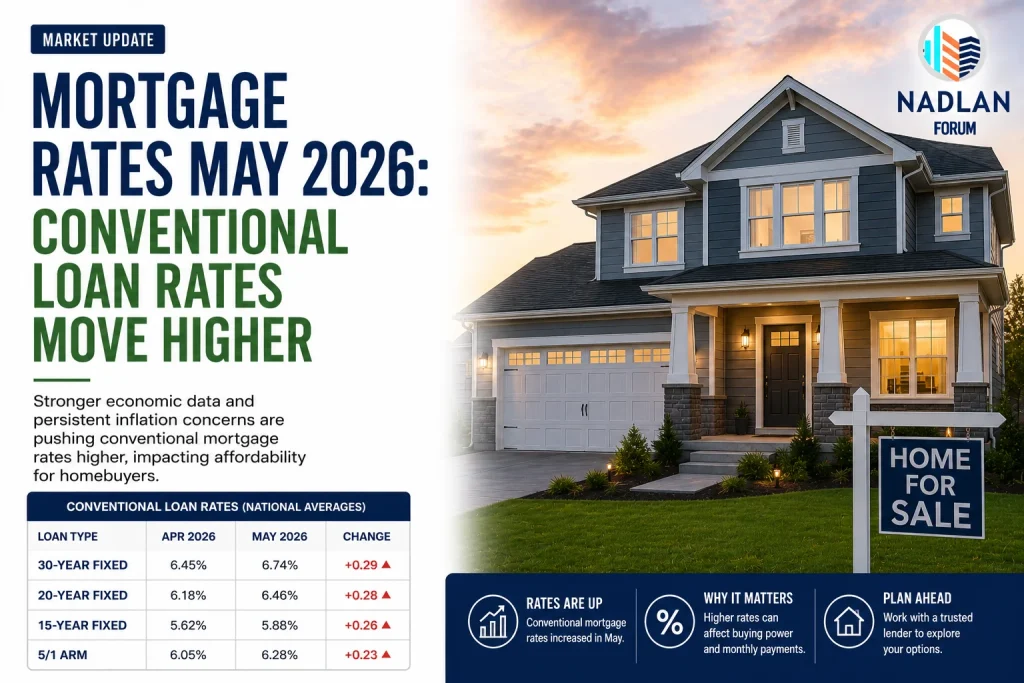

Mortgage Rates May 13, 2026: Conventional Loan Rates Move Higher

Mortgage Rates Rise Across Most Loan Types

Mortgage rates moved higher on May 13, 2026, reversing some of the declines seen earlier in the week.

According to the latest market data, conventional fixed-rate mortgages and adjustable-rate mortgage products all increased compared to the previous day.

The rise follows continued market concerns surrounding inflation and expectations that the Federal Reserve may keep interest rates elevated for longer.

Current Mortgage Rates

National average mortgage rates currently include:

- 30-year fixed: 6.26%

- 20-year fixed: 6.22%

- 15-year fixed: 5.76%

- 5/1 ARM: 6.47%

- 7/1 ARM: 6.30%

- 30-year VA: 5.65%

- 15-year VA: 5.23%

The largest increases were seen in adjustable-rate mortgage products, which rose notably compared to the previous day.

Refinance Rates Show Mixed Movement

Refinance rates also remained elevated, though some categories moved less aggressively.

Current refinance averages include:

- 30-year fixed refinance: 6.23%

- 20-year fixed refinance: 6.24%

- 15-year fixed refinance: 5.66%

- 5/1 ARM refinance: 6.12%

- 7/1 ARM refinance: 5.94%

Refinance rates often remain slightly higher than purchase mortgage rates, although the gap can vary depending on lender competition and market conditions.

Inflation Concerns Continue Affecting Rates

Mortgage markets remain highly sensitive to inflation data and Federal Reserve policy expectations.

Recent consumer and wholesale inflation reports both came in stronger than expected, increasing concerns that interest rates may stay elevated longer than previously forecast.

Investors now expect the Fed to remain cautious about cutting rates while inflation remains above target.

These expectations have helped push Treasury yields and mortgage rates higher.

30-Year Mortgage Remains Most Popular

The 30-year fixed-rate mortgage continues to be the most widely used loan option among homebuyers.

Advantages of a 30-Year Mortgage

- Lower monthly payments

- Predictable fixed payments

- Greater budget flexibility

Because repayment is spread over a longer period, monthly costs are generally more manageable.

Drawbacks

The biggest downside is total interest paid over time.

Borrowers often pay substantially more interest across 30 years compared to shorter loan terms.

15-Year Mortgages Offer Long-Term Savings

The 15-year fixed mortgage remains attractive for borrowers focused on reducing long-term interest costs.

Benefits of a 15-Year Loan

- Lower interest rates

- Faster loan payoff

- Significant interest savings

Tradeoffs

Monthly payments are much higher because the loan balance is repaid in half the time.

Many homeowners choose shorter terms when they have stable income and want to build equity faster.

Adjustable-Rate Mortgages Carry More Risk

Adjustable-rate mortgages, or ARMs, continue to attract attention despite recent increases.

With products such as the 5/1 ARM:

- The rate stays fixed for five years

- The rate adjusts annually afterward

ARMs can sometimes offer lower starting rates than fixed mortgages. However, recent market conditions have reduced that advantage in many cases.

Borrowers using ARMs face uncertainty because future payments depend on interest rate movements after the initial fixed period ends.

Housing Affordability Still Under Pressure

Even though rates remain below the highs reached earlier this year, affordability challenges continue across much of the housing market.

Buyers are still dealing with:

- Elevated home prices

- Higher monthly payments

- Limited inventory in some regions

- Inflation-related living costs

These factors continue slowing housing demand in many areas.

Mortgage Rates Likely to Stay Volatile

Mortgage rates are expected to remain volatile as markets react to:

- Inflation reports

- Federal Reserve statements

- Treasury yield movements

- Labor market data

- Global energy prices

Economic uncertainty continues making daily rate movements more sensitive than usual.

Refinancing Activity Remains Limited

Many homeowners still hold mortgages from 2020 and 2021 with rates below 4%, reducing incentives to refinance into today’s higher-rate environment.

Most refinance activity now comes from:

- Cash-out refinancing

- Debt consolidation

- Shorter-term loan restructuring

rather than traditional rate reductions.

What Buyers Should Watch Next

Future mortgage rate direction will likely depend heavily on inflation trends and upcoming Federal Reserve decisions.

If inflation cools later this year, mortgage rates could stabilize or gradually move lower. However, persistent inflation may keep borrowing costs elevated longer than many buyers expected.

Final Thoughts

Mortgage rates in May 2026 moved higher again as investors reacted to continued inflation pressure and expectations for higher-for-longer Federal Reserve policy.

While borrowing costs remain below recent peaks, affordability challenges continue shaping buyer activity across the housing market. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses