Fannie Mae Mortgage Portfolio Growth: Government Pushes to Support Lower Rates

Fannie Mae Expands Mortgage Holdings

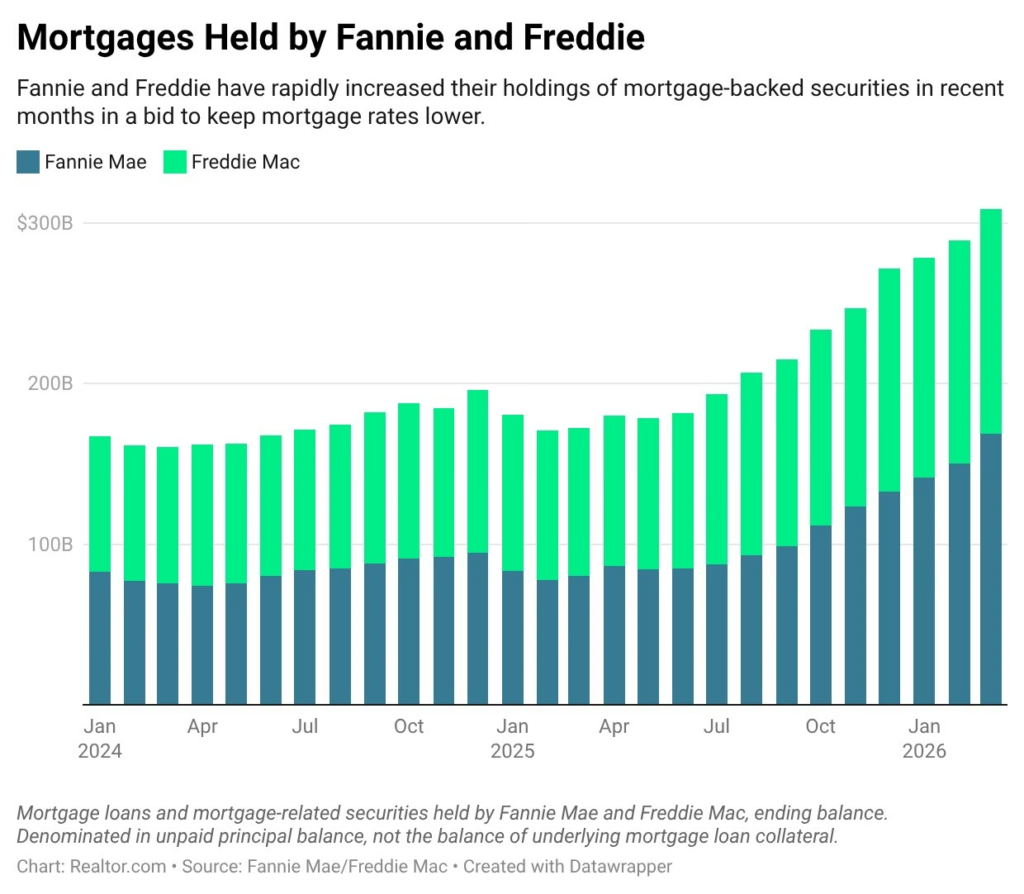

Fannie Mae has significantly increased its mortgage holdings over the past year as the federal government looks for ways to support the housing market and reduce borrowing costs.

In March alone, the company added roughly $18.3 billion to its retained mortgage portfolio. Over the entire first quarter, portfolio growth reached approximately $36 billion.

Fannie Mae’s total retained portfolio now stands near $168.7 billion, more than double the balance it held a year earlier.

Push to Support the Housing Market

The expansion comes as the administration continues looking for ways to lower mortgage rates and improve housing affordability.

Earlier this year, the administration directed both Freddie Mac and Fannie Mae to purchase large amounts of mortgage-backed securities.

The goal is to strengthen the secondary mortgage market and improve liquidity, which can help reduce borrowing costs for homebuyers.

By increasing demand for mortgage-backed securities, Fannie Mae and Freddie Mac may help lower mortgage rates indirectly.

How Mortgage-Backed Security Purchases Affect Rates

Mortgage-backed securities are bundles of home loans sold to investors. When organizations like Fannie Mae purchase more of these securities, it increases demand in the market.

Higher demand can help push mortgage yields lower, which may eventually reduce rates offered to borrowers.

Economists say this strategy is intended to make homeownership more affordable at a time when elevated mortgage rates continue to limit buyer activity.

Portfolio Growth Accelerated Quickly

Fannie Mae sharply expanded operations during the first quarter of 2026.

The company reported:

- $84.4 billion in purchases

- $41.7 billion in dispositions

- $6.5 billion in liquidations

As a result, the retained mortgage portfolio increased from approximately $132.5 billion at the end of 2025 to nearly $168.7 billion by March.

Compared to March of last year, the retained portfolio balance has more than doubled.

Shift Toward Higher-Yielding Assets

Company leadership said part of the strategy involves shifting investments toward higher-yielding mortgage assets.

At the same time, the company reduced some holdings in its liquidity portfolio while increasing mortgage-related investments.

Executives stated that the company remains focused on supporting liquidity and stability in the housing market across all economic conditions.

Administration Also Exploring IPO Possibility

Discussions have also continued around the future structure of Fannie Mae and Freddie Mac.

Both companies have remained under government conservatorship since the 2008 financial crisis. There has been renewed conversation about potentially returning the organizations to public markets through a large public offering.

Some estimates suggest a future offering involving both companies could be valued in the hundreds of billions of dollars.

However, opinions remain divided among policymakers and market analysts about whether such a move would improve or complicate housing finance stability.

Risks Continue to Exist

While expanding mortgage purchases may help improve affordability, the strategy also increases financial risk.

Holding more mortgages directly on company balance sheets exposes Fannie Mae more heavily to potential losses if borrowers fail to repay loans.

This type of exposure became a major issue during the 2007-2008 housing crisis, when rising defaults created severe losses across the mortgage market.

Since then, stricter safeguards and oversight measures have been implemented to reduce systemic risk.

Housing Supply Still the Bigger Problem

Some economists argue that mortgage rates alone are not the main issue facing the housing market.

While lower borrowing costs could help buyers, the larger challenge remains limited housing supply. In many markets, there are still not enough homes available to meet demand.

Inventory shortages continue to keep prices elevated, even as affordability pressures grow.

Mortgage Rates Remain Elevated

Mortgage rates have remained relatively high in 2026 due to ongoing inflation concerns, energy price pressures, and global uncertainty.

Although some government actions may help stabilize borrowing costs, broader economic conditions continue to influence the mortgage market.

This means affordability challenges are likely to remain even if rates decline modestly.

What This Means for Homebuyers

For buyers, efforts to stabilize mortgage rates could provide some relief if financing costs move lower over time.

However, affordability still depends on several factors, including:

- Home prices

- Household income growth

- Housing supply

- Inflation trends

Even small changes in mortgage rates can affect monthly payments and overall purchasing power.

Final Thoughts

Fannie Mae’s rapid mortgage portfolio growth highlights how policymakers are trying to support the housing market during a period of elevated borrowing costs and affordability challenges.

While increased mortgage-backed security purchases may help lower rates, the housing market still faces larger structural issues tied to supply shortages and inflation pressures. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses