Mortgage Rates Today: 30- and 15-Year Rates Move Lower on June 16, 2026

U.S. mortgage rates showed mixed movement on Tuesday, June 16, 2026, as key loan products shifted in different directions. According to Zillow lender marketplace data, long-term fixed rates slightly declined, while some shorter-term and adjustable-rate products posted small increases.

The latest changes highlight an ongoing pattern of small daily fluctuations in the mortgage market as lenders adjust pricing based on economic conditions and bond market activity.

Today’s Mortgage Rates

Mortgage rates across major loan types remained relatively stable overall, with only minor shifts compared to the previous day.

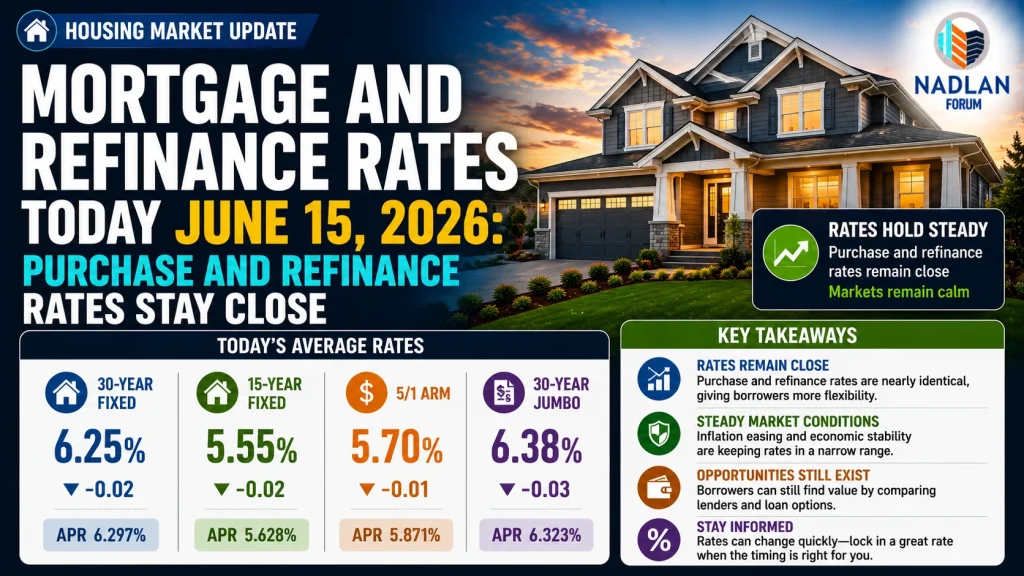

- 30-year fixed: 6.31% (down 4 basis points)

- 20-year fixed: 6.19% (up 9 basis points)

- 15-year fixed: 5.74% (down 4 basis points)

- 5/1 ARM: 6.31% (up 1 basis point)

- 7/1 ARM: 6.32%

- 30-year VA: 5.88%

- 15-year VA: 5.39%

- 5/1 VA: 5.72%

These figures represent national averages and may vary depending on borrower credit profiles, down payments, and lender pricing.

Mortgage Refinance Rates Today

Refinance rates followed a similar mixed pattern, with slight adjustments across loan categories.

- 30-year fixed refinance: 6.34%

- 20-year fixed refinance: 6.11%

- 15-year fixed refinance: 5.82%

- 5/1 ARM refinance: 6.25%

- 7/1 ARM refinance: 6.35%

- 30-year VA refinance: 5.79%

- 15-year VA refinance: 5.33%

- 5/1 VA refinance: 5.60%

In general, refinance rates remain slightly higher than purchase rates, reflecting added lender risk and market pricing adjustments.

What’s Driving Today’s Mortgage Rate Movement

Mortgage rates continue to respond to broader economic signals, including inflation expectations, bond yields, and Federal Reserve policy outlooks.

Even small daily changes, such as a few basis points, reflect shifting investor sentiment in the bond market, which directly influences mortgage pricing.

Fixed-rate loans like the 30-year and 15-year mortgages tend to move together, while adjustable-rate products can react differently depending on short-term rate expectations.

30-Year vs 15-Year Mortgage Costs

The difference between long-term and short-term mortgages remains significant for borrowers.

A typical comparison shows:

- A $400,000 30-year mortgage at 6.19% results in about $2,447 monthly principal and interest, with more than $480,000 in total interest paid over the life of the loan.

- A $400,000 15-year mortgage at 5.65% increases monthly payments to about $3,300, but reduces total interest to roughly $194,000.

While 15-year loans cost more monthly, they significantly reduce long-term interest expenses and help borrowers build equity faster.

Fixed vs Adjustable-Rate Mortgages

Fixed-rate mortgages maintain the same interest rate for the entire loan term, offering predictable monthly payments. Borrowers only see changes if they refinance later.

Adjustable-rate mortgages (ARMs), such as 5/1 or 7/1 loans, typically offer a fixed rate for an initial period before adjusting annually based on market conditions.

Although ARMs sometimes start with lower rates, recent market conditions have reduced that advantage, making fixed-rate loans more appealing for many borrowers.

Mortgage Rate Outlook

Market forecasts suggest mortgage rates may remain relatively stable through 2026.

- Some projections place the 30-year mortgage rate near 6.4%–6.5% for the year.

- Longer-term outlooks suggest only modest changes into 2027.

This indicates that borrowers should expect continued rate fluctuations within a narrow range rather than sharp declines or spikes.

Conclusion

Mortgage rates on June 16, 2026, reflect a mixed but stable environment. While 30-year and 15-year fixed rates saw slight declines, other loan categories moved higher or remained flat.

For buyers and homeowners, today’s market continues to emphasize timing flexibility, lender comparison, and long-term financial planning over short-term rate swings. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses