New Home Listings Move Closer to Pre-Pandemic Levels as Inventory Slowly Recovers

Fresh data from First American shows that the housing market is still moving at a slow pace, with existing-home sales stuck near a 4-million-per-year rhythm. Even with steady demand, high prices and limited affordability continue to hold back the number of completed transactions. But there is a small but meaningful bright spot: new home listings are rising and getting closer to where they were before the pandemic, giving buyers more choices than they’ve had in years.

The return of supply matters because the years before 2020 particularly 2018 and 2019 represent one of the last periods when demand, supply, and mortgage rates were more evenly matched. Comparing today’s numbers with that baseline helps show how far the market has come after the extreme swings of the pandemic, including the intense seller’s market, rapid price spikes, and record-low rates followed by sharp rate increases.

In most markets, sales tend to pick up when new listings approach “normal” levels, and that trend appears to be returning.

“As more homeowners list their properties, more buyers get the chance to act. This supports a healthier flow of transactions and nudges the market toward balance,” said Odeta Kushi, Deputy Chief Economist at First American.

A Closer Look at Sales and Listing Patterns Across the Country

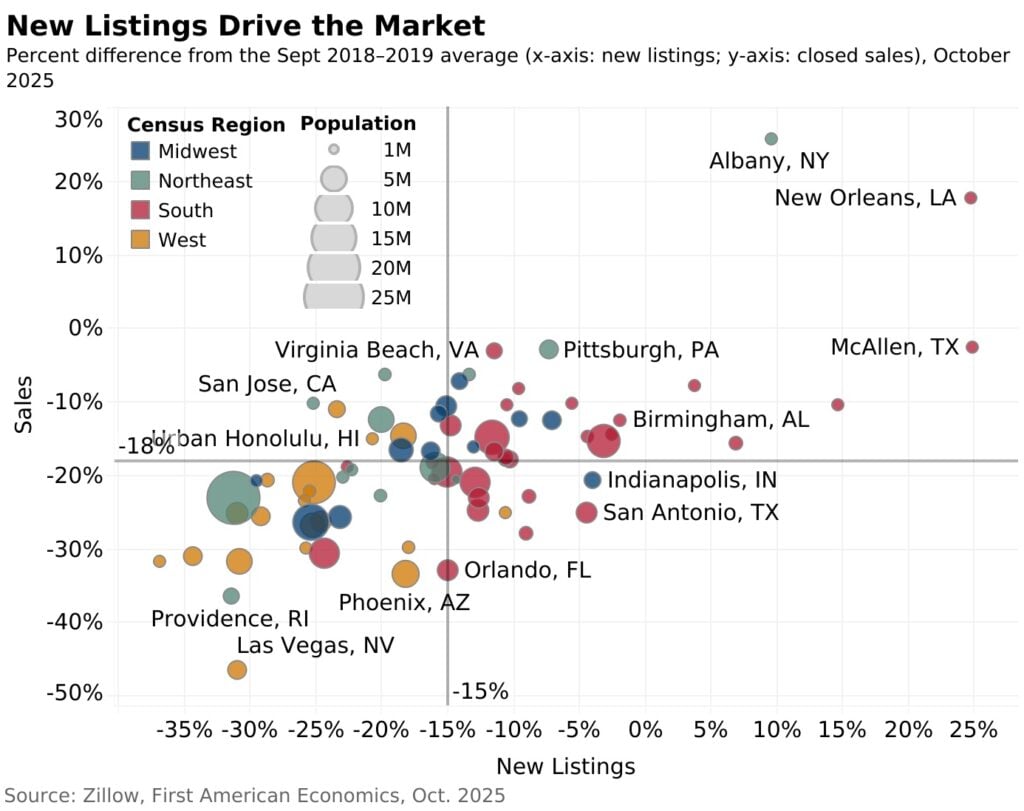

To understand how the market is progressing, First American compared October 2025 sales counts and new listings in 75 major metros against each metro’s own 2018–2019 average for the same month. Instead of focusing on total inventory which can rise simply because homes are taking longer to sell this approach highlights new listings, which directly measure how many fresh options buyers receive.

The outcome forms a simple four-quadrant snapshot of where markets stand today:

1. Pace Setters

These markets are closest to their pre-pandemic levels for both sales and new listings.

They appear to be leading the normalization trend. Examples include:

- Pittsburgh

- Knoxville, TN

- Virginia Beach, VA

Many of these markets are in the South, Northeast, and Midwest regions where prices tend to be more reasonable.

2. Demand-Ahead Markets

Sales are closer to “normal” than listings, meaning buyers are active but supply remains tight.

Northeastern and Midwestern markets dominate this category, including places like:

- Boston

- Detroit

If these areas see more sellers enter the market, they could quickly shift into the pace-setter group.

3. Supply-Ahead Markets

New listings look more normal than the demand side. These markets largely in the South are seeing better supply but slower buyer response because of affordability pressures or local economic trends.

Examples include:

- San Antonio

- Tampa, FL

This gap may narrow if mortgage rates dip or local job markets strengthen.

4. Stuck-in-Neutral Markets

Both sales and new listings are further from their pre-pandemic levels than the national average.

Many Western metros fall here, including:

- Portland, OR

- Los Angeles

These markets still face soft sales activity and low listing counts, reflecting ongoing affordability challenges and slower population growth.

More Listings Are Helping Ease a Complicated Housing Market

The link between rising new listings and stabilizing sales is clear. As inventory improves, even slowly, it provides the foundation for a healthier market one where buyers can shop and sellers can move without being stuck.

For October, First American’s updated Existing-Home Sales Outlook shows:

- Existing-home sales are projected to rise 0.3% from September

- Sales are expected to be 1.1% higher than one year ago

The drivers behind this increase include:

- A still-resilient economy (+0.3% influence)

- A gradually easing rate-lock effect (+0.3%) measured using the gap between current mortgage rates and the average rate homeowners already have

- A small boost in buying power (+0.1%)

(Note: The mortgage-rate spread is measured with a two-month delay in the modeling.)

Looking Ahead

The U.S. housing market still faces affordability hurdles, and sales remain far below pre-pandemic highs. But the steady rise in new listings paired with a slowly easing rate environment suggests that 2026 could bring more movement for both buyers and sellers.

If supply continues to climb, even gradually, the market could move one step closer to stability. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses