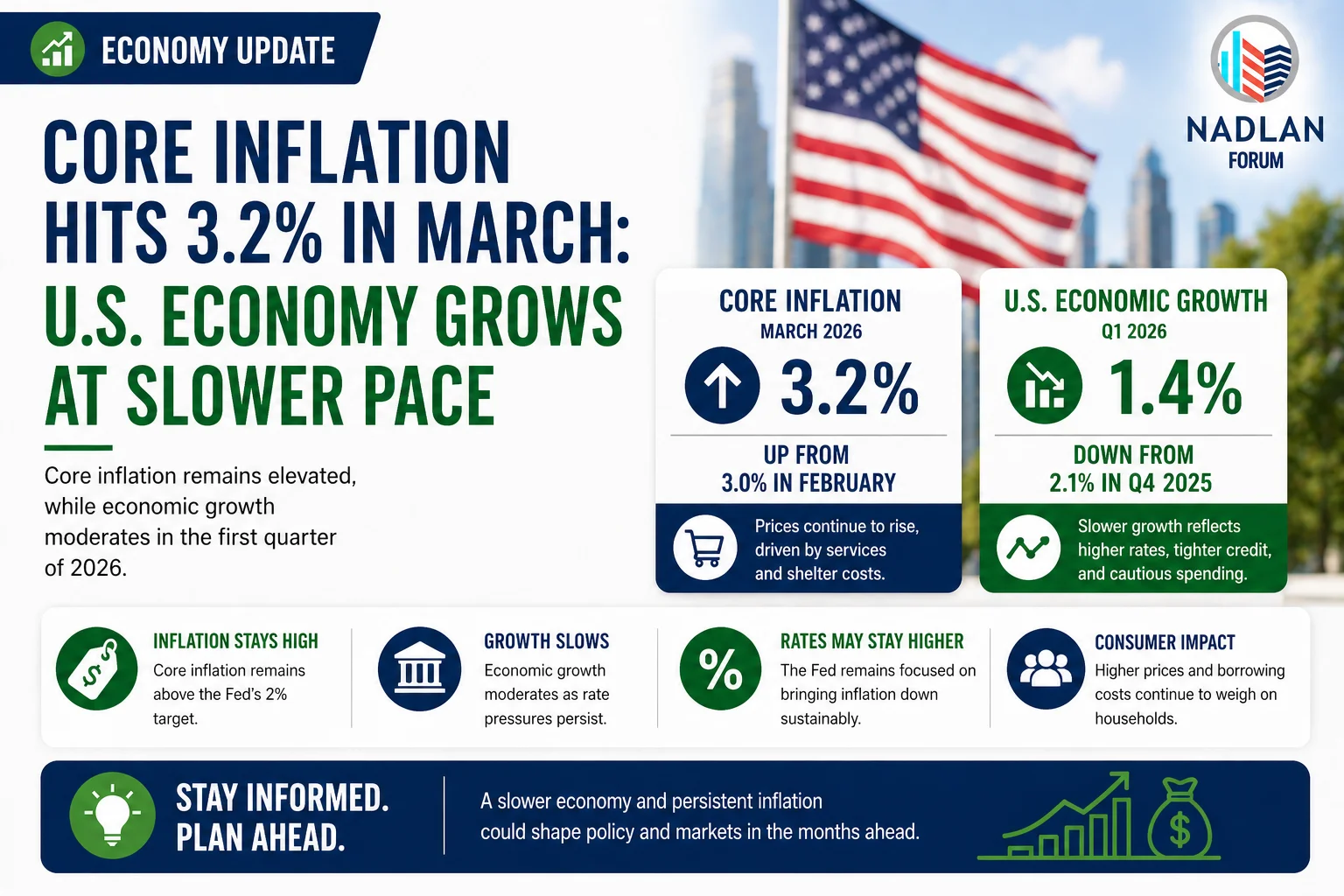

FICO Introduces Direct License Program to Revolutionize Mortgage Credit Scoring

In a significant move for the mortgage industry, FICO has launched its FICO Mortgage Direct License Program, a game-changing initiative that aims to streamline the delivery of FICO Scores to mortgage lenders, brokers, and other industry stakeholders. This new approach removes the reliance on the traditional tri-merge resellers and the three nationwide credit bureaus, creating a more transparent and cost-efficient system for mortgage professionals.

As mortgage lenders have long depended on third-party resellers to access FICO Scores, this new program empowers them to bypass intermediaries and directly access credit scores, which will allow for greater price transparency, reduce unnecessary markups, and lead to significant cost savings. This move is expected to drive more competition within the industry and help reduce the overall cost of doing business in the mortgage market.

A New Era of Pricing and Transparency

FICO’s Chief Executive Officer, Will Lansing, emphasized that the direct licensing of FICO Scores represents a transformative shift in the way credit scores are priced and delivered across the mortgage lending sector. “This change will eliminate unnecessary markups on the FICO Score and give more control over pricing models to the entities making the mortgage decisions,” said Lansing. “We are eliminating intermediaries and opening up a more transparent and competitive market.”

The new program is designed with two primary pricing models for lenders to choose from:

Performance Model – Under this model, FICO offers a reduced royalty fee of $4.95 per score, cutting average costs by 50% compared to the previous pricing structure. This performance model recognizes the FICO Score’s importance in driving mortgage liquidity and supporting the broader mortgage ecosystem. A $33 per borrower per score fee is applied when a mortgage loan is closed. This fee replaces the previously charged fees for re-issuing FICO Scores, allowing for more extensive usage within the mortgage market, including by mortgage insurers, GSEs, investors, and rating agencies.

Standard Per Score Model – This model maintains the previous cost structure of $10 per score for resellers, ensuring that there is no increase in costs for lenders who prefer to continue using the existing pricing model.

Empowering the Mortgage Industry

FICO’s move to directly license its credit scores is aimed at improving the overall efficiency of the mortgage process. By streamlining the distribution of credit scores, the FICO Mortgage Direct License Program will empower tri-merge resellers, making it easier for mortgage lenders to access the information they need while lowering overall costs. This creates a win-win situation for lenders and borrowers alike, ensuring that the mortgage process remains affordable and accessible.

FICO’s new pricing structure was met with praise from William Pulte, Director of the Federal Housing Finance Agency (FHFA), who commended FICO for responding to industry feedback. On social media, he acknowledged FICO’s efforts to make the mortgage market more competitive and transparent, noting that such moves were essential for creating a more stable and secure environment for American consumers. Pulte also called on other major players, like the credit bureaus and VantageScore, to adopt similar measures to enhance competition in the market.

Industry Reactions

The Mortgage Bankers Association (MBA) has also shown strong support for FICO’s new program, seeing it as a significant step toward resolving the longstanding concerns over the high costs of credit reporting in the mortgage industry. Bob Broeksmit, President and CEO of MBA, stated, “FICO’s new direct license program is a much-needed change that enhances transparency and gives mortgage lenders more pricing options. We’ve been calling for reforms in the credit reporting sector, and this program represents an important move in the right direction.”

FICO’s decision to offer its new mortgage score pricing models to the three major credit bureaus on the same terms also signals a shift toward a more level playing field within the industry, although FICO will not control any additional markups the bureaus may impose.

What This Means for Lenders and Borrowers

For lenders, the new direct license program offers several key benefits:

- Cost savings through reduced per-score fees

- Greater pricing flexibility, allowing lenders to choose between different models based on their needs

- Transparency, as it eliminates hidden costs and markups from third-party resellers

- Improved competition in the market, which may lead to better pricing for consumers

For homebuyers, particularly those purchasing homes with conventional mortgages, this shift could eventually lead to lower costs as lenders pass on savings from more efficient credit score pricing. Additionally, borrowers could benefit from a more streamlined mortgage process, as the flow of credit data becomes more direct and less dependent on intermediaries.

Looking Forward: A Changing Landscape for Credit Scores

The launch of FICO’s Mortgage Direct License Program is a pivotal moment in the mortgage and credit scoring industries. As transparency increases and costs decrease, it is expected that the entire mortgage ecosystem will become more efficient, driving better outcomes for both lenders and homebuyers. In the future, more competition could emerge as other credit score providers are prompted to reconsider their own pricing models and structures.

Ultimately, FICO’s new program is poised to reshape the way mortgage lenders, brokers, and other industry participants interact with credit scoring data, marking a significant shift toward more efficiency and fairness in the mortgage market. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses