Home Insurance Costs 2026: Rising Premiums Add Pressure on Housing

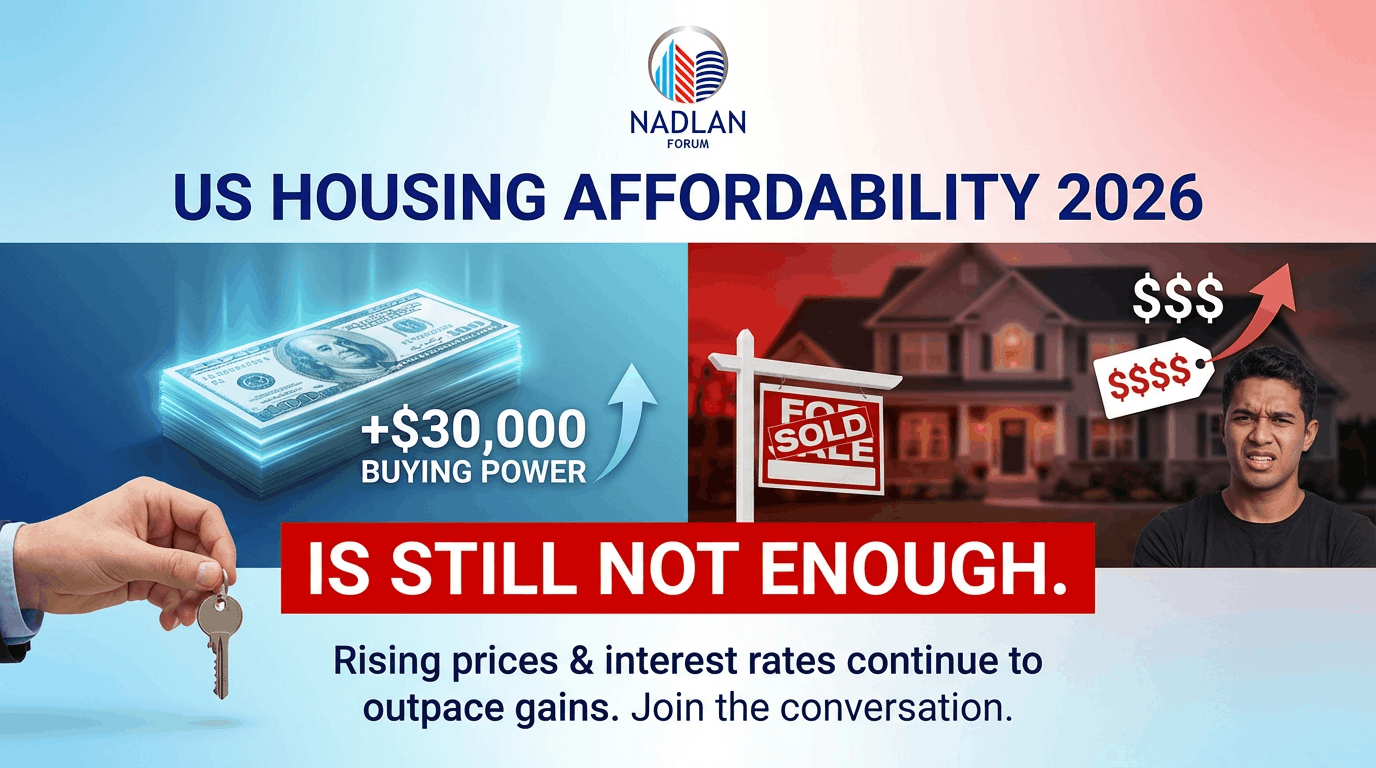

The cost of owning a home is rising, and insurance is becoming a bigger part of the financial burden. A recent study based on nearly 1.2 million mortgage loans shows that home insurance premiums have increased sharply over the past few years, adding new pressure to housing affordability.

While home values have also grown during this time, the rapid rise in insurance costs is making it harder for many homeowners and buyers to manage monthly expenses.

Insurance Costs Have Risen Sharply Since 2021

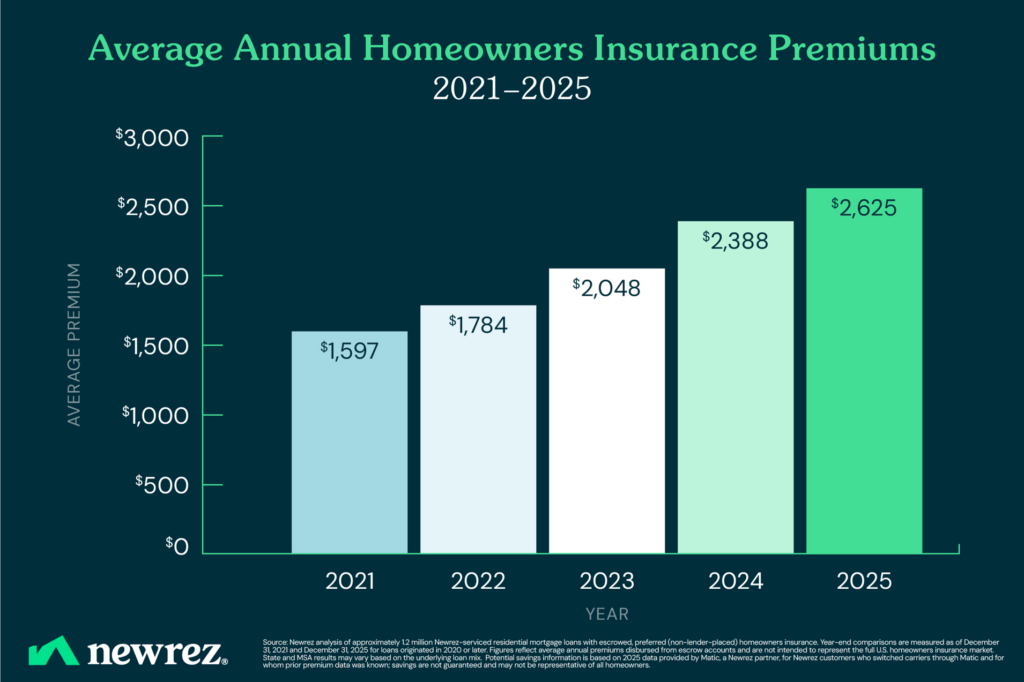

Data from Newrez shows that the average annual home insurance premium increased significantly between 2021 and 2025.

- 2021 average premium: $1,597

- 2025 average premium: $2,625

- Total increase: about 64%

Premiums saw strong increases between 2022 and 2024, with double-digit growth each year. However, the pace slowed in 2025, with a 10% increase the lowest growth rate in recent years.

Even with this slowdown, costs remain much higher than just a few years ago.

Home Values Rise, But Costs Still Climb

During the same period, home values also increased.

According to the Zillow Home Value Index, average home prices rose by roughly $50,000 between 2021 and 2025.

This growth has helped homeowners build equity, which supports long-term financial stability. However, rising insurance premiums are offsetting some of these gains by increasing monthly housing costs.

Why Insurance Premiums Are Increasing

Several factors are driving higher insurance costs:

Severe Weather Events

More frequent storms, floods, and wildfires are increasing claims, which leads insurers to raise premiums.

Higher Rebuilding Costs

Construction materials and labor have become more expensive, making it costlier to repair or rebuild homes.

Risk-Based Pricing

Insurance companies are adjusting prices based on local risks, which can vary widely by region.

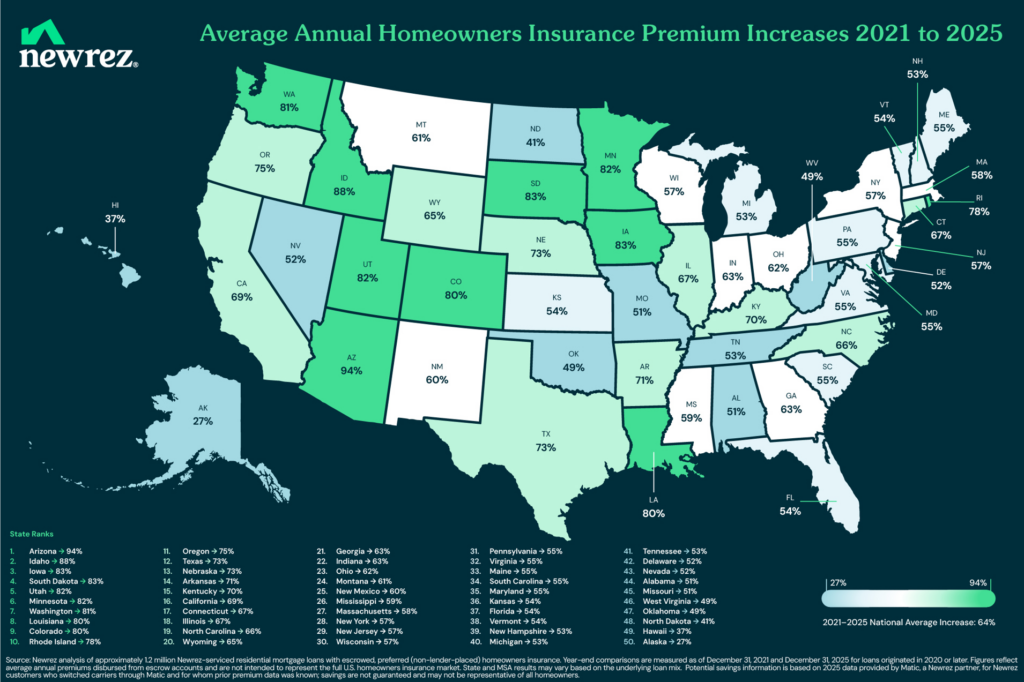

Regional Differences in Insurance Costs

Insurance premiums are not the same across the country. Some areas are seeing much higher costs due to weather risks and rebuilding expenses.

States with the highest average annual premiums include:

- Louisiana: $4,238

- Florida: $4,060

- Texas: $3,952

- Nebraska: $3,898

- Colorado: $3,854

These higher costs often reflect exposure to hurricanes, floods, or severe storms.

Fastest-Growing Insurance Costs

Some states have seen especially large increases over the past few years.

Top increases between 2021 and 2025:

- Arizona: +94%

- Idaho: +88%

- Iowa: +83%

- South Dakota: +83%

- Utah: +82%

By comparison, Alaska saw the smallest increase at around 27%.

These differences show how local conditions play a major role in determining insurance costs.

Metro-Level Trends

Insurance costs also vary widely between cities.

- Miami area: highest average premium at $5,546

- Seattle area: lowest among major metros at $2,087

While Miami has high costs due to hurricane risk, cities with lower natural disaster exposure tend to have more affordable premiums.

Impact on Homeowners and Buyers

Rising insurance costs are becoming a key part of housing affordability.

For homeowners:

- Monthly expenses are increasing

- Budget planning is more difficult

- Insurance is taking a larger share of total housing costs

For buyers:

- Higher costs may reduce how much home they can afford

- Lenders may factor insurance into affordability calculations

- Total ownership costs are higher than expected

Homeowners Still Showing Resilience

Despite higher costs, overall mortgage delinquency rates remain below historical averages. This suggests that most homeowners are still managing their payments, even with rising expenses.

However, certain groups may feel more pressure, especially those with tighter budgets or homes in high-risk areas.

Ways to Lower Insurance Costs

Homeowners may be able to reduce their premiums by taking a few steps:

- Compare quotes from different insurers

- Bundle home and auto insurance policies

- Increase deductibles

- Upgrade home features to reduce risk (such as roofing or security systems)

Data from Matic shows that homeowners who switched insurance providers saved an average of $928 in 2025.

What This Means for the Housing Market

Higher insurance costs are becoming a long-term factor in housing affordability.

- Buyers may be more cautious when choosing locations

- Sellers in high-cost areas may need to adjust pricing

- Builders may consider risk factors when planning new projects

Insurance is no longer a minor expense — it is now a major part of the cost of owning a home.

Key Takeaways

- Home insurance costs 2026 have risen by about 64% since 2021

- Growth slowed slightly in 2025 but remains high

- Costs vary widely by state and region

- Severe weather and rebuilding costs are key drivers

- Homeowners can reduce costs by comparing policies

Final Thoughts

The rising cost of home insurance is changing the housing landscape. While home values have increased, higher insurance premiums are adding new pressure on affordability.

For buyers and homeowners, understanding insurance costs is now just as important as tracking mortgage rates. Planning ahead and exploring savings options can help manage these rising expenses in the years ahead. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses