Inflation, Mortgage Rates, and Housing: Why the Market Faces New Challenges

The U.S. housing market continues to face challenges as stronger economic data and higher inflation keep mortgage rates elevated. While affordability improved slightly earlier this year, recent developments have reduced optimism for a stronger housing recovery during 2026.

Strong employment growth, rising consumer prices, and persistent housing inflation are creating additional obstacles for buyers already dealing with expensive home prices and elevated borrowing costs.

Strong Economy Pushes Interest Rates Higher

Recent economic reports showed that the U.S. economy remains resilient.

The labor market added approximately 172,000 jobs during May, far exceeding expectations, while unemployment remained relatively stable. Revisions to earlier months also added more jobs than initially reported, easing concerns that hiring activity was slowing sharply.

Inflation data added another challenge. Consumer prices accelerated to an annual rate of 4.2%, with energy costs contributing significantly to the increase. Core inflation remained elevated, indicating that price pressures have not fully disappeared.

These developments have strengthened expectations that interest rates could remain higher for longer.

As Treasury yields increased, mortgage rates also moved higher, making home financing more expensive.

Housing Affordability Remains Fragile

Although affordability has improved somewhat compared with last year, those gains remain vulnerable.

Mortgage rates and monthly payments are still slightly lower than year-ago levels, and a larger share of homes remains affordable for median-income households than during the worst affordability period.

However, any increase in mortgage rates can quickly erase these improvements.

At the same time, inflation is reducing household purchasing power. Rising costs for food, energy, insurance, and other necessities are making it harder for many families to save for down payments or qualify for mortgages.

Housing Market Activity Slows

Recent market data reflects the growing affordability challenges.

Both home sales and new listings have weakened compared with earlier expectations.

Many housing analysts now believe overall sales activity could remain relatively flat during 2026 instead of showing a stronger recovery.

Potential buyers continue to face:

- Elevated home prices.

- Higher mortgage rates.

- Inflation pressures.

- Economic uncertainty.

- Concerns about future Federal Reserve policy.

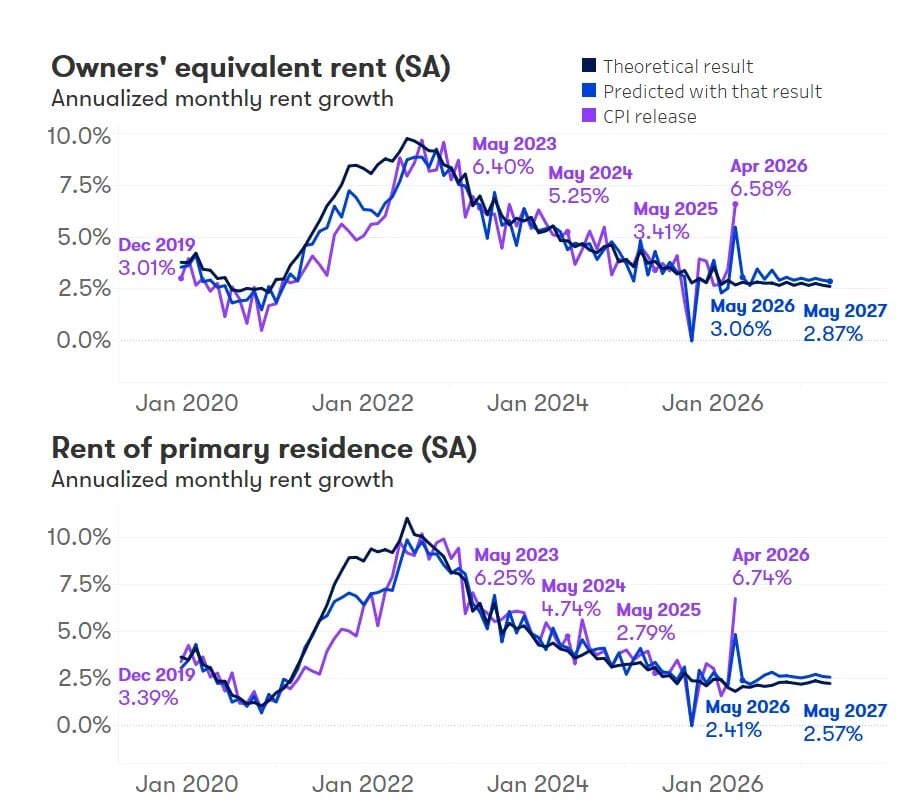

Shelter Inflation Remains Elevated

Housing-related inflation continues to be one of the largest contributors to overall consumer prices.

Two major measures receive close attention from economists:

Owner’s Equivalent Rent

Owner’s Equivalent Rent estimates what homeowners would pay if they rented their own homes.

Analysts expect this measure to continue increasing steadily during 2026, with annual growth remaining above 3%.

Rent of Primary Residence

This measure tracks actual rental payments made by tenants.

While rental inflation has moderated from pandemic highs, annual growth remains positive and continues contributing to overall inflation.

Shelter Inflation Forecast Table

| Period | OER MoM Forecast | OER MoM Actual | OER YoY Forecast | OER YoY Actual | Rent MoM Forecast | Rent MoM Actual | Rent YoY Forecast | Rent YoY Actual |

|---|---|---|---|---|---|---|---|---|

| December 2025 | 0.27% | 0.31% | 3.25% | 3.36% | 0.21% | 0.27% | 2.93% | 2.92% |

| January 2026 | 0.26% | 0.22% | 3.29% | 3.26% | 0.21% | 0.25% | 2.78% | 2.84% |

| February 2026 | 0.18% | 0.22% | 3.14% | 3.19% | 0.19% | 0.13% | 2.74% | 2.68% |

| March 2026 | 0.21% | 0.28% | 3.02% | 3.10% | 0.17% | 0.19% | 2.55% | 2.56% |

| April 2026 | 0.44% | 0.53% | 3.20% | 3.30% | 0.39% | 0.55% | 2.63% | 2.79% |

| May 2026 | 0.25% | — | 3.27% | — | 0.20% | — | 2.76% | — |

Rental Market Outlook

Rental markets are also showing renewed strength.

Single-family rental growth expectations have increased, with annual gains projected to reach approximately 3.2% by the end of 2026.

Apartment rents are also expected to strengthen. Multifamily rental growth forecasts have improved and are projected to rise around 2.1% annually.

While these increases remain below the rapid gains experienced during the pandemic, they suggest that rental demand remains healthy.

Why Housing Inflation Is Staying High

Housing inflation had been slowing steadily over the past few years, but that trend now appears to be leveling off.

Several factors are contributing to this change.

Landlords continue facing higher operating expenses, including insurance, maintenance, taxes, and financing costs.

At the same time, stronger leasing activity during the spring rental season has encouraged property owners to increase rents across their portfolios.

However, economists do not expect another major surge in rent growth.

Vacancy rates have largely returned to historical averages, and market rents remain relatively balanced, reducing the likelihood of excessive price increases.

Mortgage Rates Continue to Influence Housing

Higher mortgage rates remain one of the biggest challenges for the housing market.

As financing costs increase, buyers often reduce their budgets or postpone purchasing decisions altogether.

Higher borrowing costs also discourage existing homeowners from selling because many have mortgages with significantly lower interest rates.

This combination limits market activity while helping support home prices.

What This Means for Buyers

Today’s market remains difficult but not impossible for buyers.

Those with stable employment, strong credit, and long-term housing plans may still find opportunities, particularly in markets with improving inventory and slower price growth.

Buyers should carefully evaluate monthly affordability rather than focusing solely on home prices.

Shopping among lenders and improving credit profiles can also help reduce financing costs.

Housing Market Outlook

The outlook for the remainder of 2026 depends heavily on inflation and interest rates.

If inflation gradually moderates, mortgage rates could stabilize and support improved housing activity.

If inflation remains elevated, borrowing costs could stay high and slow the pace of recovery.

Many economists expect the housing market to continue adjusting rather than experiencing a major boom or significant downturn.

Bottom Line

Higher inflation and rising mortgage rates are creating new obstacles for the U.S. housing market. Strong job growth and elevated consumer prices have reduced expectations for lower interest rates, keeping borrowing costs relatively high.

Although affordability has improved modestly from last year, many households continue to face financial pressure from rising living expenses and expensive housing. Shelter inflation remains elevated, while rental markets continue to show moderate growth.

The housing recovery has not stopped, but its pace has slowed considerably. Future progress will largely depend on inflation trends, mortgage rates, and overall economic conditions during the second half of 2026. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses