Mortgage Rates Stay Elevated: Why They Remain Below Recent Highs Despite Market Volatility

Mortgage rates moved modestly higher during the first week of July, but the increase had less to do with major economic news and more to do with unusual activity in the financial markets. While borrowers experienced higher financing costs compared with the previous week, mortgage rates remain below the peaks reached earlier this spring.

The latest market movements highlight how closely mortgage rates are tied to the bond market. Even when there is no major economic announcement, trading activity among large institutional investors can create short-term volatility that quickly affects home loan pricing.

Fortunately for homebuyers, a weaker-than-expected U.S. employment report later in the week helped reverse part of the earlier increase, preventing mortgage rates from climbing back to their recent highs.

Bond Market Volatility Drove Mortgage Rates Higher

Mortgage rates are heavily influenced by the performance of the bond market, particularly U.S. Treasury securities and mortgage-backed securities.

During the final days of the second quarter, financial markets experienced an unusually large amount of trading activity as institutional investors adjusted portfolios before quarter-end.

Large investment firms, pension funds, insurance companies, and asset managers often rebalance billions of dollars in investments at the end of each quarter.

These transactions can temporarily create significant swings in bond prices, even without major economic news.

Because mortgage rates closely follow bond market movements, borrowers often see loan pricing change rapidly during periods of heightened market volatility.

Quarter-End Trading Created Temporary Market Pressure

Quarter-end is traditionally one of the busiest periods for financial markets.

As investment managers finalize portfolio allocations, settle large transactions, and rebalance assets, bond prices can fluctuate sharply over a very short period.

This wave of trading pushed bond prices lower early in the week.

Since bond prices and bond yields move in opposite directions, yields increased, placing upward pressure on mortgage rates.

The result was a noticeable increase in mortgage pricing despite the absence of any major changes in the broader economic outlook.

Mortgage Rates Jumped Early in the Week

Mortgage lenders reacted quickly to the changing bond market.

Average 30-year fixed mortgage rates increased approximately 0.125 percentage points during the middle of the week before stabilizing.

Some lenders implemented pricing changes immediately, while others adjusted rates more gradually depending on when trading volatility occurred during the day.

As a result, borrowers shopping for mortgages may have noticed meaningful pricing differences between lenders throughout the week.

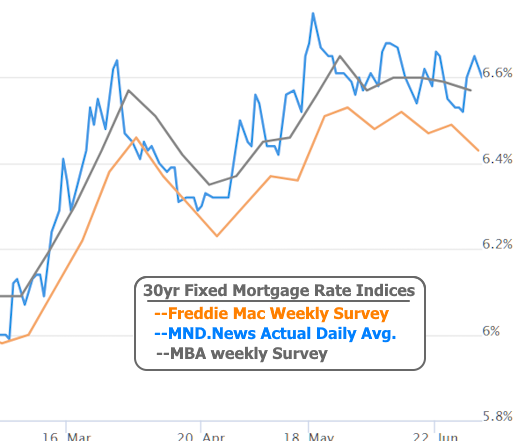

Although the increase was significant over just a few days, rates remained below the levels experienced during mid-May and early June, providing some reassurance for prospective homebuyers.

June Jobs Report Helped Improve Mortgage Rates

Later in the week, financial markets received new economic data that shifted investor expectations.

The June employment report showed the U.S. economy added only 57,000 jobs, substantially below economists’ expectations.

Slower job creation generally suggests economic growth is cooling.

For bond investors, weaker labor market data often increases demand for bonds because it reduces expectations that the Federal Reserve will need to tighten monetary policy aggressively.

As investors purchased more bonds following the report, bond yields declined.

Lower yields helped mortgage rates recover nearly half of the increases recorded earlier in the week.

Why Weak Employment Data Can Lower Mortgage Rates

Although slower hiring may be concerning for the overall economy, it often benefits mortgage borrowers.

When employment growth weakens:

- Inflation pressures may ease.

- Consumer spending can slow.

- The Federal Reserve faces less pressure to raise interest rates.

- Investors often move money into bonds.

- Bond yields decline.

- Mortgage rates frequently move lower.

This relationship explains why disappointing economic news can sometimes create favorable conditions for homebuyers seeking financing.

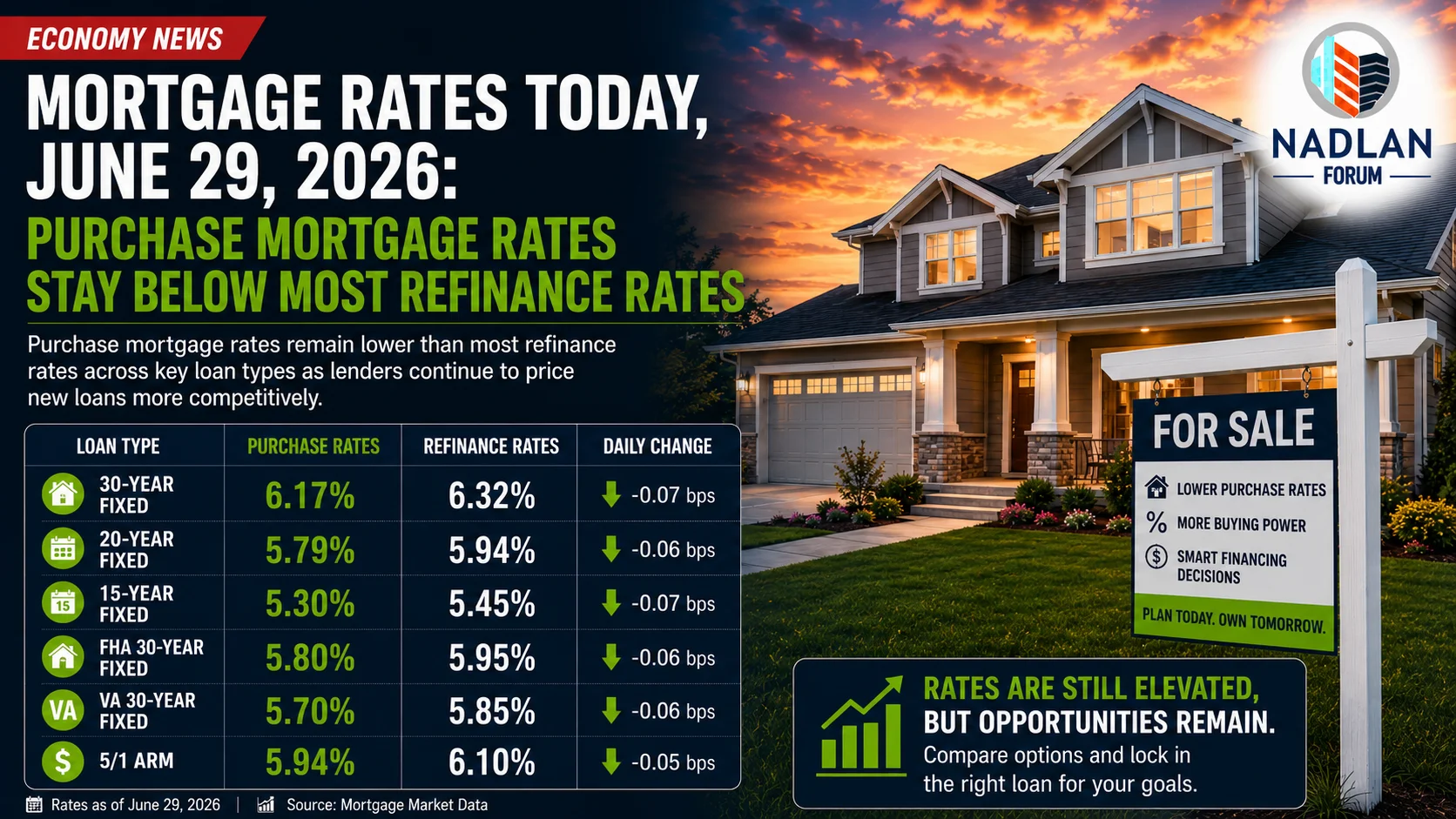

Mortgage Rates Ended the Week Slightly Higher

Despite recovering after the employment report, mortgage rates still finished the week modestly above their previous levels.

Average 30-year fixed mortgage rates ended approximately 0.07 percentage points higher than one week earlier.

The increase was relatively modest compared with the sharp daily swings experienced earlier in the week.

Importantly, borrowers are still seeing lower rates than those available during several periods earlier this year.

Why Some Mortgage Rate Reports Look Different

Consumers may notice that mortgage rate reports published by different organizations occasionally show conflicting numbers.

This occurs because various surveys use different collection methods.

Some weekly mortgage reports average rates over several business days, while others reflect daily market pricing.

When rates change rapidly during the week, weekly surveys may not immediately capture the full impact of market movements.

As a result, published averages can temporarily differ even though they are all measuring the same mortgage market.

What Could Move Mortgage Rates Next Week?

Several important events could influence mortgage rates during the coming week.

Financial markets will closely monitor:

- Federal Reserve meeting minutes

- Inflation data

- Treasury market activity

- Bond market performance

- Investor sentiment

- Additional economic reports

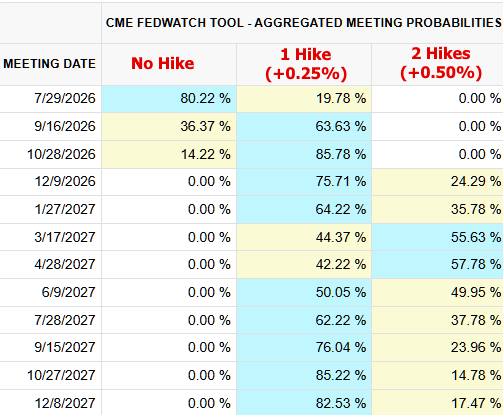

The minutes from the Federal Reserve’s most recent policy meeting may provide additional insight into how policymakers view inflation, economic growth, and future interest rate decisions.

Investors will analyze those discussions carefully for clues about the direction of monetary policy during the remainder of 2026.

Markets Still Expect Higher Interest Rates Later This Year

Despite the weaker June employment report, many investors continue to expect the Federal Reserve could raise short-term interest rates before the end of the year if inflation remains above its long-term target.

Expectations regarding future monetary policy continue to shift as new economic data becomes available.

Key indicators that will influence those decisions include:

- Inflation reports

- Employment growth

- Consumer spending

- Wage growth

- Gross Domestic Product (GDP)

- Financial market conditions

Mortgage rates are likely to remain sensitive to each of these reports throughout the second half of 2026.

What This Means for Homebuyers

Although mortgage rates remain elevated compared with the historically low levels of several years ago, recent market conditions offer a more balanced environment than many buyers experienced during the pandemic housing boom.

Housing inventory has improved across many markets, competition has moderated, and home price growth has slowed in numerous regions.

Even if mortgage rates fluctuate modestly from week to week, buyers who focus on strengthening their credit profile, comparing multiple lenders, and selecting the right loan program may still secure competitive financing.

Waiting for perfectly timed interest rates may prove less effective than preparing financially and taking advantage of improved housing market conditions.

Looking Ahead

The first week of July demonstrated how quickly mortgage rates can respond to financial market activity, even when economic conditions change very little.

Quarter-end bond market volatility temporarily pushed rates higher, but weaker-than-expected employment data helped offset much of that increase before the week concluded.

Going forward, inflation, Federal Reserve policy, labor market performance, and Treasury yields will continue to shape mortgage rate movements. While short-term volatility is likely to remain, current borrowing costs are still below the highs reached earlier this spring, providing a somewhat more favorable environment for buyers entering the housing market during the remainder of 2026. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses