Homebuyer Affordability Slips in April: Median Mortgage Payment Climbs to $2,152

Housing affordability took a small step backward in April as rising mortgage rates and larger loan amounts pushed monthly home purchase payments higher.

According to the Mortgage Bankers Association’s Purchase Applications Payment Index (PAPI), the national median mortgage payment for homebuyers increased to $2,152 in April, up from $2,131 in March. While affordability remains better than it was one year ago, the latest data shows that housing costs continue to challenge many prospective buyers.

The report measures changes in mortgage payments relative to household income and serves as one of the industry’s key affordability indicators.

Mortgage Payments Move Higher

The national median mortgage payment increased by $21 month over month, reaching $2,152 in April.

Although the increase was relatively modest, it reflects the combined effect of slightly higher mortgage rates and larger average loan amounts during the month.

Compared to April 2025, however, the median payment was still down by $35, representing a 1.6% annual decline.

This suggests that affordability conditions remain somewhat improved from last year despite recent monthly pressure.

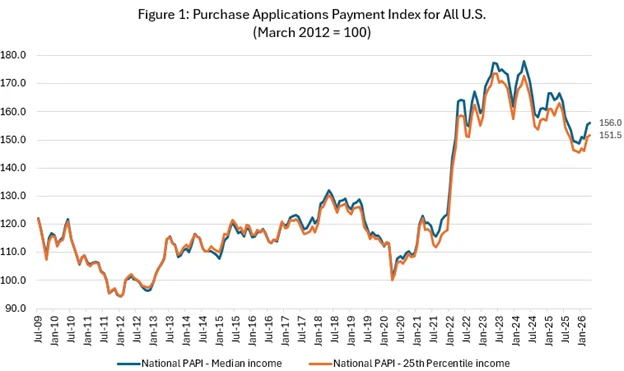

Affordability Index Shows Slight Deterioration

The Purchase Applications Payment Index rose from 155.5 in March to 156.0 in April.

A higher PAPI reading indicates worsening affordability because mortgage payments consume a larger share of household income.

When mortgage rates increase, loan sizes grow, or incomes fail to keep pace with housing costs, affordability declines. Conversely, lower mortgage rates and rising incomes help improve affordability.

The 0.3% monthly increase signals a modest deterioration rather than a significant affordability shock.

Income Growth Continues to Help Buyers

One of the reasons affordability has not deteriorated more sharply is continued wage growth.

Household incomes increased approximately 4% compared with one year earlier, helping offset higher housing expenses.

As a result, the affordability index remains 5.3% lower than a year ago, indicating that overall affordability conditions are still better than they were during the same period in 2025.

Income growth has become an important support factor for buyers navigating elevated home prices and mortgage rates.

FHA and Conventional Borrowers See Higher Payments

Monthly payments increased across major loan categories.

For FHA borrowers, the median mortgage payment rose from $1,812 in March to $1,829 in April. However, that figure remains below the $1,895 recorded one year earlier.

Conventional loan applicants experienced a similar trend. Their median payment increased from $2,145 in March to $2,166 in April, though it remained lower than the $2,206 recorded in April 2025.

The data suggests affordability remains under pressure but has improved compared with conditions seen during last year’s higher-rate environment.

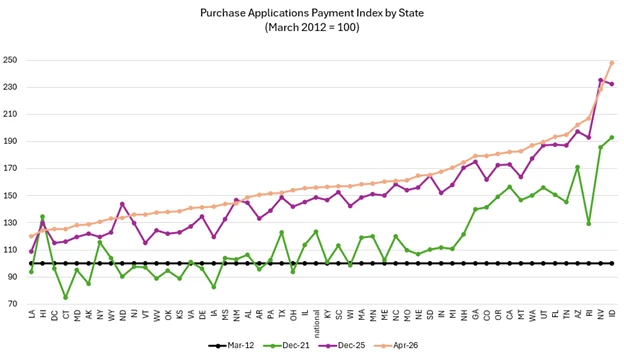

States Facing the Greatest Affordability Challenges

Housing affordability varies significantly across the country.

States with the highest affordability pressures according to the PAPI included:

- Idaho (248.1)

- Nevada (228.4)

- Rhode Island (206.9)

- Arizona (202.2)

- Tennessee (194.8)

These markets continue to face challenges due to elevated home prices relative to local incomes.

Rapid home value appreciation during recent years has left many buyers struggling to keep pace despite moderating mortgage rates.

States Showing Better Affordability Conditions

Several states continue to offer relatively stronger affordability compared with the national average.

Among the lowest PAPI readings were:

- New York (116.7)

- Louisiana (120.1)

- Hawaii (124.4)

- District of Columbia (125.2)

- Connecticut (125.2)

- Maryland (128.4)

These lower readings suggest mortgage payments consume a smaller percentage of household income in these locations compared with higher-cost affordability markets.

Affordability Challenges Across Demographic Groups

The report also examined affordability trends among different household groups.

Affordability weakened slightly for all major groups in April:

- Black households: PAPI increased from 161.0 to 161.5

- Hispanic households: PAPI increased from 143.9 to 144.3

- White households: PAPI increased from 156.8 to 157.3

While the increases were small, they reflect the broader affordability pressures affecting buyers nationwide.

Mortgage Payments Compared With Rent

The MBA also tracks the relationship between homeownership costs and rental costs through its Mortgage Payment-to-Rent Ratio.

The ratio declined from 1.38 during the fourth quarter of 2025 to 1.35 during the first quarter of 2026.

This indicates that mortgage payments became slightly more affordable relative to rents.

Meanwhile, the national median asking rent increased to $1,579 during the first quarter of 2026, up from $1,464 in the previous quarter.

Although buying a home remains more expensive than renting in many markets, the gap narrowed slightly during the first quarter.

New Home Market Shows Slight Improvement

The Builders’ Purchase Application Payment Index also reflected modest affordability improvement in the new-home market.

The median mortgage payment for newly built homes decreased from $2,210 in March to $2,188 in April.

Builders continue using incentives, price adjustments, and financing programs to attract buyers in an environment where affordability remains a key challenge.

Outlook for Homebuyer Affordability

The housing market continues to balance competing forces.

Mortgage rates remain significantly lower than the peaks seen during recent years, and wage growth continues supporting purchasing power. However, elevated home prices and occasional rate increases continue limiting affordability gains.

Many housing economists expect affordability to improve gradually throughout the remainder of 2026 if mortgage rates remain stable and household incomes continue rising.

While April’s report showed a slight setback, the broader trend still points toward modest improvement compared with the affordability conditions buyers faced over the past two years.

For prospective buyers, affordability remains challenging but is generally moving in a more favorable direction than it was a year ago. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses