Home Affordability Improves Slightly in 2026: Buyers Still Need Six-Figure Incomes

Homebuying affordability showed modest improvement during April 2026 as lower mortgage rates and rising incomes helped offset continued home-price growth. While housing remains expensive by historical standards, recent data suggests buyers are beginning to see small gains after several years of worsening affordability.

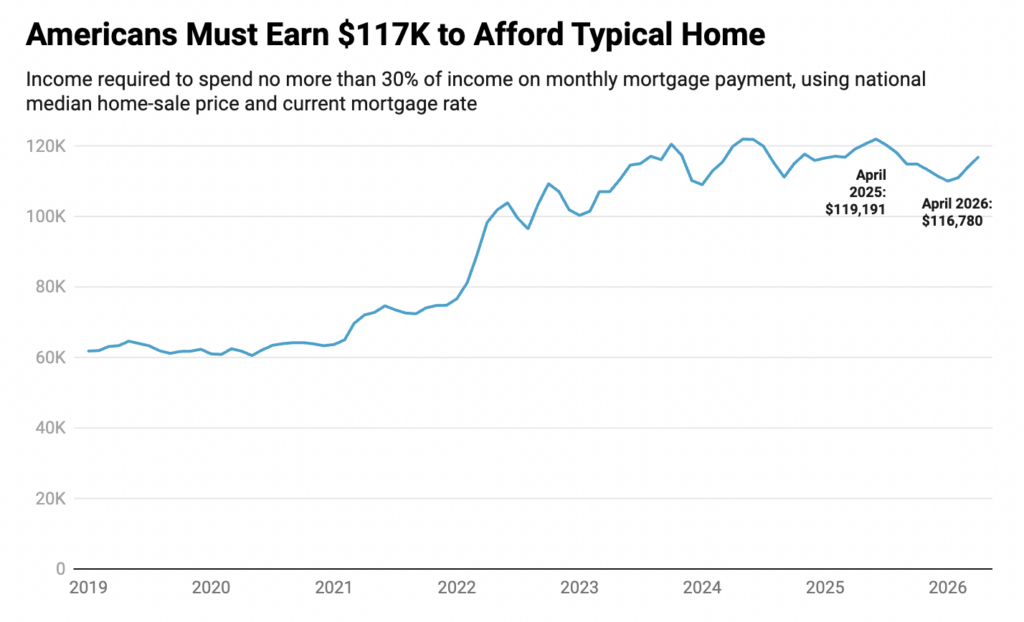

According to new research from Redfin, the annual income needed to afford the typical home for sale in the United States fell to $116,780 in April. That marks a 2% decline from the $119,191 required one year earlier and represents the seventh consecutive month of year-over-year affordability improvements.

Although the improvement is encouraging, the income needed to purchase the average home still remains significantly higher than what most American households earn.

Lower Mortgage Rates Help Ease Housing Costs

One of the biggest contributors to improving affordability was the decline in mortgage rates during April.

The average 30-year fixed mortgage rate dropped from 6.73% a year earlier to approximately 6.33% during April 2026. Lower borrowing costs reduced monthly mortgage payments and slightly improved purchasing power for buyers.

At the same time, household incomes continued growing.

Median household income reached an estimated $87,599, up roughly 4% compared to the previous year. Higher earnings combined with slightly lower financing costs helped narrow the affordability gap.

However, the improvement remains limited because home prices continue rising in many markets.

Home Prices Continue Moving Higher

While mortgage rates provided some relief, home values continued increasing across much of the country.

The median U.S. home-sale price rose 2.4% year over year during April. This ongoing appreciation prevented affordability from improving more significantly.

Additionally, mortgage rates moved higher again during May, with average weekly rates climbing back above 6.5%.

As a result, buyers entering the market now may not experience the same affordability advantages that existed in April.

Housing experts note that affordability remains far worse than before the sharp run-up in prices and mortgage rates that began during the pandemic housing boom.

Buyers Still Need More Than the Average Household Income

Despite recent progress, the affordability gap remains substantial.

The typical U.S. household earns about $88,000 annually. However, buyers need approximately $116,780 to comfortably afford the median-priced home under standard lending guidelines.

That means many households still fall well short of the income needed to purchase a typical property.

Financial experts generally recommend spending no more than 30% of gross income on housing expenses. Yet for many Americans, purchasing the median-priced home would require spending closer to 40% of household income.

Although this is an improvement from 42.4% a year earlier, affordability remains stretched for many buyers.

More Listings Are Becoming Affordable

Another positive development is the growing share of homes considered affordable for median-income households.

In April:

- 32.9% of active listings were affordable for households earning the median income.

- One year earlier, only 28.7% of listings met that standard.

The increase suggests buyers have more options than they did a year ago.

However, affordability remains well below historical norms.

Before mortgage rates surged in 2022, more than half of all home listings across the country were typically affordable for the median-income household.

Today’s affordability levels remain far below those long-term averages.

Housing Inventory Continues Helping Buyers

Buyers are also benefiting from improved inventory conditions.

Compared to previous years, many markets now have:

- More homes available for sale

- Longer listing periods

- Greater negotiating opportunities

- Reduced bidding competition

In many areas, sellers still outnumber active buyers, giving purchasers more leverage during negotiations.

These conditions have helped offset some affordability challenges, particularly for buyers willing to negotiate on price, repairs, or seller concessions.

Chicago Leads Major Markets in Affordability Improvement

Among the nation’s largest metropolitan areas, Chicago recorded the strongest affordability improvement.

In April, buyers needed an income of approximately $101,075 to afford the median-priced home in the Chicago area.

That represents a 13.3% improvement compared to one year earlier.

Other major markets showing notable affordability gains included:

- San Jose, California: income requirement down 5.6%

- Seattle, Washington: income requirement down 5.5%

These markets benefited from slower price growth, improving inventory, and more balanced buyer-seller conditions.

Several Midwest Markets Remain Affordable

A number of Midwestern markets continue offering affordability advantages compared to many coastal cities.

Metro areas where median household incomes exceed the income needed to purchase a home include:

- Baltimore

- Cincinnati

- Cleveland

- Detroit

- Indianapolis

- Minneapolis

- Pittsburgh

- St. Louis

- Warren, Michigan

These markets continue attracting attention from first-time buyers, retirees, and investors seeking lower housing costs and stronger affordability.

San Francisco Becomes Less Affordable Again

Not every market experienced improvement.

San Francisco posted the largest affordability decline among major metro areas.

Buyers now need approximately $443,979 in annual income to afford the median-priced home there, representing a 7% increase from one year earlier.

Several factors contributed to the rise:

- Strong housing demand

- Limited supply

- Growth in high-income technology jobs

- Continued investment tied to artificial intelligence expansion

Other metros experiencing worsening affordability included:

- Philadelphia

- Providence, Rhode Island

These markets continue facing inventory shortages and strong buyer demand.

Buyer Demand Is Starting to Return

Housing activity has begun increasing as affordability conditions improve modestly.

Recent data shows pending home sales rising during early May, suggesting more buyers are re-entering the market after sitting on the sidelines for much of the past two years.

Many buyers appear encouraged by:

- More available listings

- Greater negotiating power

- Stabilizing mortgage rates

- Rising wages

However, increased demand could eventually create more competition and place upward pressure on prices again.

Risks Could Slow Future Affordability Gains

While affordability has improved modestly, several risks remain.

Housing economists point to several factors that could reverse recent progress:

Potential Challenges Ahead

- Higher mortgage rates

- Additional Federal Reserve rate hikes

- Rising energy prices

- Inflation pressures

- Global geopolitical uncertainty

- Economic slowdowns

Any significant increase in borrowing costs could quickly reduce purchasing power and make homes less affordable again.

Outlook for the Rest of 2026

Most housing analysts expect affordability to improve gradually through the remainder of 2026, though gains are likely to remain modest.

Inventory growth, slowing home-price appreciation, and steady wage increases should provide some support for buyers.

At the same time, mortgage rates remain the biggest factor influencing affordability. If rates stabilize or move lower, more households could re-enter the housing market. If rates rise again, recent affordability improvements could quickly disappear.

For now, buyers are seeing better conditions than they did a year ago, but homeownership remains financially challenging for many Americans as the housing market continues adjusting to a higher-rate environment. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses