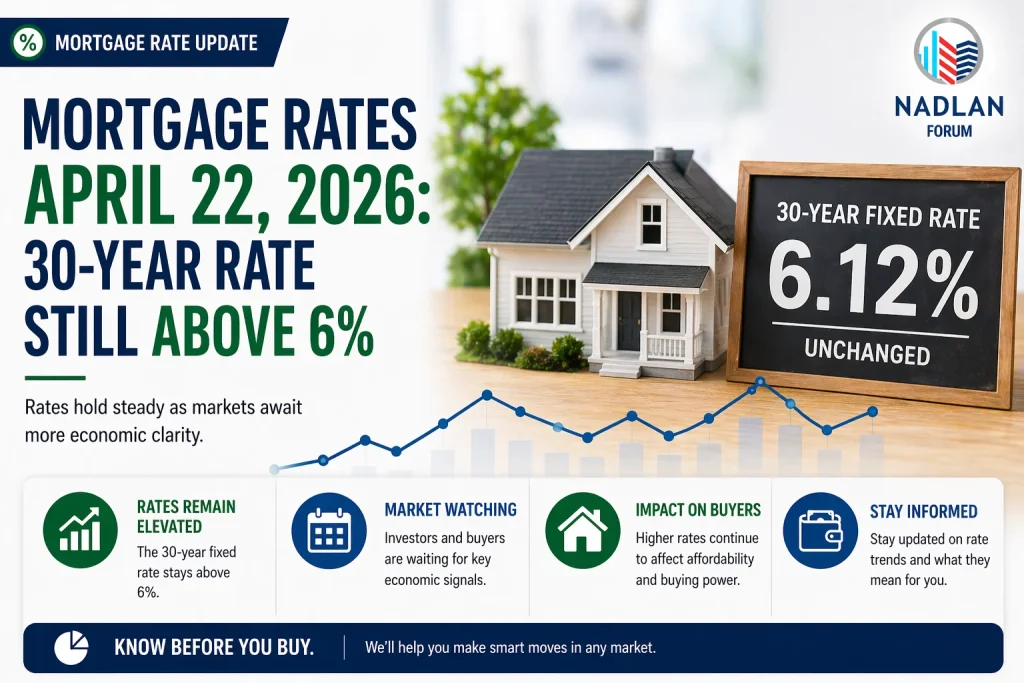

Mortgage Rates April 22, 2026: 30-Year Rate Still Above 6%

Rates Hover Near a Key Level

Mortgage rates are continuing to move within a narrow range, with the 30-year fixed rate still slightly above the 6% mark. According to the latest data from Zillow, the 30-year mortgage rate increased to 6.09%, while shorter-term loans remain below that level.

The current trend shows that while borrowing costs have eased compared to recent highs, the market is still waiting for a clear move below 6%, which many buyers see as an important threshold.

Today’s Mortgage Rates Overview

Here are the latest national average mortgage rates:

Purchase Rates:

- 30-year fixed: 6.09%

- 20-year fixed: 5.93%

- 15-year fixed: 5.55%

- 5/1 ARM: 6.32%

- 7/1 ARM: 6.17%

- 30-year VA: 5.48%

- 15-year VA: 5.16%

- 5/1 VA: 5.39%

Refinance Rates:

- 30-year fixed: 6.09%

- 20-year fixed: 5.93%

- 15-year fixed: 5.55%

- 5/1 ARM: 5.39%

- 7/1 ARM: 6.17%

- 30-year VA: 5.48%

- 15-year VA: 5.16%

- 5/1 VA: 5.39%

While refinance rates are often higher than purchase rates, current data shows they are very close, reflecting stable market conditions.

Why the 6% Level Matters

The 6% range has become a key psychological point for both buyers and lenders. When rates move below this level:

- Monthly payments become more manageable

- Buyer demand tends to increase

- Affordability improves slightly

Although rates have dropped from recent highs near 6.50%, they are still hovering just above this important level.

Understanding 30-Year vs. 15-Year Loans

Choosing the right loan term remains one of the biggest decisions for buyers.

30-Year Fixed Mortgage:

- Lower monthly payments

- More flexibility for budgeting

- Higher total interest over time

This option is popular because it spreads payments over a longer period, making homeownership more accessible on a monthly basis.

15-Year Fixed Mortgage:

- Lower interest rate

- Faster loan payoff

- Less total interest paid

However, the trade-off is higher monthly payments, which can limit affordability for some buyers.

Adjustable-Rate Mortgages: Still an Option?

Adjustable-rate mortgages (ARMs) continue to be part of the market, though their appeal has shifted.

With an ARM:

- The rate stays fixed for an initial period (such as 5 or 7 years)

- After that, it adjusts annually based on market conditions

While ARMs traditionally start with lower rates, current data shows that fixed rates are sometimes just as competitive. This means borrowers should compare options carefully before deciding.

What’s Driving Mortgage Rates Right Now

Mortgage rates are influenced by a mix of economic and market factors, including:

- Inflation trends

- Bond market performance

- Federal Reserve policy expectations

- Global economic conditions

At the moment, these forces are balancing each other, keeping rates relatively stable without sharp movements.

How Buyers Can Navigate This Market

Even with rates holding steady, buyers can take steps to improve their position:

- Compare offers from multiple lenders

- Improve credit score before applying

- Reduce existing debt

- Save for a larger down payment

These actions can help secure better loan terms, even when overall market rates remain unchanged.

Refinancing in the Current Environment

For homeowners, refinancing decisions depend on individual circumstances.

It may make sense to refinance if:

- You can secure a lower rate than your current loan

- You want to switch to a shorter loan term

- You need to adjust monthly payments

However, with rates near 6%, many homeowners are waiting for further declines before making a move.

Short-Term Outlook for Mortgage Rates

Recent trends show that rates have eased from their late-March highs, but progress has slowed. Forecasts suggest:

- Rates may continue to move within a narrow range

- A drop below 6% is possible but not guaranteed

- Economic data in the coming weeks could influence direction

For now, the market appears to be in a holding pattern.

The Bottom Line

Mortgage rates on April 22, 2026 remain just above 6%, with shorter-term loans offering slightly lower rates. While the market has improved compared to recent highs, buyers are still waiting for a clearer drop below the 6% level.

In this environment, preparation and smart financial planning can make a big difference. Whether buying or refinancing, understanding your options is key to making the most of current market conditions. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses