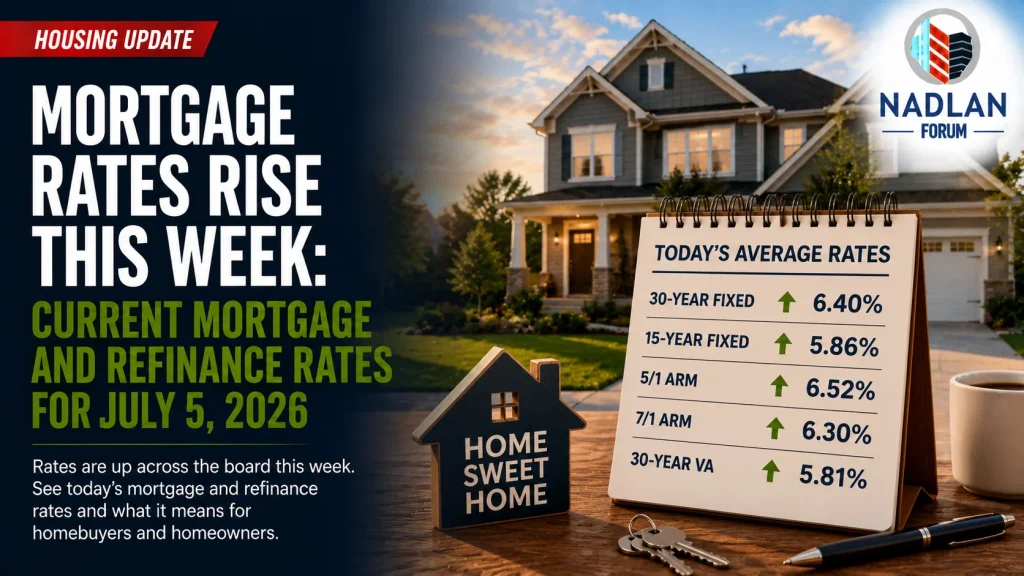

Mortgage Rates Rise This Week: Current Mortgage and Refinance Rates for July 5, 2026

Mortgage rates moved noticeably higher during the first week of July, reversing some of the stability seen in recent weeks. While rates remain within the range many economists expected for 2026, the latest increase means homebuyers and homeowners may face higher borrowing costs than they did just a week ago.

According to the latest national mortgage data, the average 30-year fixed mortgage rate climbed to 6.40%, while several other fixed and adjustable loan products also posted weekly increases. Although financing costs remain elevated compared with the historic lows of recent years, the broader housing market continues to benefit from improving inventory levels and slower home price growth in many regions.

For buyers planning to purchase a home or homeowners considering refinancing, understanding today’s rates and comparing loan options remains essential.

Mortgage Rates Increase Compared With Last Week

Mortgage rates have risen across most major loan products since late June.

Compared with one week earlier:

- 30-year fixed mortgage: 6.40% (up 23 basis points)

- 15-year fixed mortgage: 5.86% (up 11 basis points)

- 5/1 adjustable-rate mortgage (ARM): 6.52% (up 43 basis points)

Although these increases are significant on a week-to-week basis, mortgage rates remain near the range many housing economists projected for 2026.

Higher Treasury yields, changing economic expectations, and continued uncertainty surrounding inflation have all contributed to recent movements in mortgage pricing.

Current Mortgage Rates Today (July 5, 2026)

National average mortgage rates currently include:

- 30-year fixed: 6.40%

- 20-year fixed: 6.29%

- 15-year fixed: 5.86%

- 5/1 ARM: 6.52%

- 7/1 ARM: 6.30%

- 30-year VA: 5.81%

- 15-year VA: 5.51%

- 5/1 VA: 5.74%

These figures represent national averages. Individual borrowers may receive different rates depending on their credit score, loan amount, down payment, debt-to-income ratio, property type, and lender.

Current Mortgage Refinance Rates

Homeowners looking to refinance are seeing rates remain close to purchase loan pricing.

Current national refinance averages are:

- 30-year fixed: 6.38%

- 20-year fixed: 6.12%

- 15-year fixed: 5.84%

- 5/1 ARM: 6.33%

- 7/1 ARM: 6.04%

- 30-year VA: 5.80%

- 15-year VA: 5.51%

- 5/1 VA: 5.70%

Although refinance rates are often slightly higher than purchase rates, current market conditions have narrowed that gap for many loan products.

Whether refinancing makes financial sense depends on your existing mortgage rate, closing costs, remaining loan balance, and long-term financial goals.

Monthly Mortgage Payment Example

Mortgage rates directly affect monthly housing costs.

Using a home purchase price of $425,000 with a 20% down payment, a borrower would finance approximately $340,000.

At an interest rate near 6.36% on a 30-year fixed mortgage, estimated monthly costs include:

- Principal and interest: Approximately $2,119

- Estimated property taxes: About $354 per month

- Estimated homeowners insurance: Around $150 per month

This produces a total estimated monthly housing payment of approximately $2,623, excluding HOA fees or private mortgage insurance where applicable.

Even small changes in mortgage rates can significantly impact monthly payments and total interest paid over the life of the loan.

Comparing 30-Year and 15-Year Mortgages

Two of the most common mortgage options remain the 30-year fixed and 15-year fixed loans.

30-Year Fixed Mortgage

The 30-year mortgage continues to be the most popular option because it spreads payments over three decades, reducing monthly payment obligations.

For example, a $300,000 mortgage at approximately 6.41% would generate a monthly principal and interest payment of roughly $1,878.

However, borrowers would pay approximately $376,000 in interest over the life of the loan.

15-Year Fixed Mortgage

A 15-year mortgage generally offers a lower interest rate while allowing homeowners to pay off their loan much faster.

Using the same $300,000 mortgage at approximately 5.80%, the estimated monthly payment would increase to about $2,499, but total interest paid would decline to approximately $150,000.

Borrowers choosing between these options should consider both their monthly budget and long-term financial goals.

Fixed-Rate vs. Adjustable-Rate Mortgages

Borrowers also have the choice between fixed-rate and adjustable-rate mortgages.

A fixed-rate mortgage locks in the same interest rate for the full loan term, providing predictable monthly payments regardless of future market conditions.

An adjustable-rate mortgage (ARM) offers a fixed introductory rate for a set number of years before adjusting periodically based on market indexes and loan terms.

For example:

- A 5/1 ARM maintains its initial rate for five years before adjusting annually.

- A 7/1 ARM keeps the same rate for seven years before yearly adjustments begin.

Historically, ARMs often started with lower rates than fixed mortgages. However, in today’s market, some fixed-rate loans are priced similarly or even below adjustable-rate products, making careful comparison especially important.

How to Qualify for a Lower Mortgage Rate

Although overall market rates are beyond a borrower’s control, several personal financial factors can improve loan pricing.

Borrowers may qualify for better rates by:

- Maintaining a high credit score

- Making a larger down payment

- Reducing debt before applying

- Lowering their debt-to-income ratio

- Demonstrating stable income and employment

- Comparing offers from multiple lenders

Shopping with several lenders within a short period can also help borrowers identify the most competitive combination of interest rates, fees, and loan terms.

Why Comparing APR Matters

When evaluating mortgage offers, borrowers should look beyond the advertised interest rate.

The Annual Percentage Rate (APR) includes not only the interest rate but also many of the lender’s fees and financing costs.

Because APR reflects the overall annual cost of borrowing, it often provides a more accurate comparison between competing loan offers.

Reviewing both the interest rate and APR can help borrowers identify the best overall financing option rather than simply choosing the lowest advertised rate.

Are Mortgage Rates Expected to Fall?

Current forecasts suggest mortgage rates may remain relatively stable through the remainder of 2026.

Several housing economists expect the average 30-year fixed mortgage rate to remain in the 6.4% to 6.5% range during the second half of the year.

Future movements will depend on several economic factors, including:

- Inflation

- Federal Reserve policy

- Treasury yields

- Employment growth

- Consumer spending

- Overall economic conditions

While significant rate declines are not widely expected in the near term, moderate improvements remain possible if inflation continues to ease.

What This Means for Homebuyers

Although borrowing costs have increased compared with last week, today’s housing market offers several advantages that were less available during the highly competitive conditions of recent years.

Inventory has improved across many markets, giving buyers more choices and greater negotiating power. Sellers are also becoming more willing to offer concessions, complete repairs, and negotiate pricing in many areas.

For buyers who are financially prepared, focusing on finding the right property and securing competitive financing may be more productive than waiting for substantial interest rate declines that may not occur in the short term.

Looking Ahead

Mortgage rates remain an important factor shaping affordability across the housing market, and recent increases highlight how quickly borrowing costs can change.

Even so, today’s rates remain within the range anticipated by many housing analysts for 2026. Combined with improving housing inventory and moderating home price growth, current market conditions continue to provide opportunities for qualified buyers.

As inflation, employment, and Federal Reserve policy evolve throughout the year, mortgage rates are expected to remain responsive to new economic data. Borrowers who monitor market conditions, strengthen their financial profile, and compare multiple loan offers will be best positioned to secure favorable financing. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses