward affordable housing programs, including the Low-Income Housing Tax Credit, which remains one of the nation’s largest incentives for developing affordable rental housing.

The report also points to continued discussions surrounding the 21st Century ROAD to Housing Act, which seeks to increase housing production, improve financing options and reduce some regulatory barriers to construction.

While these measures may support future housing development, researchers emphasize that significantly more investment will be required to close the nation’s affordable housing gap.

What the Report Means for Homebuyers

For prospective buyers, the report suggests that affordability may remain difficult despite improving inventory.

More homes are becoming available in certain markets, giving buyers additional choices and slightly more negotiating power.

However:

- Mortgage rates remain elevated.

- Home prices remain near record highs.

- Entry-level housing remains limited.

- Monthly payments remain historically expensive.

Buyers who have stable employment, strong credit and adequate savings may find more opportunities than they did during the intense seller’s market of recent years.

What It Means for Real Estate Investors

The report presents both opportunities and challenges for investors.

Markets experiencing increased inventory may provide additional purchasing opportunities, particularly where construction has expanded rapidly.

At the same time, investors should recognize that:

- Rent growth has moderated.

- Vacancy rates have increased.

- Insurance costs continue rising.

- Property taxes remain elevated in some regions.

- Operating expenses have increased.

Long-term investment decisions should continue focusing on local market fundamentals rather than national averages.

Population growth, employment trends, rental demand and new construction remain among the most important factors affecting future investment performance.

Looking Ahead

The Harvard report concludes that the housing market is beginning to stabilize after several years of extraordinary disruption.

Supply conditions have improved, but affordability remains the central issue limiting both homeownership and rental mobility.

Without additional construction—particularly of lower-priced homes—and continued policy support, millions of households are likely to remain priced out of both homeownership and affordable rental housing.

The report suggests meaningful progress will require coordinated action from federal, state and local governments alongside continued private-sector investment.

Final Thoughts

Harvard’s 2026 State of the Nation’s Housing report illustrates a market that is slowly recovering from severe supply shortages but continues to struggle with historically high housing costs.

While builders have increased housing production and inventory has improved in many areas, elevated mortgage rates, expensive home prices and limited affordable housing continue preventing many Americans from purchasing homes or finding reasonably priced rentals.

For buyers, renters and investors alike, affordability not inventory remains the defining challenge of the U.S. housing market in 2026. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses