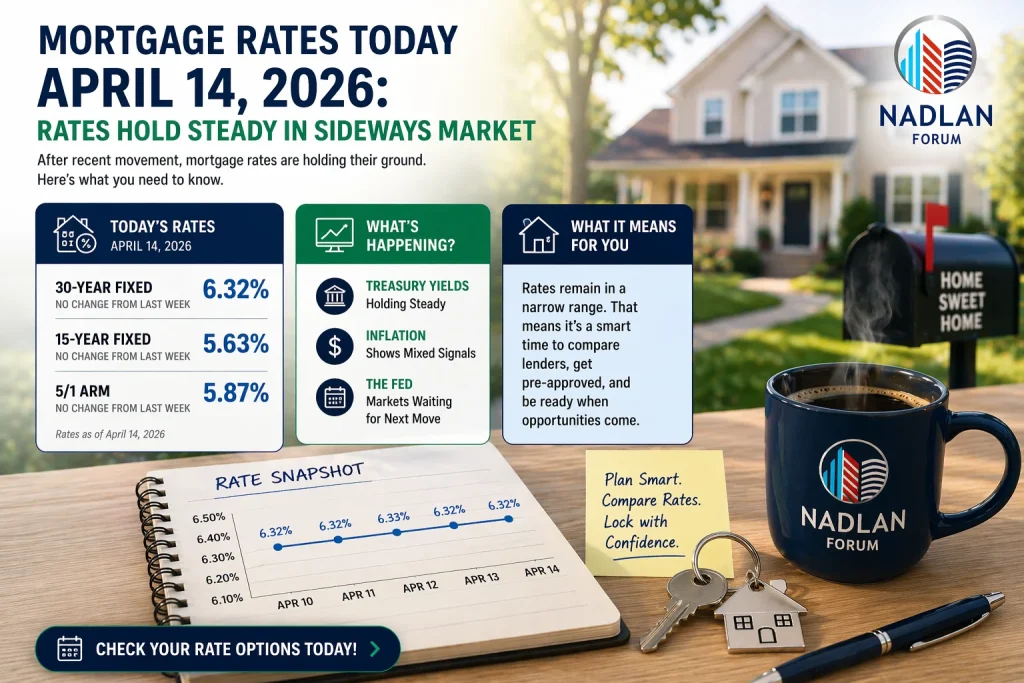

Mortgage Rates Today April 14 2026: Rates Hold Steady in Sideways Market

Rates Show Minimal Movement This Week

Mortgage rates are showing very little change as of mid-April, reflecting a steady market with no strong push in either direction. According to Zillow, the average 30-year fixed mortgage rate has edged up slightly to 6.16%, while the 15-year fixed rate has also moved higher to 5.65%.

These small increases just one basis point highlight a broader trend: rates are moving sideways rather than trending clearly up or down. This pattern is largely tied to the bond market, which has remained stable over the past week. Without a major economic shift or policy change, mortgage rates are likely to stay within a narrow range for now.

Today’s Mortgage Rates Snapshot

Here’s a look at current national average mortgage rates:

- 30-year fixed: 6.16%

- 20-year fixed: 6.05%

- 15-year fixed: 5.65%

- 5/1 ARM: 6.46%

- 7/1 ARM: 6.37%

- 30-year VA: 5.56%

- 15-year VA: 5.25%

- 5/1 VA: 5.37%

These figures are averages and may vary depending on location, lender, and borrower profile.

Today’s Refinance Rates

Refinance rates are slightly higher than purchase rates, which is typical in most market conditions. Current averages include:

- 30-year fixed refinance: 6.27%

- 20-year fixed refinance: 6.22%

- 15-year fixed refinance: 5.73%

- 5/1 ARM refinance: 6.24%

- 7/1 ARM refinance: 6.11%

- 30-year VA refinance: 5.86%

- 15-year VA refinance: 5.53%

- 5/1 VA refinance: 5.46%

Even though refinancing can still make sense for some homeowners, the relatively small gap between current and past rates means fewer people are rushing to refinance compared to previous years.

Why Mortgage Rates Are Moving Sideways

The current rate stability is closely tied to broader economic conditions. Key factors include:

- Stable bond yields

- Mixed inflation signals

- No major policy changes from the Federal Reserve

- Ongoing global uncertainty

Mortgage rates tend to follow the 10-year Treasury yield, and with that benchmark showing limited movement, home loan rates are also staying within a tight range.

Until new economic data such as inflation reports or employment numbers—shifts expectations, this sideways trend may continue.

30-Year vs. 15-Year Mortgage: What to Know

Borrowers often compare 30-year and 15-year loans when deciding on financing. Each option has clear trade-offs:

30-Year Fixed Mortgage

- Lower monthly payments

- Higher total interest paid over time

- More flexibility for budgeting

15-Year Fixed Mortgage

- Higher monthly payments

- Lower interest rates

- Significant savings on total interest

For example, a $400,000 loan at 6.16% over 30 years results in a monthly payment of around $2,440 and nearly $478,000 in total interest.

The same loan at 5.65% over 15 years increases the monthly payment to about $3,300 but reduces total interest to roughly $194,000.

For buyers who can afford higher monthly payments, shorter loan terms can lead to major long-term savings.

Fixed vs. Adjustable-Rate Mortgages

Another key decision for borrowers is choosing between fixed-rate and adjustable-rate mortgages (ARMs).

Fixed-Rate Mortgages:

- Rate stays the same for the entire loan term

- Predictable monthly payments

- Better for long-term stability

Adjustable-Rate Mortgages (ARMs):

- Lower or similar starting rates

- Rate changes after an initial fixed period

- Payments can increase over time

In today’s market, ARMs are not always cheaper than fixed rates, which reduces their appeal for many buyers. However, they may still work for borrowers planning to move or refinance within a few years.

What This Means for Homebuyers

A stable rate environment can be helpful for buyers because it reduces uncertainty. Instead of rushing to lock in a rate, buyers have more time to:

- Compare lenders

- Improve credit scores

- Save for a larger down payment

However, affordability remains a challenge, as rates are still higher than the historic lows seen in recent years.

Outlook for Mortgage Rates in 2026 and Beyond

Forecasts suggest mortgage rates may remain close to current levels through the rest of 2026. Industry expectations indicate:

- Around 6.30% average for 30-year loans in 2026

- Potential drop below 6% by year-end (depending on inflation trends)

Looking ahead to 2027, projections vary. Some forecasts expect rates to stay near current levels, while others suggest a gradual decline toward the mid-5% range.

Final Thoughts

Mortgage rates today show a market that is stable but still sensitive to economic changes. While rates are not falling sharply, they are also not rising significantly, giving buyers and homeowners a window to plan carefully.For now, the best strategy is to focus on personal finances credit score, savings, and debt levels rather than trying to predict short-term rate movements. For direct financing consultations or mortgage options for you visit 👉 Nadlan Capital Group.

Responses