First-Time Homebuyers Are Getting Younger: New Fed Data Reveals Surprising Trend

New data suggests that first-time homebuyers are becoming slightly younger, offering an encouraging sign for the housing market despite continued affordability challenges.

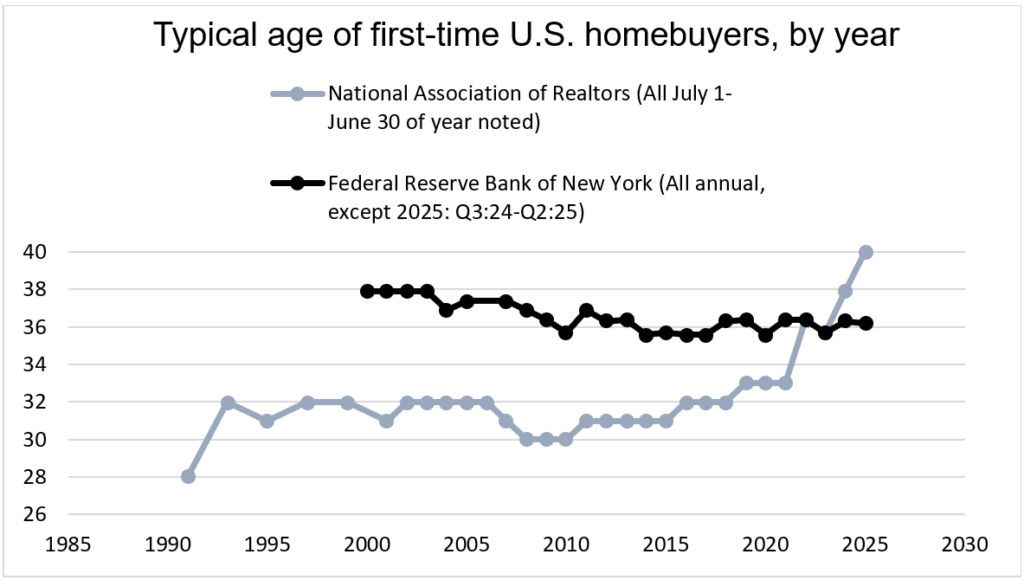

According to recent Federal Reserve research, both the median and average age of Americans purchasing their first home with a mortgage declined during the first quarter of 2026. While the changes are modest, they stand out against a backdrop of elevated home prices and mortgage rates that have made homeownership increasingly difficult for many households.

First-Time Buyer Age Moves Lower

Federal Reserve data shows:

- Median first-time homebuyer age: 33 years.

- Average first-time homebuyer age: 36.2 years.

Compared with the previous quarter:

- Median age declined from 34 to 33.

- Average age declined from 36.8 to 36.2.

The data also compares favorably with long-term historical averages. Since 2000, the median age has gradually drifted slightly lower while the average age has remained relatively stable.

Although the improvement is small, it suggests younger buyers are continuing to enter the housing market despite challenging conditions.

How the Data Is Collected

The Federal Reserve’s findings come from the New York Fed Consumer Credit Panel.

The database uses a 5% random sample of U.S. credit reports and tracks:

- Borrower age.

- Mortgage history.

- Previous homeownership activity.

A borrower is classified as a first-time homebuyer if they have never previously held a residential mortgage.

Because the data relies on mortgage records, cash purchases are not included in the analysis.

The quarterly updates provide one of the most timely measures of first-time buyer activity in the United States.

Why Other Studies Show Older Buyers

Some housing studies have suggested first-time buyers are getting significantly older.

For example, recent survey-based research estimated the average first-time buyer age at around 40 years.

The difference largely comes from methodology.

Survey-based studies may receive fewer responses from younger households, while credit-report data captures actual mortgage borrowers across a broader population.

The Federal Reserve data indicates:

- Younger buyers represent a larger share of first-time mortgage borrowers than some surveys suggest.

- Millennials and Generation Z continue participating in the housing market.

- Age trends may not be as extreme as previously believed.

Affordability Remains the Bigger Issue

While age trends offer some positive news, affordability remains the primary obstacle for first-time buyers.

Today’s buyers face a difficult combination of:

- Elevated home prices.

- Mortgage rates above recent historical norms.

- Higher insurance costs.

- Increased property taxes.

- Rising living expenses.

Many potential buyers can qualify for a mortgage but struggle to save for down payments and monthly housing costs.

The affordability challenge affects buyers across nearly every region of the country.

Home Prices and Mortgage Rates Changed the Market

The housing market experienced extraordinary changes over the past several years.

During the pandemic:

- Mortgage rates reached historic lows.

- Housing demand surged.

- Home prices accelerated rapidly.

Later, inflation prompted aggressive interest rate increases.

Mortgage rates more than doubled from pandemic lows, creating a difficult environment for first-time buyers who had to contend with:

- Higher purchase prices.

- Higher borrowing costs.

The result was a significant increase in the income needed to purchase a home.

Income Requirements Have Jumped

Housing affordability has changed dramatically.

Between 2019 and 2024:

- Income needed for a typical first-time home purchase increased by approximately 41%.

- Overall household income growth was only about 11%.

This widening gap means housing costs have risen much faster than earnings.

Many lower-income households have found it increasingly difficult to qualify for homeownership.

Even moderate-income families often need larger down payments and stronger financial profiles than in previous years.

Younger Buyers Are Finding Ways to Compete

Despite these obstacles, younger homebuyers continue finding paths into the market.

Common strategies include:

Larger Savings

Many buyers spend additional years building down payments before purchasing.

Family Assistance

Some receive financial help from parents or relatives for down payments and closing costs.

Government Loan Programs

FHA, VA, and USDA loans continue helping qualified buyers reduce upfront costs.

Flexible Location Choices

Many first-time buyers are expanding their home searches into more affordable suburban and smaller metropolitan areas.

Dual-Income Households

Combined incomes often improve purchasing power and mortgage qualification.

These strategies are helping some younger households overcome affordability barriers.

Regional Opportunities Continue to Emerge

Housing affordability varies significantly across the country.

Many Midwestern and Southern markets continue offering:

- Lower home prices.

- More inventory.

- Lower property taxes.

- Better affordability relative to local incomes.

Meanwhile, many coastal markets remain significantly more expensive for first-time buyers.

The ability to work remotely has also allowed some younger households to relocate to more affordable regions while maintaining higher-paying jobs.

What This Means for the Housing Market

The decline in first-time buyer age could signal several positive developments:

- Younger households remain engaged in homeownership.

- Mortgage availability continues supporting qualified borrowers.

- Housing demand remains healthy despite elevated rates.

- Buyers are adapting to changing market conditions.

First-time buyers are an essential component of a healthy housing market because they create demand throughout the entire housing chain.

Their continued participation supports broader market stability.

What Buyers Should Focus On

Rather than trying to perfectly time the housing market, prospective first-time buyers can strengthen their position by focusing on financial preparation.

Important steps include:

- Building credit scores.

- Reducing debt.

- Saving for down payments.

- Shopping among multiple lenders.

- Exploring first-time buyer assistance programs.

- Maintaining realistic expectations regarding home size and location.

Strong financial preparation can often have a greater impact than waiting for significant market changes.

Bottom Line

New Federal Reserve data suggests first-time homebuyers became slightly younger during early 2026, with the median buyer age falling to 33 years. While the change is modest, it demonstrates that younger households continue finding ways to enter the housing market despite elevated home prices and mortgage rates.

The larger challenge remains affordability rather than age. Higher borrowing costs and rapidly rising home prices have increased the income required to purchase a home, making ownership more difficult for many Americans. Even so, younger buyers continue adapting through careful financial planning, government-backed loan programs, and expanding their search into more affordable markets.

The latest data offers a reminder that while housing conditions remain challenging, the dream of homeownership continues to attract a new generation of buyers. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses