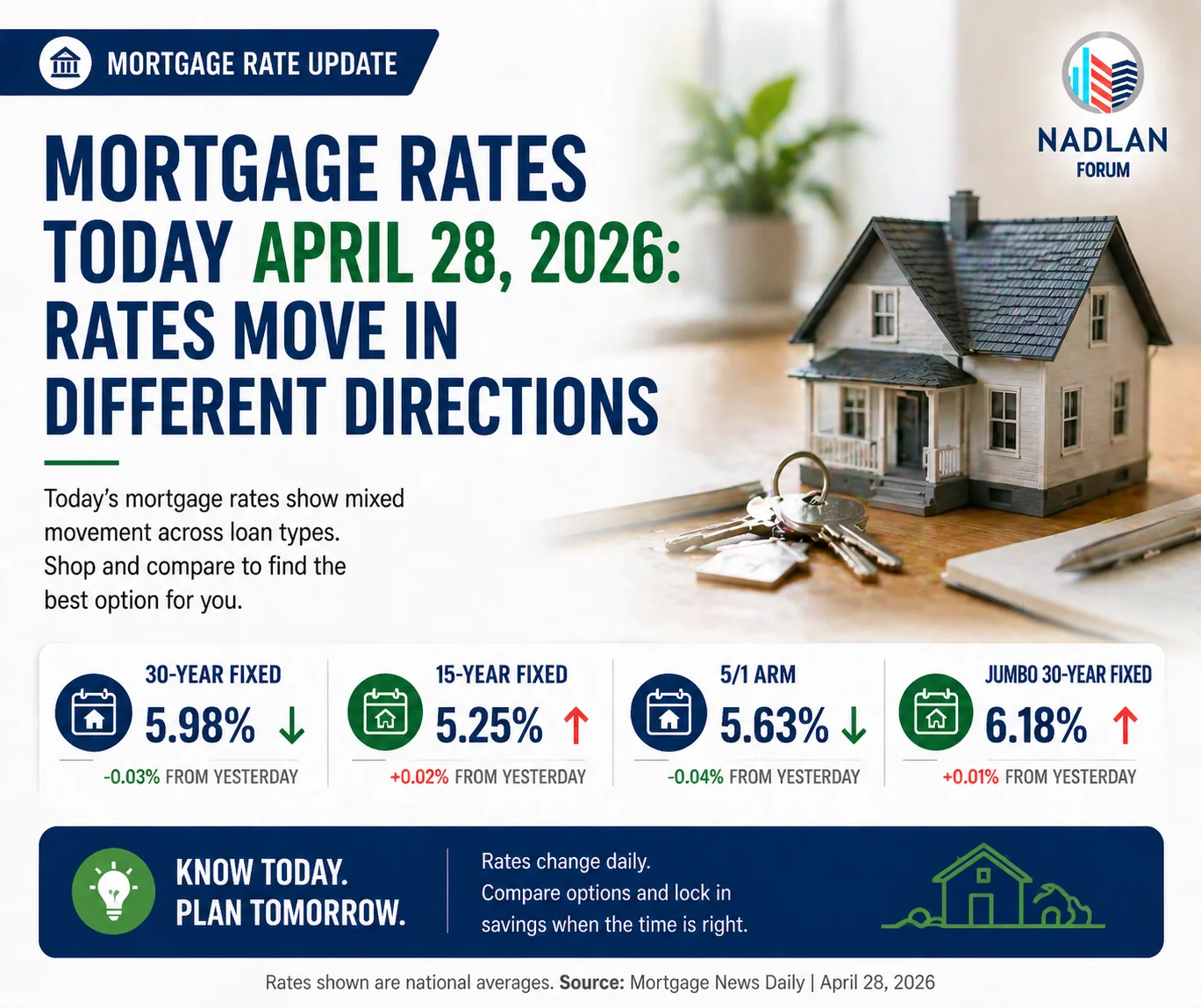

Homeowners and Insurers Face Rising Costs as 2025 Hurricane Season Begins

As the 2025 hurricane and wildfire season kicks off, homeowners and insurance providers alike are bracing for another year of climate-related challenges. From rising premiums to limited policy availability, the financial toll of natural disasters is becoming harder to ignore especially for those living in high-risk areas.

A recent report from the Federal Insurance Office (FIO) of the U.S. Department of the Treasury found that from 2018 to 2022, homeowners’ insurance premiums rose 8.7% faster than inflation, with much steeper increases for policyholders in regions frequently hit by wildfires, floods, and hurricanes.

Wildfires and Hurricanes: A Growing Financial Threat

Data from Deep Sky Research’s “Wildfires 2025” report, which analyzed conditions in California, Oregon, Texas, and Washington, shows that wildfire risk has increased twentyfold in recent years. The findings suggest that climate change is not only reshaping weather patterns, but also disrupting the insurance industry.

Meanwhile, the National Oceanic and Atmospheric Administration (NOAA) has issued an active hurricane season forecast. For the 2025 Atlantic season (June 1 – November 30), NOAA predicts:

- 13 to 19 named storms

- 6 to 10 hurricanes

- 3 to 5 major hurricanes (Category 3 or higher)

With stronger and more frequent storms predicted, both fire and water-related damage are expected to drive record-setting losses again this year.

High-Risk Homeowners Paying the Price

According to the Treasury Department, homeowners in the top 20% of climate-vulnerable ZIP codes paid an average annual premium of $2,321 a staggering 82% more than those in the lowest-risk zones.

“Insurance premiums are climbing, and skipping coverage is not a smart move right now,” said Shannon Martin, Insurance Expert at Bankrate. “As FEMA shifts more disaster relief responsibility to state governments, homeowners need both a solid insurance policy and an emergency fund.”

In states like Oklahoma, Nebraska, and Kansas, which are prone to tornadoes and hail, households are spending a higher share of their income on insurance than anywhere else in the country. Oklahoma leads the list, where 6.84% of the average household’s income about $6,133 annually goes toward home insurance. In contrast, Hawaii, California, and Washington, D.C. have the lowest insurance-to-income ratios.

Insurance Coverage Becomes Harder to Find

In many climate-vulnerable areas, insurance carriers are pulling back or refusing to renew policies altogether. From 2018 to 2022, nonrenewal rates in the highest-risk ZIP codes were about 80% higher than those in safer areas. This trend was especially noticeable in parts of California, the Gulf Coast, Florida, and Oklahoma.

“Insurance markets are signaling how climate change will affect broader financial systems,” said Max Dugan-Knight, Climate Data Scientist at Deep Sky. “When carriers can’t price risk accurately, they leave triggering ripple effects across property values, mortgages, and local economies.”

Major insurers such as Farmers, Progressive, and AAA have already scaled back operations or exited markets in disaster-prone states like Florida, where hurricanes and flooding risks are high.

Storm Preparation Costs Could Rise with New Tariffs

As homeowners prepare for hurricane season, rising material costs due to new federal tariffs could make storm readiness more expensive. Plywood, roofing nails, and generators staples for hurricane prep may soon cost more if Trump-era tariffs return after a mid-July grace period.

“Many don’t realize tariffs affect basic prep items,” Martin explained. “If you’re planning to stock up, now’s the time prices may spike mid-season.”

FEMA Budget Cuts Spark Concerns About Disaster Response

Adding to the uncertainty, FEMA’s ability to respond to major disasters has come into question. The agency has reportedly lost 30% of its full-time staff due to layoffs and Department of Government Efficiency (DOGE) buyouts.

During a House Rules Committee hearing, Rep. Jared Moskowitz of Florida warned that FEMA may not be able to respond effectively this year. He blamed budget cuts and criticized Homeland Security for reducing FEMA’s capacity.

“They’ve turned FEMA into Newark Airport,” Moskowitz said. “It’s overwhelmed and unprepared.”

President Trump has also indicated a shift in FEMA’s role, suggesting that state governments should take more responsibility for disaster relief a move that has drawn criticism from lawmakers in storm-prone regions.

Bottom Line:

As the 2025 storm season begins, homeowners face a perfect storm of risks: higher premiums, limited policy availability, increased storm severity, and uncertain federal aid. With wildfire threats rising and hurricane forecasts intensifying, preparation and protection has never been more critical. Visit Nadlan Capital Group for more information about finance.

Responses