Homeowners Could Be Forced to Give Up Their Low Mortgage Rates—Even If They Don’t Want To

For years, homeowners who locked in historically low mortgage rates during the pandemic have held a powerful advantage one that has also frozen much of the housing market. But new data from Realtor.com and Cotality suggest that this long-standing stalemate may soon begin to crack as economic pressures and life circumstances push more owners to move, even if it means letting go of their once-coveted low rates.

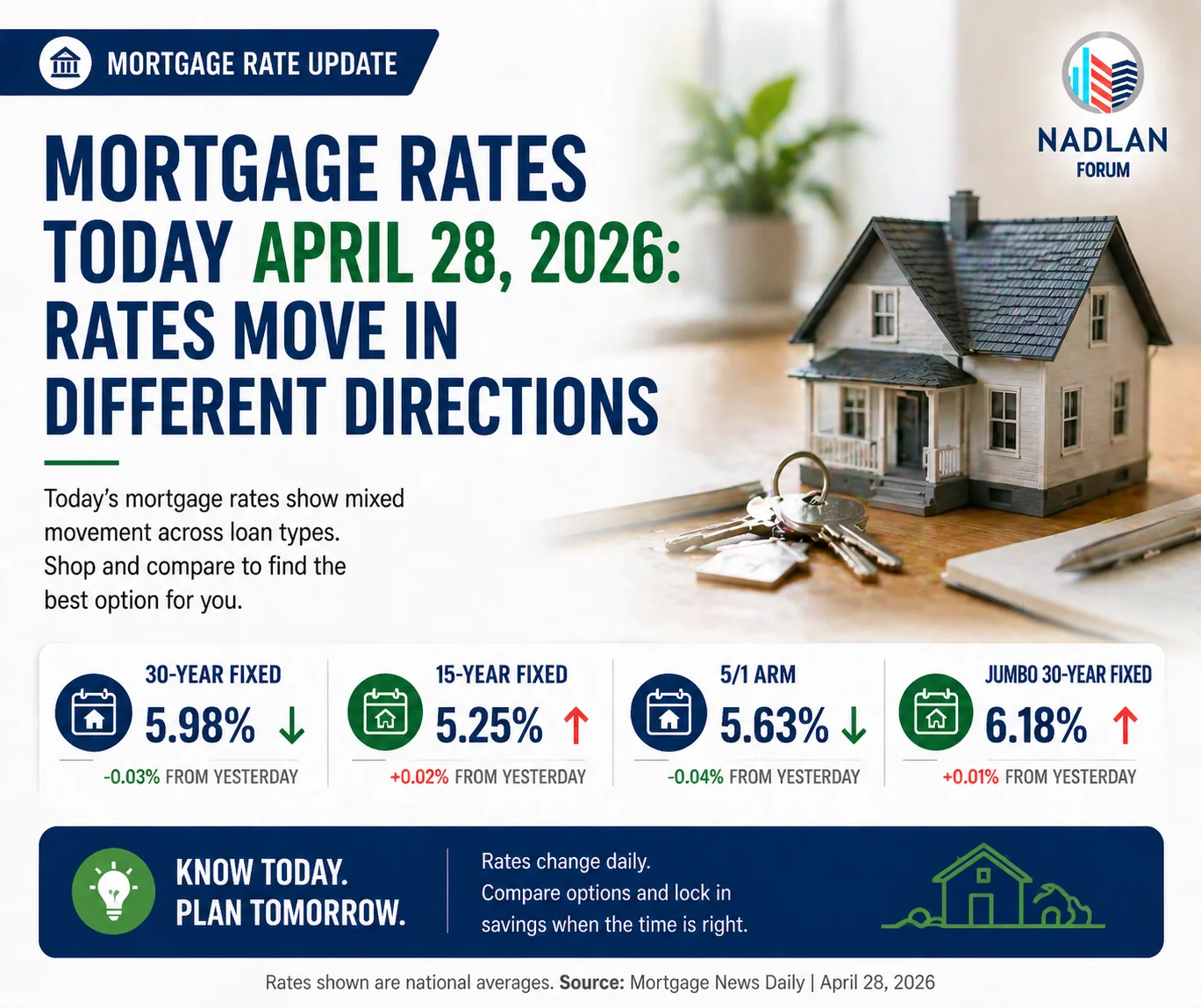

According to Realtor.com’s latest analysis, supported by data from Cotality, 52.5% of American homeowners currently have mortgage rates below 4% as of the second quarter of 2025. That’s roughly two percentage points lower than the prevailing rates, which have hovered in the low-to-mid 6% range for several months.

Before the pandemic, selling and upgrading homes was a normal part of household financial growth. But that dynamic has shifted dramatically, as homeowners especially those who refinanced during 2020–2021 now find themselves locked into ultra-cheap loans they can’t bear to replace.

The “Golden Handcuffs” of Low Rates

Cotality’s economists describe this as a case of “golden handcuffs”—a term that captures how today’s homeowners are trapped by the financial advantage of their existing loans.

“The difference between a 4% and a 6% mortgage rate can mean hundreds or even thousands of dollars more each month,” said Dr. Selma Hepp, Chief Economist at Cotality. “That gap has effectively frozen the market, particularly for move-up buyers, empty nesters, and people who might otherwise relocate for work or lifestyle reasons.”

The Federal Housing Finance Agency estimates that this “lock-in effect” prevented roughly 1.72 million home sales between 2022 and 2024. That represents a massive hit to the housing market’s natural turnover what economists call market churn.

“Transaction volume, especially for existing homes, has fallen to levels we haven’t seen in decades,” Hepp explained. “The high cost of moving has replaced mobility with stagnation.”

Inventory: Slowly Rebuilding, But Still Far Behind

Realtor.com’s September 2025 Housing Market Trends Report reinforces that story. It shows that while listings are gradually increasing, overall housing supply remains 14% below pre-pandemic levels. The pace of growth has slowed since May, signaling that most homeowners are still reluctant to list their properties despite improving market conditions.

Regional disparities tell an even more complex story. The South and West now have slightly more homes for sale than they did in 2019, largely due to new construction and migration shifts. In contrast, the Northeast and Midwest remain deeply undersupplied, with inventories still more than 50% below pre-pandemic levels.

The shortage of available homes continues to fuel price rigidity, even as higher mortgage rates keep many buyers on the sidelines. Nationally, the median list price in September held steady at $425,000, unchanged from last year. However, on a price-per-square-foot basis, values rose in the Midwest and Northeast, where competition for limited inventory remains fierce.

“Low supply tends to create tight conditions that favor sellers,” said Hepp. “Even when affordability is strained, scarcity can sustain price growth. In some cities, the ratio of buyers to available homes is still remarkably high.”

Buyers and Sellers Both Face a Stalemate

While falling mortgage rates have sparked a modest rise in home sales, both buyers and sellers are still wrestling with affordability pressures. For potential buyers, high home prices and interest rates have combined to create one of the toughest purchasing environments in recent memory.

The result: homes are sitting longer before selling. The average listed property in September stayed on the market for 62 days, up from 55 days a year earlier. Sellers are increasingly adjusting expectations—offering concessions or price cuts to attract buyers but demand remains constrained.

“For many first-time buyers, the math simply doesn’t work,” Hepp said. “Even small reductions in mortgage rates aren’t enough to offset high prices and rising living costs. That keeps a large segment of potential homeowners on the sidelines.”

This tug-of-war between low-rate homeowners and priced-out buyers has slowed what should be a cyclical housing market. Homeowners don’t want to sell because they can’t afford to buy again; buyers can’t buy because affordability is stretched to its limits.

The Turning Point Ahead

Despite the current gridlock, analysts believe that time and necessity will eventually break the deadlock. As families grow, jobs change, and life events unfold, many homeowners will have no choice but to move, even if it means giving up their low mortgage rates.

Additionally, if mortgage rates continue their gradual decline into 2026, more homeowners could reenter the market, easing inventory shortages and creating fresh opportunities for buyers.

“Eventually, mobility wins,” said one housing market strategist. “People will still need to move for work, retirement, or family reasons. The real question is whether rates will fall fast enough to make those moves financially feasible again.”

In the meantime, the market remains in a delicate balance. With limited supply, high prices, and a nation of homeowners clinging to historically cheap mortgages, the housing sector is still struggling to find its rhythm.

As Hepp summarized:

“The pandemic reshaped housing behavior in a way we’ve never seen before. The golden handcuffs won’t last forever but for now, they’re keeping a tight grip on the housing market.” For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses