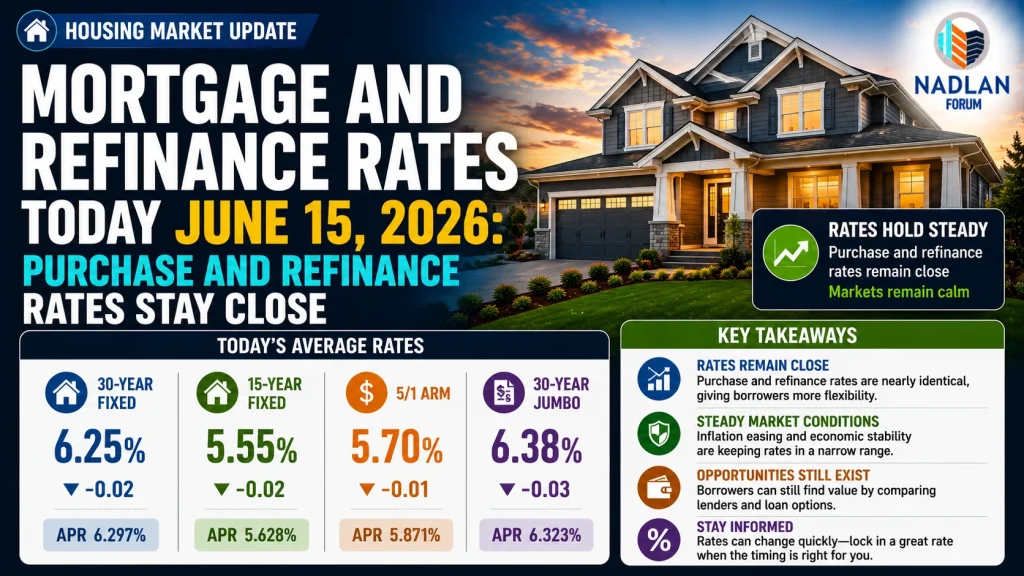

Mortgage Rates Today: Home Loan and Refinance Rates Move Higher on June 9, 2026

Mortgage rates moved higher on June 9, giving homebuyers and homeowners another reminder that borrowing costs remain unpredictable in today’s housing market. According to the latest national data, fixed mortgage rates increased while adjustable-rate mortgages experienced some of the biggest daily jumps.

Although the changes were relatively modest for most fixed-rate loans, the continued movement higher adds another challenge for buyers already dealing with elevated home prices and affordability concerns.

For homeowners considering refinancing, rates remain close to purchase loan rates, creating opportunities for some borrowers while making others wait for better market conditions.

Today’s Mortgage Rates

According to the latest national averages, mortgage rates increased across most major loan products.

Current purchase mortgage rates include:

- 30-year fixed: 6.41%

- 20-year fixed: 6.40%

- 15-year fixed: 5.81%

- 5/1 ARM: 6.66%

- 7/1 ARM: 6.74%

- 30-year VA: 5.96%

- 15-year VA: 5.51%

- 5/1 VA: 5.71%

The average 30-year fixed mortgage increased by three basis points from the previous day, while the average 15-year mortgage rose seven basis points.

Adjustable-rate mortgages saw some of the largest increases, with the 5/1 ARM climbing by 34 basis points.

Refinance Rates Remain Close to Purchase Rates

Homeowners considering refinancing may notice that refinance rates remain very similar to purchase mortgage rates.

Current refinance averages are:

- 30-year fixed: 6.38%

- 20-year fixed: 6.44%

- 15-year fixed: 5.80%

- 5/1 ARM: 6.38%

- 7/1 ARM: 6.01%

- 30-year VA: 5.86%

- 15-year VA: 5.37%

- 5/1 VA: 5.64%

In some loan categories, refinance rates are actually slightly lower than purchase rates.

Whether refinancing makes financial sense depends on the homeowner’s current mortgage, remaining loan balance, and long-term plans.

Why Mortgage Rates Continue to Move

Mortgage rates are influenced by several economic factors.

Some of the biggest drivers include:

Inflation

Higher inflation often pushes mortgage rates upward because investors demand higher returns.

Federal Reserve Policy

Although the Federal Reserve does not directly set mortgage rates, its interest rate decisions influence borrowing costs throughout the economy.

Treasury Yields

Mortgage rates generally move alongside longer-term Treasury bond yields.

Economic Data

Employment reports, consumer spending, inflation readings, and economic growth all affect investor expectations and mortgage pricing.

Recent economic reports have created uncertainty about future interest rate policy, contributing to ongoing market volatility.

Comparing a 30-Year and 15-Year Mortgage

Many buyers continue to debate whether a shorter mortgage term makes financial sense.

30-Year Fixed Mortgage

Advantages include:

- Lower monthly payments.

- More financial flexibility.

- Easier qualification for many borrowers.

- Extra cash available for savings or investments.

The main drawback is paying significantly more interest over the life of the loan.

15-Year Fixed Mortgage

Benefits include:

- Lower interest rates.

- Faster loan payoff.

- Significant long-term interest savings.

- Faster equity growth.

The trade-off is a much higher monthly payment.

For many buyers, the decision depends on balancing monthly affordability with long-term financial goals.

Adjustable-Rate Mortgages Require Careful Planning

Adjustable-rate mortgages, commonly called ARMs, have become more complicated in today’s market.

With a typical ARM:

- The interest rate stays fixed for an initial period.

- The rate adjusts periodically afterward.

- Monthly payments can increase or decrease depending on market conditions.

Historically, ARMs often started with lower interest rates than fixed loans.

Recently, however, some ARM products have offered rates similar to or even higher than fixed mortgages.

Borrowers considering an ARM should understand how future rate adjustments could affect their payments.

How Rising Rates Affect Homebuyers

Even small increases in mortgage rates can significantly affect affordability.

Higher rates generally mean:

- Larger monthly payments.

- Reduced purchasing power.

- Smaller loan approvals.

- Increased interest costs over time.

For example, a difference of only a few tenths of a percentage point can add thousands of dollars to the total cost of a mortgage over 30 years.

Many buyers are adjusting their home search budgets to account for higher financing costs.

Tips for Getting a Better Mortgage Rate

While national averages provide a market snapshot, individual borrowers can often improve the rate they receive.

Some common strategies include:

Improve Credit Scores

Higher credit scores typically qualify for better interest rates.

Reduce Debt

Lower debt-to-income ratios can improve loan terms.

Increase the Down Payment

Larger down payments reduce lender risk.

Compare Multiple Lenders

Shopping around often leads to better offers.

Consider Discount Points

Paying points upfront may reduce the long-term interest rate.

Comparing several loan estimates remains one of the most effective ways to lower borrowing costs.

What Experts Expect for Mortgage Rates

Housing economists continue to expect mortgage rates to remain relatively stable through the remainder of 2026.

Current industry forecasts suggest:

- Some analysts expect average 30-year rates near 6.5%.

- Others anticipate rates closer to 6.3%.

- Large declines are not widely expected in the near future.

Future inflation reports, labor market data, and Federal Reserve decisions will continue influencing mortgage markets.

Is Now a Good Time to Buy or Refinance?

The answer depends more on personal circumstances than daily rate movements.

For buyers, purchasing a home when finances are stable and the right property becomes available often matters more than trying to perfectly time the market.

For homeowners considering refinancing, the decision depends on:

- Current mortgage rate.

- Remaining loan term.

- Closing costs.

- Expected time in the home.

- Monthly payment goals.

Running the numbers carefully can help determine whether refinancing provides meaningful savings.

Bottom Line

Mortgage rates moved higher on June 9, with the average 30-year fixed mortgage reaching 6.41% and several adjustable-rate products posting larger increases. Refinance rates remain close to purchase loan rates, offering opportunities for some homeowners while keeping affordability challenges in focus.

Although borrowing costs remain elevated compared with recent years, buyers and homeowners still have ways to improve their financing options through strong credit, larger down payments, and careful comparison shopping. As inflation, Federal Reserve policy, and economic data continue shaping financial markets, mortgage rates are likely to remain dynamic throughout the rest of 2026. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses