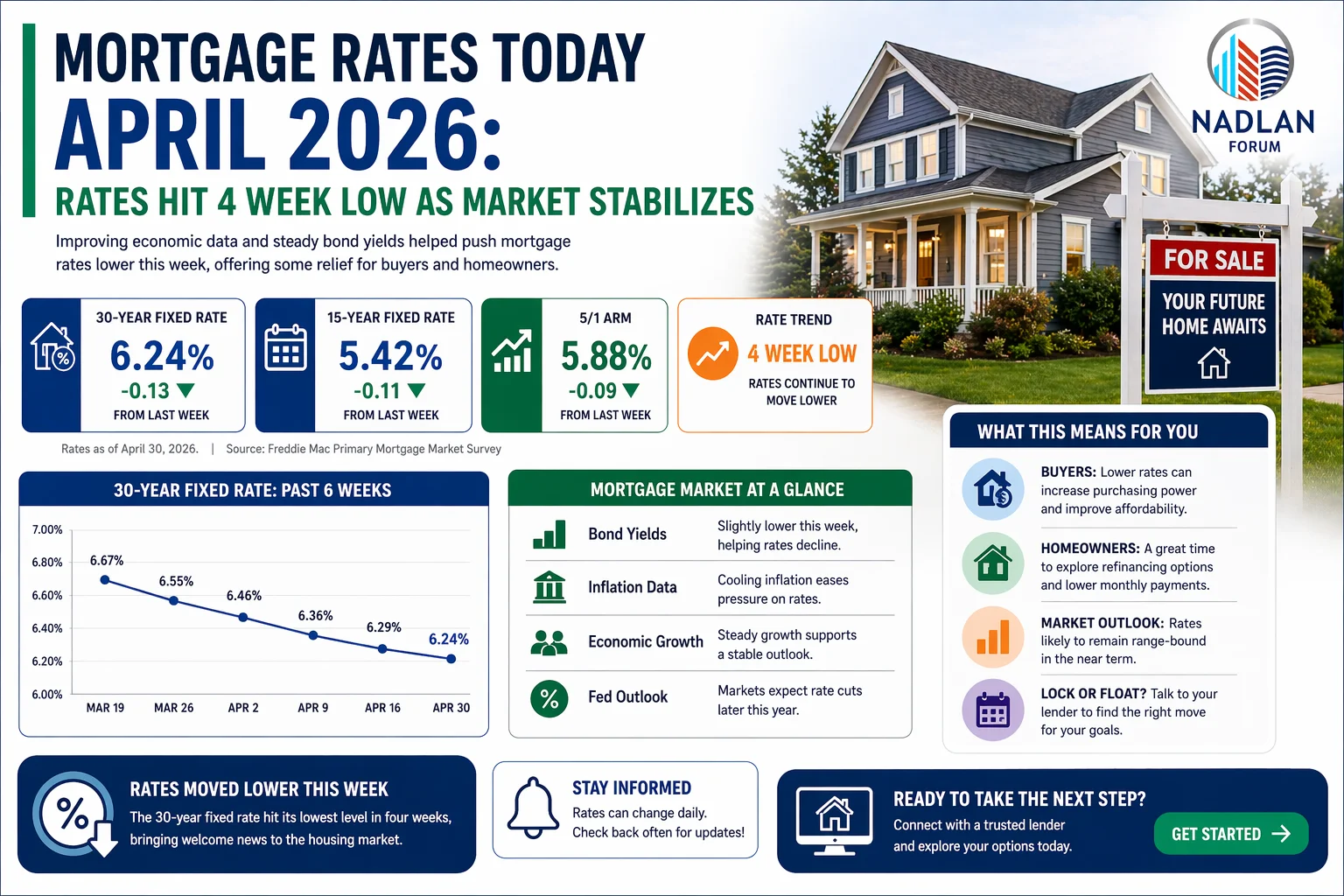

Mortgage Rates Today: Home Loan and Refinance Rates Mostly Move Lower on June 10, 2026

Mortgage rates moved mostly lower on June 10, offering a bit of relief for homebuyers and homeowners after several days of upward pressure. While the popular 30-year fixed mortgage and several adjustable-rate products declined, the 15-year fixed mortgage moved slightly higher.

The latest changes come as financial markets continue to digest recent inflation data, economic reports, and expectations for future Federal Reserve policy. Although borrowing costs remain elevated compared with the lows seen during the pandemic, today’s rates remain within the range many economists expected for 2026.

For buyers entering the market and homeowners considering refinancing, understanding today’s mortgage trends can help with choosing the right loan strategy.

Mortgage Rates Today

According to the latest national averages, mortgage rates for home purchases are:

30-year fixed: 6.33%

20-year fixed: 6.26%

15-year fixed: 5.89%

5/1 ARM: 6.54%

7/1 ARM: 6.54%

30-year VA: 5.80%

15-year VA: 5.50%

5/1 VA: 5.69%

Compared with the previous day:

- 30-year fixed fell by 8 basis points.

- 20-year fixed dropped by 14 basis points.

- 15-year fixed increased by 8 basis points.

- Adjustable-rate products generally moved lower.

The decline in longer-term rates may help improve affordability for some buyers entering the housing market.

Current Refinance Rates

Homeowners considering refinancing should also monitor today’s averages.

Current refinance rates include:

30-year fixed: 6.46%

20-year fixed: 6.44%

15-year fixed: 5.91%

5/1 ARM: 6.51%

7/1 ARM: 6.43%

30-year VA: 5.94%

15-year VA: 5.39%

5/1 VA: 5.83%

Refinancing rates are often slightly higher than purchase mortgage rates, although market conditions can occasionally reverse that relationship.

For homeowners with older high-interest loans, refinancing may still provide long-term savings depending on individual circumstances.

Why Mortgage Rates Changed

Mortgage rates do not move independently. They respond to several economic factors.

Key influences include:

- Inflation data.

- Treasury bond yields.

- Federal Reserve policy expectations.

- Employment reports.

- Global economic events.

- Investor demand for mortgage-backed securities.

Recent inflation reports showed price pressures remain above the Federal Reserve’s target, but softer underlying inflation helped calm financial markets, allowing some mortgage rates to move lower.

Daily fluctuations are common and may continue as investors evaluate new economic data.

What Lower Rates Mean for Buyers

Even small changes in mortgage rates can affect affordability.

A lower interest rate can reduce:

- Monthly mortgage payments.

- Total interest paid over the life of the loan.

- Debt-to-income ratios.

- The amount of income needed to qualify.

For buyers shopping for homes, today’s modest decline could improve purchasing power compared with earlier in the week.

However, affordability remains challenging because home prices and borrowing costs are still historically elevated.

30-Year Fixed Mortgage

The 30-year fixed mortgage remains the most popular loan option for American homebuyers.

Benefits

- Lower monthly payments.

- Predictable payment schedule.

- Protection from future rate increases.

- Easier budgeting.

Drawbacks

- Higher interest rate than shorter-term loans.

- More interest paid over time.

- Longer repayment period.

Many buyers choose this option because it offers financial flexibility while keeping monthly housing costs manageable.

15-Year Fixed Mortgage

The 15-year fixed mortgage offers a different balance between cost and affordability.

Advantages

- Lower long-term interest costs.

- Faster equity building.

- Mortgage paid off in half the time.

- Lower total borrowing expense.

Disadvantages

- Higher monthly payments.

- Smaller margin for unexpected financial changes.

The slight increase in today’s 15-year rate may not significantly affect borrowers focused on long-term interest savings.

Adjustable-Rate Mortgages

Adjustable-rate mortgages, or ARMs, continue to attract certain borrowers.

A 5/1 ARM or 7/1 ARM keeps the interest rate fixed for an initial period before adjusting periodically.

ARMs may work well for borrowers who:

- Plan to move within several years.

- Expect future income growth.

- Anticipate refinancing before adjustments begin.

However, future interest rate increases remain a potential risk.

Current market conditions have narrowed the pricing advantage between adjustable and fixed-rate mortgages, making careful comparison important.

Should You Buy or Refinance Now?

The answer depends on personal financial goals rather than daily market movements alone.

Buying may make sense if:

- You have stable income.

- You plan to stay in the home for several years.

- You find a property that fits your budget.

Refinancing may be worth considering if:

- You can lower your interest rate.

- You want to reduce monthly payments.

- You want to shorten your loan term.

- You plan to convert an adjustable loan into a fixed rate.

Waiting for significantly lower rates carries some uncertainty because future mortgage movements depend on inflation, Federal Reserve policy, and broader economic conditions.

Tips for Getting a Better Mortgage Rate

Borrowers can improve their chances of securing a competitive mortgage by:

Improve Your Credit Score

Higher credit scores generally qualify for better rates.

Reduce Existing Debt

Lower debt-to-income ratios improve loan eligibility.

Save for a Larger Down Payment

A larger down payment may reduce lender risk and improve pricing.

Compare Multiple Lenders

Obtaining several quotes often results in better loan terms.

Consider Discount Points

Paying points upfront can reduce the interest rate over the life of the loan.

Lock Your Rate

If you find a favorable rate, locking it can protect against market volatility.

What Could Happen Next?

Mortgage rates are likely to remain sensitive to upcoming economic reports and Federal Reserve decisions.

Key developments to watch include:

- Inflation reports.

- Employment data.

- Federal Reserve meetings.

- Treasury market movements.

- Consumer spending trends.

Many housing economists expect mortgage rates to remain in the mid-6% range through much of 2026, though short-term fluctuations are likely.

Bottom Line

Mortgage rates on June 10, 2026, moved mostly lower, providing some welcome relief for homebuyers after recent increases. The average 30-year fixed mortgage fell to 6.33%, while several refinance and adjustable-rate products also declined. The 15-year fixed mortgage was the main exception, posting a modest increase.

Although borrowing costs remain above the historically low levels seen in previous years, today’s rates continue to support steady housing activity. For buyers and homeowners alike, focusing on personal finances, comparing multiple lenders, and understanding available loan options may have a greater impact than trying to perfectly time daily market movements. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses