Real Estate Debt Funds: Investment Guide for 2026

Real estate debt funds have emerged as a compelling alternative investment vehicle for investors seeking stable income streams with reduced volatility compared to equity investments. These specialized funds pool capital from multiple investors to originate or acquire debt secured by real estate properties, offering an attractive middle ground between traditional bonds and direct property ownership. As the commercial real estate market continues to evolve in 2026, understanding the mechanics, benefits, and risks associated with these investment vehicles has become increasingly important for sophisticated investors looking to diversify their portfolios.

Understanding Real Estate Debt Fund Structures

Real estate debt funds operate by collecting capital from qualified investors and deploying those funds into various forms of real estate-backed loans. The fundamental premise involves lending money to property owners or developers who need financing for acquisitions, refinancing, construction projects, or property improvements. In exchange for providing this capital, the fund receives regular interest payments and principal repayment at loan maturity.

Primary Investment Strategies

These funds typically pursue one of several distinct strategies based on risk tolerance and return objectives:

- Senior debt: First-lien mortgages with conservative loan-to-value ratios, typically 55-70%

- Mezzanine debt: Subordinated loans positioned between senior debt and equity, offering higher yields

- Bridge loans: Short-term financing for transitional properties or borrowers requiring quick capital

- Construction loans: Funding for ground-up development or major renovation projects

- Preferred equity: Hybrid instruments with debt-like characteristics but positioned in the capital stack above common equity

The structure and function of real estate debt funds varies significantly based on these strategic approaches, with each offering different risk-return profiles suited to diverse investor objectives.

Market Performance and Growth Trends

The real estate debt funds sector has experienced substantial expansion over the past decade, with institutional investors increasingly allocating capital to this asset class. According to recent market research, senior debt funds have demonstrated particularly strong performance compared to other private asset classes, attracting significant attention from pension funds, endowments, and family offices.

Historical Returns and Benchmarking

Real estate debt funds have historically delivered returns ranging from 6% to 15% annually, depending on the strategy and risk profile. Senior secured loans typically generate returns in the 7-10% range, while mezzanine and subordinated debt can produce yields of 12-15% or higher.

| Strategy Type | Typical Annual Return | Loan-to-Value Range | Investment Horizon |

|---|---|---|---|

| Senior Debt | 7-10% | 55-70% | 3-7 years |

| Mezzanine Debt | 12-15% | 70-85% | 2-5 years |

| Bridge Loans | 9-13% | 60-75% | 6-24 months |

| Construction Loans | 10-14% | 65-80% | 1-3 years |

These performance metrics reflect the stability and income-generating potential that attracts investors seeking alternatives to traditional fixed-income securities. The consistency of returns stems from contractual interest payments and the secured nature of the underlying collateral.

Key Advantages for Investors

Real estate debt funds offer several compelling benefits that differentiate them from other investment vehicles. Understanding these advantages helps investors determine whether this asset class aligns with their portfolio objectives and risk tolerance.

Income Generation and Stability

One of the primary attractions is the regular cash flow generated through monthly or quarterly interest payments. Unlike equity investments that depend on property appreciation or rental income growth, debt investments provide predictable income streams based on contractual terms. This characteristic makes them particularly appealing for investors prioritizing current income over long-term capital appreciation.

Principal protection represents another significant advantage. Debt holders occupy a senior position in the capital structure, meaning they receive repayment before equity investors in liquidation scenarios. Additionally, conservative loan-to-value ratios provide a cushion against property value declines.

The asset class also offers:

- Lower volatility compared to equity real estate investments

- Diversification benefits when combined with stocks and bonds

- Inflation hedge characteristics as interest rates typically rise with inflation

- Professional management by experienced lending teams

- Access to institutional-quality deals unavailable to individual investors

Risk Considerations and Mitigation Strategies

While real estate debt funds present attractive opportunities, investors must understand the associated risks to make informed decisions. No investment is without potential drawbacks, and debt funds face several specific challenges that require careful evaluation.

Credit and Default Risk

The most significant risk involves borrower default and potential loss of principal. If a property owner cannot meet payment obligations, the fund must pursue foreclosure or restructuring, which can be costly and time-consuming. Even with collateral backing, property value declines may result in recovery amounts below the outstanding loan balance.

Market cycle timing also presents challenges. Real estate markets operate in cycles, and debt funds originated near market peaks may face higher default rates when conditions deteriorate. Experienced fund managers mitigate this through disciplined underwriting, conservative valuations, and diversification across property types and geographic markets.

Interest rate fluctuations create additional complexity. Rising rates can reduce property values and make refinancing more difficult for borrowers, potentially increasing default risk. Conversely, falling rates may trigger early loan repayments, forcing funds to redeploy capital at lower yields.

| Risk Factor | Impact Level | Mitigation Approach |

|---|---|---|

| Borrower Default | High | Conservative LTV, thorough due diligence |

| Property Value Decline | Medium-High | Diversification, stress testing |

| Interest Rate Changes | Medium | Rate floors, shorter loan terms |

| Market Cycle Timing | Medium | Disciplined underwriting standards |

| Liquidity Constraints | Low-Medium | Appropriate fund term matching |

Due Diligence and Manager Selection

Selecting the right fund manager represents one of the most critical decisions investors face when allocating capital to real estate debt funds. The manager’s experience, track record, and investment process directly impact returns and risk management effectiveness.

Evaluating Track Records

Prospective investors should examine historical performance across multiple market cycles, not just recent years. Managers who successfully navigated the 2008-2009 financial crisis demonstrate resilience and risk management capabilities that prove invaluable during future downturns. Key metrics to evaluate include:

- Cumulative default rates across all vintages

- Loss severity on defaulted loans after recovery

- Net returns to investors after fees and expenses

- Consistency of distributions throughout various market conditions

- Portfolio diversification across property types and geographies

The investment team’s expertise matters significantly. Look for managers with decades of lending experience, strong relationships with borrowers and brokers, and robust underwriting processes. Firms like Lone Star Funds demonstrate the institutional approach that characterizes successful long-term managers.

Operational Infrastructure

Beyond investment acumen, operational capabilities ensure effective portfolio management and investor reporting. Quality managers maintain sophisticated systems for:

- Property appraisal and ongoing valuation monitoring

- Borrower financial analysis and covenant tracking

- Legal documentation and compliance oversight

- Servicing and workout procedures for troubled loans

- Transparent investor reporting with detailed performance metrics

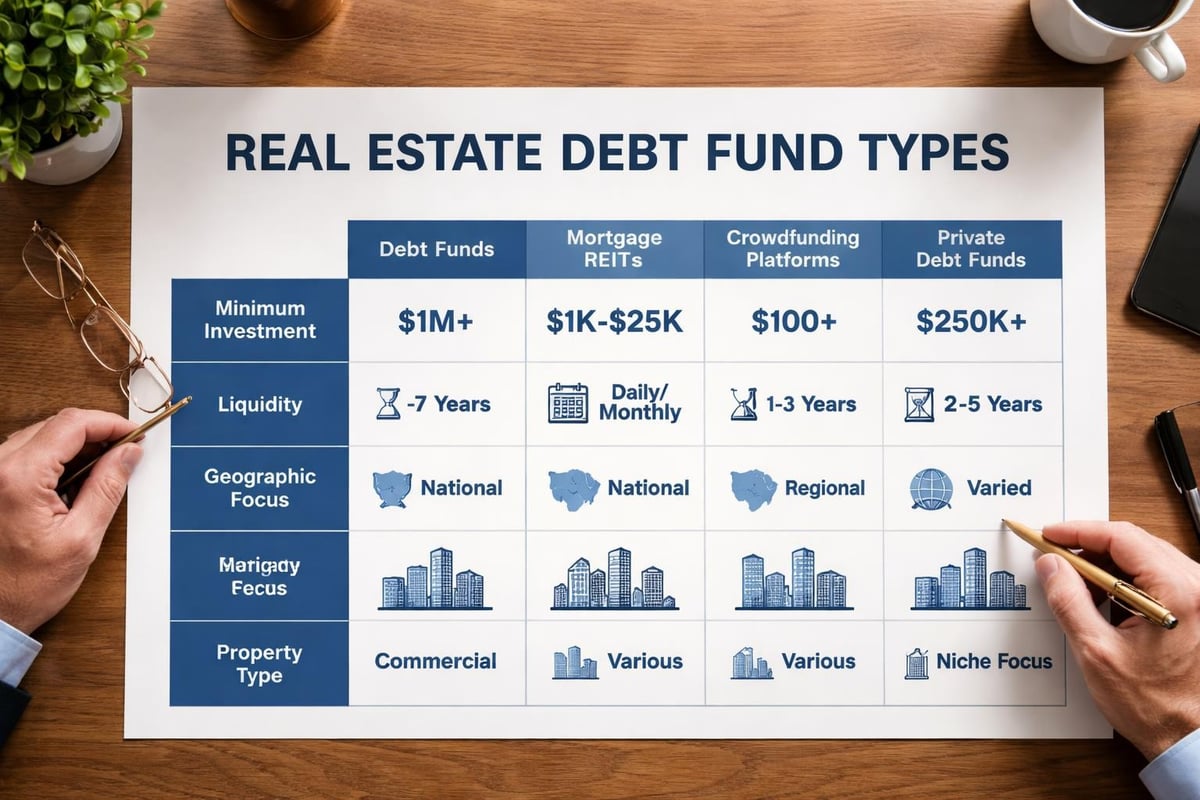

Accessing Real Estate Debt Investments

Investors can access this asset class through multiple channels, each with distinct characteristics regarding minimum investments, liquidity terms, and fee structures. Understanding these options helps align investment choices with individual circumstances and objectives.

Private Debt Funds

Institutional-quality private funds typically require substantial minimum investments ranging from $250,000 to $5 million or more. These vehicles generally target accredited or qualified purchaser investors and operate with limited liquidity. Investors commit capital for multi-year periods, often 3-7 years, receiving distributions as loans mature or are refinanced.

Capstone’s private real estate debt offerings exemplify this approach, focusing on stable passive income through carefully structured senior loans. Similarly, Redwood’s debt fund strategies emphasize current income and capital preservation for shareholders through disciplined lending practices.

Regional and Specialty Funds

Some managers focus on specific geographic markets or property types, offering concentrated exposure for investors with particular preferences. Northwind Group’s commercial real estate debt funds demonstrate this specialized approach, concentrating on particular market segments with deep local expertise.

Regional strategies can provide advantages including:

- Superior market knowledge and deal flow

- Stronger borrower relationships

- Better property inspection and monitoring capabilities

- Reduced competition from national lenders in certain markets

Integration with Broader Investment Strategies

Real estate debt funds should not exist in isolation but rather as components of comprehensive portfolio strategies. Understanding how these investments interact with other asset classes helps optimize overall risk-adjusted returns.

Portfolio Allocation Considerations

Financial advisors typically recommend allocating 5-15% of investable assets to alternative investments, with real estate debt representing a portion of that allocation. The exact percentage depends on individual factors including:

- Risk tolerance and capacity to absorb potential losses

- Income needs and preference for current cash flow versus growth

- Investment timeline and liquidity requirements

- Tax situation and sensitivity to ordinary income taxation

- Existing portfolio composition and diversification gaps

Real estate debt funds complement traditional stock and bond portfolios by providing non-correlated returns and income stability. During equity market downturns, the contractual nature of debt payments can provide ballast, though severe recessions may still impact default rates.

For investors engaged in house flipping or other active real estate strategies, debt funds offer passive exposure without the operational demands of direct property investment. This creates a balanced approach combining hands-on projects with professionally managed lending portfolios.

Tax Implications and Reporting

Understanding the tax treatment of real estate debt fund investments helps investors accurately project after-tax returns and fulfill reporting obligations. The tax characteristics differ significantly from equity real estate investments, requiring specific consideration during planning.

Income Taxation

Interest income generated by debt funds typically receives treatment as ordinary income, taxed at the investor’s marginal rate rather than the preferential capital gains rates applied to long-term equity appreciation. This can result in higher tax obligations for investors in elevated tax brackets.

However, some funds structure investments to generate qualified business income eligible for the Section 199A deduction, potentially reducing the effective tax rate by up to 20%. Investors should consult tax advisors to understand how specific fund structures impact their individual situations.

K-1 reporting represents another consideration. Many private debt funds issue Schedule K-1 forms rather than 1099 statements, which can complicate tax preparation and potentially delay filing. These forms may report income from multiple states, creating additional complexity and potential state tax filing requirements.

Current Market Dynamics in 2026

The real estate debt landscape continues evolving in response to broader economic conditions, regulatory changes, and shifting investor preferences. Several trends are shaping opportunities and challenges for both fund managers and investors.

Interest Rate Environment

Following the Federal Reserve’s policy adjustments over recent years, the interest rate environment in 2026 presents both opportunities and challenges for debt fund investors. Higher base rates have increased potential yields on new loan originations, making debt funds more competitive with traditional fixed-income alternatives.

However, existing borrowers face refinancing challenges as their loans mature, potentially increasing default risk for properties with weak fundamentals or overleveraged capital structures. Experienced managers navigate this environment by focusing on quality borrowers and properties in strong markets with sustainable cash flows.

Competitive Landscape

The real estate debt market has become increasingly competitive as banks face regulatory constraints and private capital fills the financing gap. This competition can compress yields on senior loans in prime markets, pushing some managers toward riskier segments or secondary markets to achieve target returns.

Non-listed real estate debt funds in Europe have demonstrated how this market segment continues expanding globally, providing insights into structural trends that influence the U.S. market as well.

Evaluating Fund Terms and Fee Structures

Beyond investment strategy and manager selection, understanding fund terms and fee arrangements directly impacts net returns. Investors should carefully review offering documents to ensure alignment of interests between managers and capital providers.

Management and Performance Fees

Most debt funds charge annual management fees ranging from 1.0% to 2.0% of committed or invested capital. Additionally, many structures include performance fees or carried interest, typically 10-20% of profits above a preferred return hurdle.

Common fee structures include:

- Management fees: 1.5% annually on invested capital

- Acquisition fees: 0.5-1.0% on loan originations

- Performance fees: 15-20% above 8% preferred return

- Servicing fees: Ongoing charges for loan administration

Investors should calculate total expense ratios and compare net return projections across multiple managers. Lower fees do not always indicate better value if investment performance suffers, but excessive charges can significantly erode returns over time.

Liquidity Terms and Redemption Provisions

Understanding liquidity constraints prevents surprises when capital needs arise. Most private debt funds operate as closed-end vehicles with specific fund terms, often 5-7 years with possible extensions. Investors generally cannot withdraw capital before fund maturity except through secondary market sales at potentially significant discounts.

Some funds offer limited quarterly redemption windows with advance notice requirements and potential redemption fees. These provisions protect remaining investors from forced asset sales but reduce flexibility for those needing access to capital.

Specialized Strategies and Niche Opportunities

Beyond traditional commercial mortgage lending, some debt funds pursue specialized strategies offering differentiated return profiles and risk characteristics. These approaches may appeal to investors seeking specific exposures or enhanced yields.

High-Yield Mortgage Strategies

Certain managers focus on higher-yielding opportunities in the debt spectrum, often involving transitional properties, value-add projects, or borrowers with unique circumstances. IM Capital’s high-yield mortgage approach demonstrates how specialized expertise can optimize risk-adjusted returns through careful underwriting and active portfolio management.

These strategies typically involve:

- Lower-rated borrowers with strong business plans

- Properties requiring renovation or repositioning

- Shorter loan terms with higher yields

- More active monitoring and potential workout situations

- Enhanced returns compensating for elevated risk

Short-Term Lending Programs

Some funds specialize in bridge and transitional financing, providing capital for borrowers who need quick closings or temporary funding before permanent financing. Stallion Funding’s Texas real estate funds exemplify this approach, deploying capital into short-term loans generating attractive yields through rapid turnover.

Benefits of short-term strategies include faster capital recycling, reduced interest rate risk from shorter durations, and flexibility to adjust to changing market conditions. However, these programs require robust origination pipelines to consistently redeploy capital as loans mature.

Regulatory Considerations and Compliance

Real estate debt funds operate within a complex regulatory framework that protects investors while imposing requirements on fund managers. Understanding this landscape helps investors evaluate fund legitimacy and manager professionalism.

Securities Registration and Exemptions

Most private debt funds operate under Regulation D exemptions from securities registration, limiting participation to accredited investors who meet specific income or net worth thresholds. These exemptions reduce regulatory burdens and costs but restrict the investor base to financially sophisticated individuals and institutions.

Fund managers must comply with:

- Anti-fraud provisions requiring accurate disclosure of material facts

- Custody rules protecting investor assets from misappropriation

- Valuation standards ensuring fair pricing of illiquid holdings

- Reporting requirements providing transparency to investors and regulators

- Marketing restrictions limiting general solicitation in certain circumstances

Reputable managers maintain comprehensive compliance programs and engage third-party administrators, auditors, and legal counsel to ensure adherence to applicable regulations.

Building a Diversified Debt Fund Portfolio

For investors allocating substantial capital to real estate debt, diversification across multiple funds can reduce manager-specific and strategy-specific risks. A thoughtfully constructed portfolio combines complementary approaches to optimize risk-adjusted returns.

Strategic Allocation Framework

A diversified debt fund portfolio might include:

| Fund Type | Allocation | Primary Objective | Risk Level |

|---|---|---|---|

| Senior Secured Debt | 40-50% | Income stability, capital preservation | Low-Medium |

| Mezzanine/Subordinated | 20-30% | Enhanced yield | Medium-High |

| Bridge/Transitional | 15-25% | Opportunistic returns | Medium |

| Specialty/Niche | 10-15% | Diversification, unique opportunities | Varies |

This framework balances conservative senior debt providing stability with higher-yielding strategies enhancing overall returns. Adjustments should reflect individual risk tolerance and market conditions.

Geographic and Property Type Diversification

Beyond strategy diversification, spreading investments across multiple markets and property types reduces concentration risk. Economic downturns rarely affect all regions equally, and different property sectors perform differently throughout market cycles.

Industrial and multifamily properties have demonstrated resilience through recent cycles, while office and retail face structural challenges from remote work and e-commerce trends. Debt investors should consider these dynamics when evaluating fund portfolios.

Emerging Trends and Future Outlook

The real estate debt landscape continues evolving as technology, demographic shifts, and economic forces reshape borrowing needs and lending practices. Forward-looking investors monitor these trends to identify emerging opportunities and potential risks.

Technology Integration

Data analytics and artificial intelligence increasingly influence underwriting processes, enabling more sophisticated risk assessment and pricing. Managers leveraging these tools can identify opportunities others miss while avoiding problematic credits.

Digital platforms also improve loan servicing efficiency and investor reporting transparency. Some managers now offer real-time portfolio access through secure online portals, enhancing the investor experience.

Sustainable Lending Practices

Environmental, social, and governance considerations increasingly influence lending decisions. Some debt funds now incorporate sustainability metrics into underwriting, potentially offering preferential terms for energy-efficient properties or developments meeting green building standards.

This trend reflects broader investor demand for responsible investing while potentially reducing long-term risk as properties with superior environmental performance may maintain values better through economic cycles.

Real estate debt funds represent a sophisticated investment vehicle offering attractive income potential, portfolio diversification, and professional management for qualified investors navigating the 2026 market landscape. By understanding fund structures, evaluating manager capabilities, and aligning investments with broader portfolio objectives, investors can effectively harness these opportunities while managing associated risks. Whether you’re exploring debt funds as a complement to active real estate projects or seeking passive income alternatives, Nadlan Forum provides the resources, community insights, and expert guidance to help you make informed investment decisions and build wealth through strategic real estate allocation.

Responses