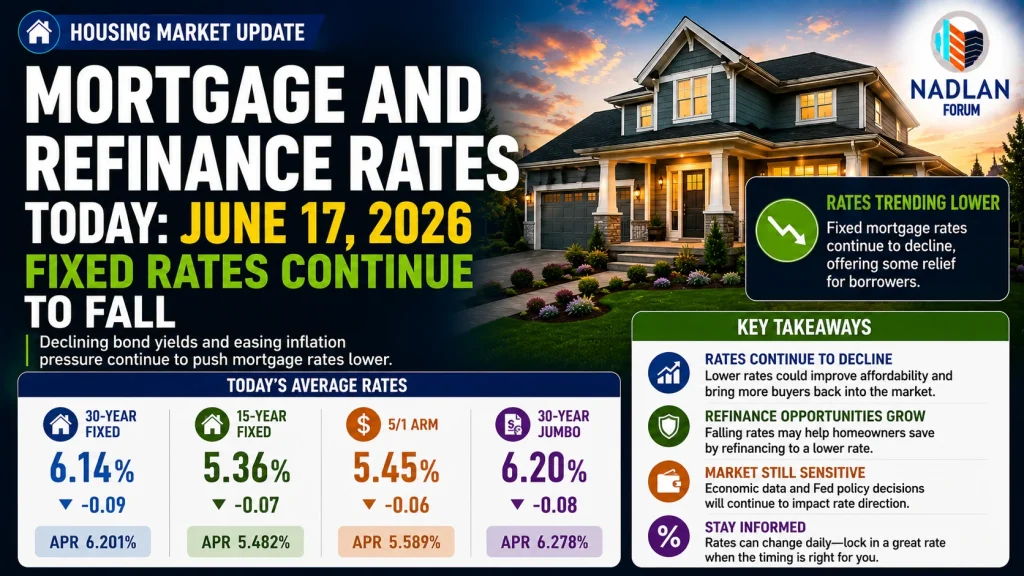

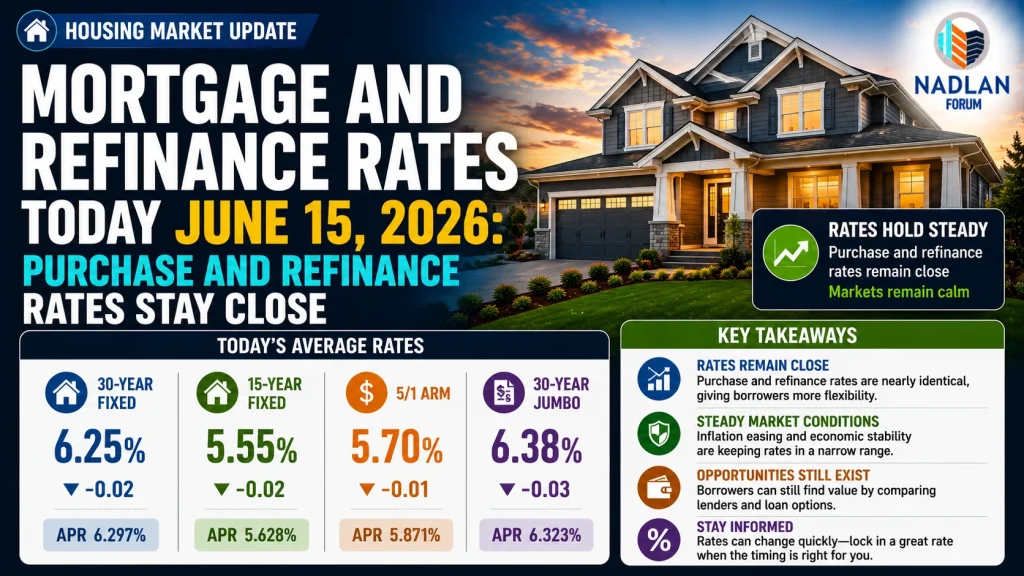

Mortgage and Refinance Rates Today: Fixed Rates Continue to Fall June 17, 2026

U.S. mortgage rates continued their gradual decline on Wednesday, June 17, 2026, according to the latest data from the Zillow lender marketplace. The trend was seen across both purchase and refinance loans, as 30-year and 15-year fixed rates edged lower, while some adjustable-rate mortgages (ARMs) remained relatively steady.

This marks another day of minor rate movements that could impact monthly payments for prospective buyers and homeowners considering refinancing.

Today’s Mortgage Rates (Purchase Loans)

National average rates for major loan types on June 17, 2026:

| Loan Type | Rate |

|---|---|

| 30-year fixed | 6.26% |

| 20-year fixed | 6.06% |

| 15-year fixed | 5.73% |

| 5/1 ARM | 6.30% |

| 7/1 ARM | 6.03% |

| 30-year VA | 5.80% |

| 15-year VA | 5.38% |

| 5/1 VA | 5.58% |

Compared with Tuesday, the 30-year fixed rate fell 5 basis points, the 15-year fixed rate declined 1 basis point, and the 5/1 ARM decreased 1 basis point. Rates are rounded to the nearest hundredth and represent national averages; actual rates may vary by lender and borrower profile.

Today’s Mortgage Refinance Rates

Refinancing rates also showed modest declines:

| Loan Type | Rate |

| 30-year fixed refinance | 6.26% |

| 20-year fixed refinance | 6.04% |

| 15-year fixed refinance | 5.68% |

| 5/1 ARM refinance | 6.20% |

| 7/1 ARM refinance | 6.31% |

| 30-year VA refinance | 5.84% |

| 15-year VA refinance | 5.31% |

| 5/1 VA refinance | 5.69% |

Refinance rates are generally slightly higher than purchase rates but can vary depending on borrower credit scores, debt-to-income ratio, and loan terms.

Advantages of Fixed-Rate Mortgages

Fixed-rate loans provide predictable monthly payments over the life of the mortgage. A 30-year fixed-rate mortgage typically offers:

- Lower monthly payments compared with shorter-term loans

- Payment stability regardless of market rate fluctuations

However, longer terms result in higher total interest paid over the life of the loan compared to shorter-term options.

Comparison Example:

- $400,000, 30-year fixed at 6.26% → ~$2,591 monthly, ~$468,000 total interest

- $400,000, 15-year fixed at 5.73% → ~$3,300 monthly, ~$194,000 total interest

Borrowers choosing shorter-term loans pay more each month but save significantly on interest and build equity faster.

Adjustable-Rate Mortgages (ARMs)

ARMs, such as 5/1 or 7/1 loans, feature:

- Fixed rates for an initial period (5 or 7 years)

- Annual adjustments afterward based on market conditions

Advantages include lower initial payments, but borrowers face the risk of rising rates later in the term. ARMs are often suitable for buyers planning to move or refinance before the adjustment period begins.

How to Get the Lowest Mortgage Rates

Borrowers seeking the most favorable rates can:

- Maintain strong credit scores

- Lower debt-to-income ratio (DTI)

- Consider shorter loan terms

- Shop multiple lenders for the best pricing

Entering the market with higher savings and a stable financial profile improves the chances of locking in lower rates.

Market Outlook

Mortgage rates have been trending lower recently, but small daily fluctuations are expected to continue. Economic indicators, inflation data, and Federal Reserve policy announcements may influence short-term rate movements.

For borrowers, the key takeaway is that even small rate drops can impact monthly payments and long-term interest costs. Prospective homeowners and refinancers should monitor rates closely and consider their financial goals when selecting loan types.

Conclusion

As of June 17, 2026, fixed mortgage rates continue to decline slightly, offering some relief to buyers and refinancers. While rates are moving lower, adjustable-rate products remain largely stable, and borrowers should weigh term length, monthly payment affordability, and long-term interest costs before choosing the right mortgage option. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses