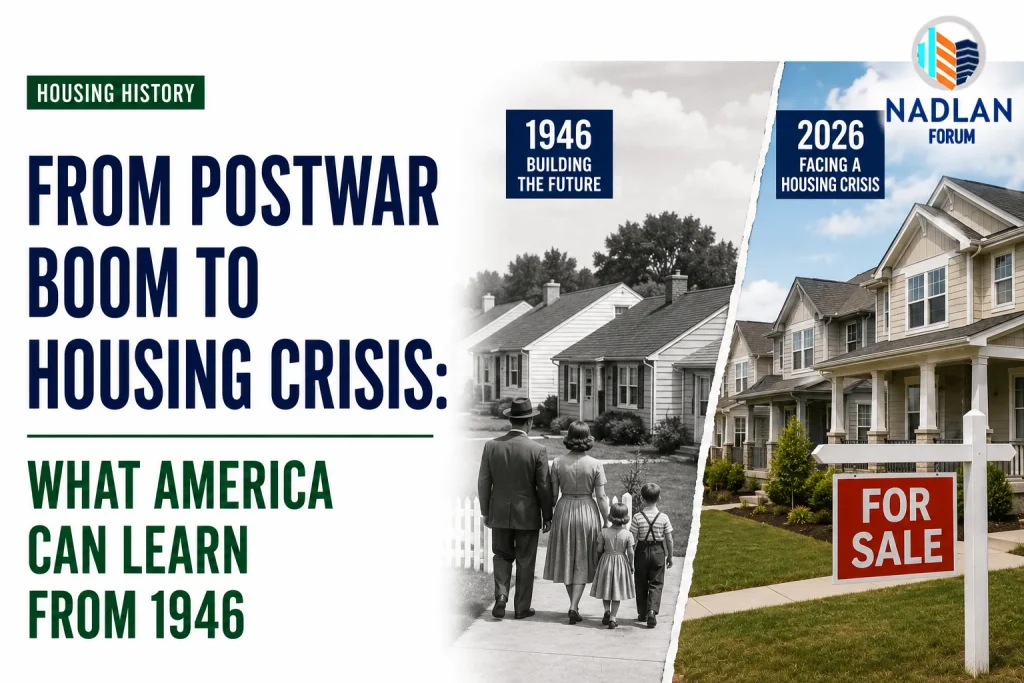

From Postwar Boom to Housing Crisis: What America Can Learn From 1946

America’s housing challenges may seem unique to modern times, but the country has faced a similar problem before. After World War II ended, millions of returning veterans needed places to live, and the nation found itself facing a severe housing shortage.

The response to that crisis changed the country. It helped create the suburbs, expanded homeownership, supported economic growth, and built wealth for millions of families. Today, with housing affordability under pressure and millions of homes still needed, many economists believe there are valuable lessons to learn from that period.

America Faced a Housing Shortage Before

While D-Day remains one of the most important moments in American history, the years that followed brought a different kind of challenge at home.

As soldiers returned from overseas, they wanted to start families and build stable lives. However, there simply were not enough homes available.

Government estimates at the time suggested that more than 2.5 million housing units were needed just for veterans and their families. Despite a population of only about 151 million people, housing shortages forced many Americans into temporary trailers, shared housing, and even tents.

Eventually, the country responded with one of the largest homebuilding efforts in history.

Fast forward to 2026, and the United States once again faces a significant housing shortage. Experts estimate the country is short more than four million homes, while affordability remains one of the biggest concerns for families and first-time buyers.

Lesson One: Housing Is an Economic Issue

After World War II, policymakers understood that housing was more than a social issue.

Leaders believed that building homes would support economic growth, create jobs, and help the nation transition from a wartime economy to a peacetime economy.

President Franklin Roosevelt included affordable housing as part of his vision for America’s future, while President Harry Truman warned that insufficient home construction could slow economic growth and employment.

The country responded by dramatically increasing home construction.

Housing starts climbed from roughly 326,000 units in 1945 to more than one million annually after the war, eventually reaching around two million units in 1950.

Today’s housing market presents similar economic concerns.

Limited housing supply affects:

- Labor mobility.

- Consumer spending.

- Business growth.

- Local economies.

- Household wealth creation.

Many economists argue that increasing housing supply would benefit not only homebuyers but the broader economy.

Lesson Two: Financing Alone Cannot Solve the Problem

Government-backed mortgage programs helped millions of veterans purchase homes after the war.

Lower borrowing costs and improved financing options expanded access to homeownership.

However, financing worked because it was paired with a large increase in housing supply.

Today’s housing market offers an important reminder of that balance.

During the pandemic, historically low mortgage rates helped many Americans buy homes or refinance existing loans. At the same time, limited inventory meant that increased buying power pushed prices significantly higher.

Several ideas have been discussed to improve affordability, including:

- Longer mortgage terms.

- Portable mortgages.

- Alternative financing structures.

While these options may help some buyers, they cannot fully solve affordability challenges if housing supply remains limited.

Increasing demand without increasing supply often results in higher home prices.

Lesson Three: Innovation Can Increase Housing Supply

One of the most famous housing developments in American history was Levittown.

Builders introduced standardized designs and assembly-line construction methods that dramatically increased efficiency.

Instead of building one house at a time, specialized crews completed individual tasks across multiple homes, allowing construction to move at unprecedented speed.

At peak production, homes could be completed in a matter of minutes between each stage of the process.

Modern housing innovations could play a similar role.

Several building methods are attracting attention:

Manufactured Housing

Factory-built homes can often be completed within a few months while reducing construction costs.

Modular Construction

Homes built in sections can shorten project timelines and improve efficiency.

3D Printing Technology

New construction methods continue to develop and may reduce labor requirements and material waste.

Accessory Dwelling Units

Smaller backyard homes can increase housing supply without major neighborhood changes.

Recent market data suggests that manufactured homes have appreciated strongly in value, challenging the perception that they cannot build long-term wealth.

Innovation alone will not solve the housing shortage, but it can become an important part of the solution.

Lesson Four: Housing Opportunities Should Reach More Families

The postwar housing boom created wealth for millions of Americans.

At the same time, many families were excluded from those opportunities due to discriminatory lending practices and unequal access to housing programs.

The effects of those policies continue to influence homeownership rates today.

Large wealth gaps remain between different demographic groups, partly because homeownership has historically been one of the most effective ways to build long-term financial security.

At the same time, homeownership is not the only housing challenge facing the country.

Many households simply need affordable and stable places to live.

Addressing the housing shortage means supporting a range of housing options, including:

- Starter homes.

- Affordable rentals.

- Manufactured housing.

- Multifamily developments.

- Workforce housing.

- Senior housing.

A balanced housing market should provide opportunities for families at different income levels and life stages.

Why Today’s Housing Market Faces Pressure

Several factors are contributing to current housing challenges.

Limited Inventory

The number of available homes remains below long-term demand.

Higher Mortgage Rates

Borrowing costs remain elevated compared with the pandemic period.

Rising Construction Costs

Labor shortages and material costs continue to affect builders.

Population Growth

Household formation continues to increase demand for housing.

Homeowner Lock-In

Many existing homeowners have mortgage rates below current market levels and are reluctant to sell.

Together, these factors have created affordability pressures across much of the country.

Can America Repeat Its Past Success?

The housing boom that followed World War II was not accidental.

It resulted from coordinated efforts involving government policy, private investment, builders, lenders, and local communities.

While today’s housing market is very different, several lessons remain relevant:

- Treat housing as an economic priority.

- Increase supply alongside financing solutions.

- Encourage innovation in construction.

- Expand housing opportunities across income levels.

No single policy will solve the housing shortage, but combining these approaches could improve affordability over time.

The Bottom Line

America’s housing challenges are significant, but they are not without precedent. After World War II, the country faced a severe housing shortage and responded with policies and innovations that expanded homeownership and supported economic growth.

Today’s housing market faces different conditions but many of the same basic problems: limited supply, affordability concerns, and growing demand. History suggests that increasing housing construction, improving financing responsibly, encouraging innovation, and creating opportunities for a broader range of households can help build a stronger and more stable housing market for future generations. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses