A New Normal for U.S. Mortgage Rates?

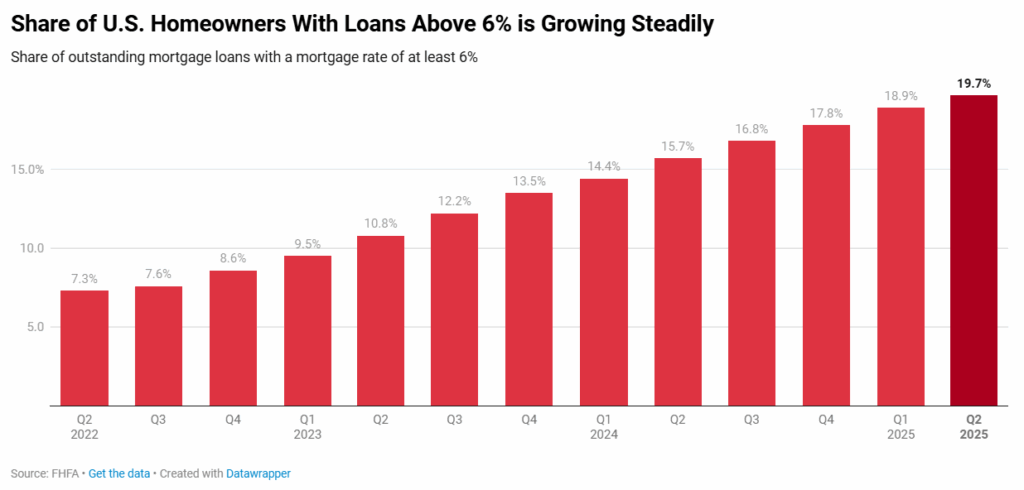

Mortgage rates in the U.S. have entered what may be a “new normal” for homeowners and buyers alike. According to the latest Redfin analysis, the share of mortgaged homeowners paying at least 6% climbed to 19.7% in Q2 2025, the highest level observed since 2015. With weekly average mortgage rates remaining above 6% since September 2022, this trend has steadily increased, rising between 0.8 and 1.4 percentage points per quarter over the past two years.

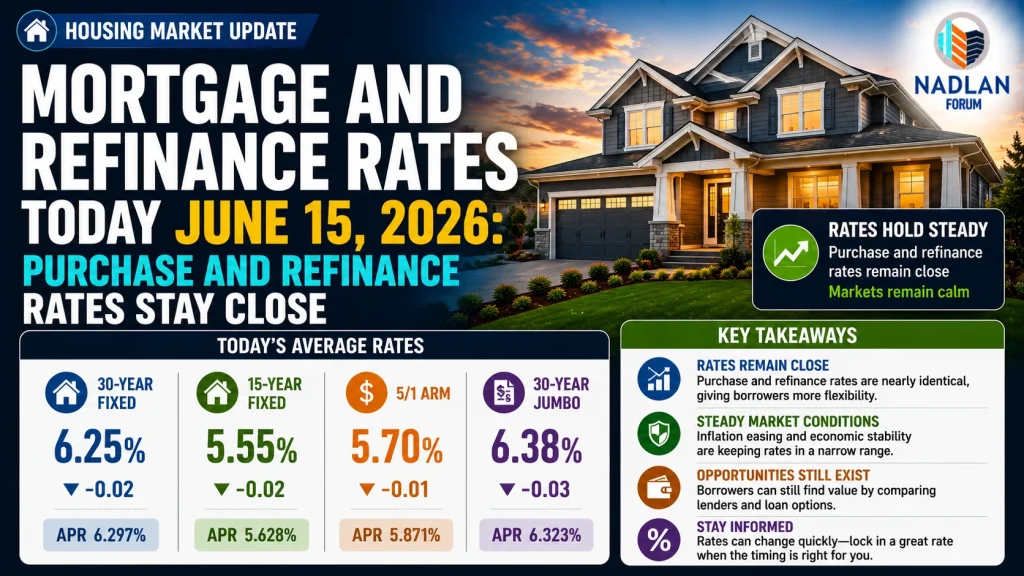

Redfin’s report used data from the Federal Housing Finance Agency’s National Mortgage Database through Q2 2025. For much of this year, mortgage rates have fluctuated between 6% and 7%, reaching a low of 6.13% in August just prior to the Federal Reserve’s interest rate cut, and rising back to 6.38% as of late September. Economists at Redfin predict that rates are likely to remain within this 6%-7% range over the next 12 months.

Pandemic Lock-In and Its Legacy

During the 2020-2022 pandemic housing boom, historically low mortgage rates fueled a surge in home sales, with at least one-third of mortgages refinanced and existing home sales climbing to decade highs. This created a lock-in effect, where many homeowners opted to stay put rather than trade up or relocate, given the prospect of paying significantly higher rates elsewhere.

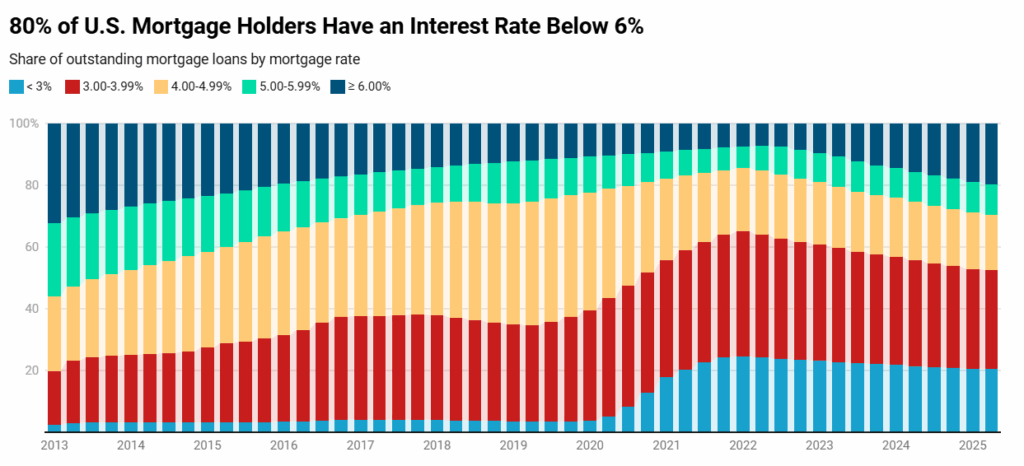

However, the lock-in effect is gradually diminishing. The share of homeowners with sub-3% mortgages has declined to 20.4% in Q2 2025, down from 24.6% in Q1 2021. Likewise, the proportion of mortgages under 6% dropped from 92.7% three years ago to 80.3% today, reflecting a slow but notable shift in homeowners’ willingness to navigate a higher-rate environment.

Chen Zhao, Redfin’s Head of Economics Research, observed:

“More homeowners are deciding it’s worth moving even if it means giving up a lower mortgage rate. Life doesn’t stand still people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood. Those needs are starting to outweigh the financial benefit of clinging to a rock-bottom mortgage rate. As a result, more homes are hitting the market than we’ve seen in years, giving buyers a wider range of choices.”

Buyer Hesitancy Despite More Listings

Even with the increase in inventory and a slight dip in rates, homebuyers remain cautious. Mariah O’Keefe, a Redfin Premier agent in Seattle, commented:

“A lot of people want to buy and they’re just hanging around waiting. Rates have not gone down significantly enough to move the needle prospective buyers need to see a bigger difference in their potential monthly payment. If rates tick down below 6%, that will bring a lot of people back into the market.”

This cautious stance underscores how sensitive today’s buyers are to even small shifts in interest rates.

Mortgage Rate Distribution Among Homeowners

Redfin’s analysis also provides a detailed breakdown of current mortgage rates for U.S. homeowners:

| Rate Range | Share of Homeowners | Notes |

|---|---|---|

| Below 3% | 20.4% | Lowest since Q2 2021 |

| 3%-3.99% | 32.1% | Lowest since Q3 2019 |

| 4%-4.99% | 17.9% | Lowest share since 2013 |

| 5%-5.99% | 9.5% | Lowest since Q3 2024 |

| ≥6% | 19.7% | Highest share since Q4 2015 |

| Below 4% | 52.5% | Down from 65.1% in Q1 2022 |

| Below 5% | 70.4% | Down from 85.6% in Q1 2022 |

| Below 6% | 80.3% | Down from 92.7% in Q2 2022 |

This data highlights the gradual normalization of mortgage rates at higher levels, signaling a departure from the ultra-low-rate environment of the past several years.

What This Means for the Market

The trend toward higher mortgage rates may encourage some homeowners to list their properties, boosting inventory and giving buyers more options. At the same time, buyers remain rate-sensitive, waiting for rates to dip closer to or below 6% before committing.

Economists suggest that the market is gradually adjusting to a more balanced, mid-range rate environment, where homeowners are less tethered to historically low mortgages but buyers are cautious about affordability.

In essence, the “new normal” could see rates hovering between 6% and 7% for an extended period, shaping both homebuyer behavior and market dynamics well into 2026. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses