Why the U.S. Housing Crisis Continues: Affordability Remains Out of Reach in 2026

Why the U.S. Housing Crisis Continues in 2026

The U.S. housing market is beginning to show signs of balance after years of rapid price growth, intense competition, and limited inventory. More homes and apartments are becoming available, construction remains above pre-pandemic levels in many markets, and population growth has slowed compared to previous years.

Despite these changes, millions of Americans continue to face serious housing affordability challenges.

The latest State of the Nation’s Housing report from the Harvard Joint Center for Housing Studies (JCHS) shows that the country’s biggest housing problem is no longer simply a shortage of homes. Instead, the issue has shifted toward a lack of homes that average workers and middle-income families can actually afford.

Although the housing market is improving in some areas, affordability remains one of the largest financial challenges facing both buyers and renters in 2026.

A More Balanced Market Does Not Mean Affordable Housing

During the housing boom of the early 2020s, demand dramatically outpaced supply. Buyers competed aggressively for limited inventory, pushing home prices to record highs.

Today, the situation looks different.

Builders have completed thousands of new homes and apartment units over the past few years, while slower population growth has reduced overall housing demand. In many cities, bidding wars have eased, inventory has increased, and sellers are offering more concessions.

Housing experts say the market is moving toward a healthier balance.

However, balance does not automatically translate into affordability.

Many newly built homes remain priced well above what first-time buyers or middle-income households can comfortably afford. Mortgage rates also remain elevated compared with the ultra-low levels seen during the pandemic, keeping monthly housing costs historically high.

As a result, many households remain priced out even as supply improves.

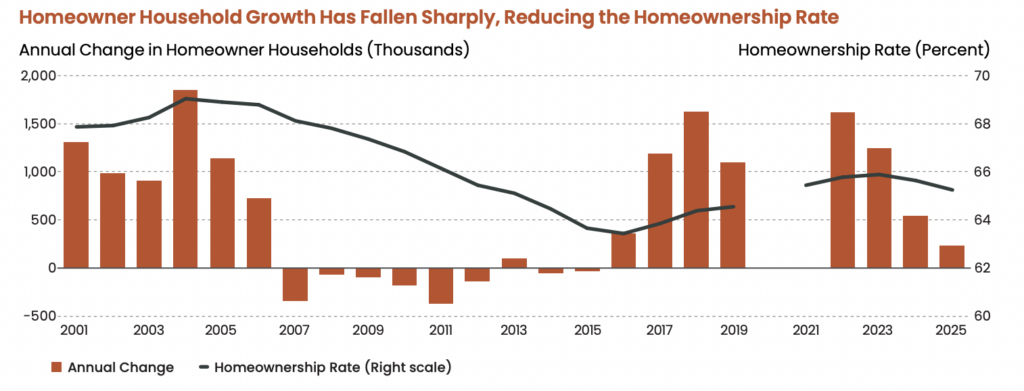

Slower Population Growth Has Changed the Market

One of the biggest shifts affecting housing demand is slower population growth.

Lower birth rates, reduced immigration, and changing household formation patterns have all contributed to weaker demand compared with previous years.

According to Harvard researchers, household formation remained slightly above one million in 2025, marking the fourth consecutive year at historically modest levels and the lowest pace since 2017.

Young adults are delaying homeownership for several reasons, including:

- Higher mortgage rates

- Rising home prices

- Student loan obligations

- Increased living expenses

- Difficulty saving for down payments

At the same time, many existing homeowners are choosing not to move because replacing their current low mortgage rate with today’s higher borrowing costs would significantly increase monthly payments.

This “lock-in effect” continues to reduce activity in the existing home market.

Affordability Is Still the Biggest Challenge

While supply has improved in some regions, housing costs remain well above income growth.

For many Americans, monthly mortgage payments, insurance premiums, property taxes, maintenance expenses, and utility costs continue to consume a growing share of household income.

Renters face similar pressures.

More than half of renter households are now considered cost-burdened, meaning they spend over 30% of their income on housing. Financial pressure has also spread beyond lower-income families.

Middle-income households earning roughly $45,000 to $75,000 annually are experiencing some of the fastest increases in housing cost burdens, leaving many families with less money for savings, healthcare, education, and everyday expenses.

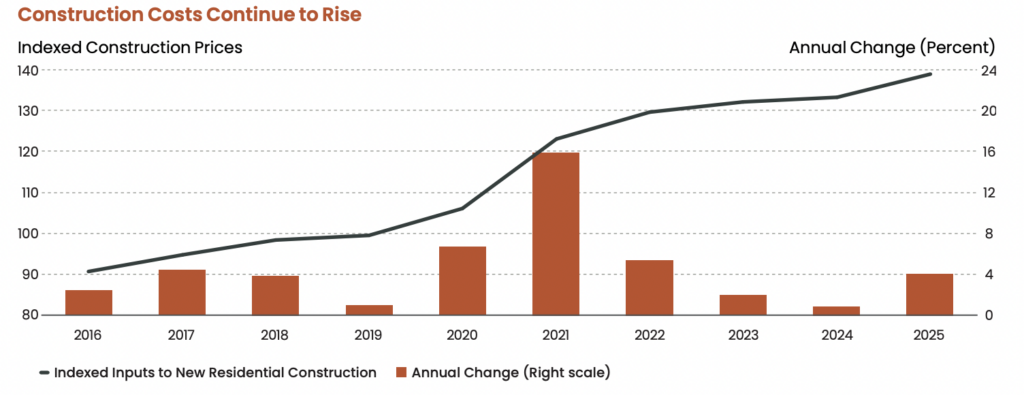

New Construction Is Concentrated in Higher Price Segments

Construction activity has remained relatively strong, but much of the new supply is concentrated in higher-priced housing.

Luxury apartments and upscale homes continue to dominate new developments because they offer stronger financial returns for builders.

Meanwhile, affordable apartments, entry-level homes, and workforce housing remain in short supply.

This mismatch creates two very different housing markets.

Higher-income households benefit from more choices, increased incentives, and slower rent growth, while lower- and middle-income households continue competing for a limited supply of affordable housing.

Housing experts increasingly argue that the conversation should shift from simply building more homes to building homes that match the budgets of everyday Americans.

Rental Supply Is Improving, but Affordability Gaps Remain

Apartment construction accelerated significantly during the pandemic, leading to a noticeable increase in rental inventory across many metropolitan areas.

As more units entered the market, rental vacancy rates climbed from roughly 6% in 2021 to above 8% in many areas.

The additional supply has helped moderate rent growth in some cities, and rental shortages are expected to ease further over the next decade.

However, many of the new apartments are luxury developments with rents beyond the reach of moderate-income households.

Affordable rental housing continues to face significant shortages, leaving millions of renters with limited options.

Housing advocates estimate the nation still lacks millions of affordable rental units for low-income households.

Home Prices Are Adjusting in Some Markets

Some regional housing markets are beginning to experience modest price reductions as builders compete for buyers.

Developers are increasingly offering incentives such as:

- Mortgage rate buydowns

- Closing cost assistance

- Price reductions

- Free upgrades

- Flexible financing options

These incentives have improved affordability for some buyers, but they have not been enough to offset the combined impact of elevated mortgage rates and years of rapid home price appreciation.

Many first-time buyers still struggle to qualify for financing or accumulate sufficient savings for a down payment.

Affordable Housing Developers Face Financial Challenges

The affordability problem extends beyond private homebuilders.

Organizations that specialize in developing affordable housing continue to face rising construction costs, expensive financing, labor shortages, and higher insurance expenses.

These financial pressures have made affordable housing projects increasingly difficult to complete without additional government assistance or public-private partnerships.

Industry leaders note that while demand for affordable housing continues to grow, current development costs often make these projects financially unworkable without subsidies or tax incentives.

As a result, many planned affordable housing developments remain delayed or financially uncertain.

Local Governments Are Testing New Housing Solutions

Cities and states are beginning to introduce policies aimed at expanding affordable housing options.

Many communities are revising zoning regulations to allow greater housing density and encourage more diverse housing types.

Several initiatives now focus on:

- Expanding accessory dwelling units (ADUs)

- Encouraging manufactured and factory-built housing

- Allowing more multifamily housing in commercial areas

- Simplifying local zoning regulations

- Reducing permitting delays

- Supporting smaller starter-home developments

These efforts are designed to increase housing supply while lowering construction costs over the long term.

Although results will take time, policymakers increasingly recognize that affordability requires more targeted solutions than simply increasing overall housing production.

The Housing Market Needs More Than Additional Supply

Housing experts agree that solving today’s affordability crisis requires a broader strategy than simply building more homes.

Future progress will likely depend on combining several approaches, including expanding affordable rental housing, increasing the supply of entry-level homes, modernizing zoning laws, reducing development costs, preserving existing affordable housing, and encouraging greater public and private investment.

The market appears to be moving toward greater stability after several years of volatility. However, stability alone will not solve the affordability crisis.

Until housing becomes more accessible across a wider range of income levels, millions of Americans will continue to struggle with buying a home, finding affordable rent, or building long-term financial security through homeownership.

Final Thoughts

The U.S. housing market in 2026 is no longer defined by extreme shortages alone. Instead, it faces a more complex challenge: ensuring that new housing meets the financial realities of working families.

Inventory is improving, builders are becoming more active, and competition has eased in many markets. Yet affordability remains the biggest obstacle for buyers and renters alike.

Addressing the housing crisis will require continued investment, smarter housing policies, and a stronger focus on producing homes at price points that ordinary Americans can afford. Until that happens, the nation’s housing challenges are likely to remain a defining issue for years to come. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses